At the simplest level a personal contract purchase agreement, or PCP, is a way of financing the buying of a car. Since their invention in the 1990s when they were first introduced by Ford under the Options brand, PCPs have become the most popular way for individuals to run a new car.

Sometimes also referred to as personal contract plans, PCPs, which are available on new and used cars now account for around three quarters of all consumer car finance and could, arguably, be credited with driving the new car market to the levels it’s at today.

What is a PCP finance agreement?

A PCP agreement is a way of buying a car through a finance agreement. Officially, they’re a form of hire purchase which means you’re agreeing to buy the car and you’re paying a regular (monthly amount toward this).

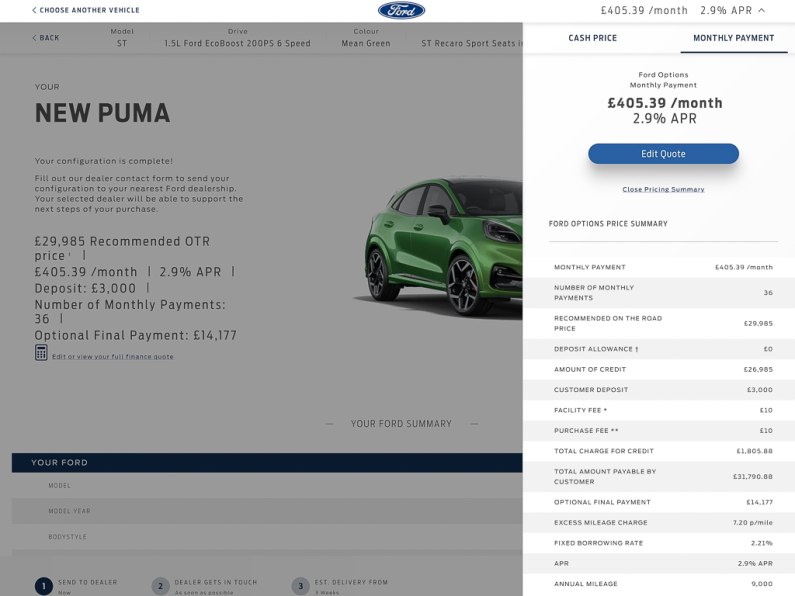

Unlike a straight hire purchase agreement where you put down a deposit then pay off the entire cost of the car over a set number of months, in a PCP scheme you put down your deposit, then you pay a monthly fee for a set time (usually three years) and at the end of that time and you want to own the car outright, you’ll pay a final (normally larger) amount to cover the outstanding cost of the car. This amount will have been agreed at the start of the contract and is usually known as the guaranteed minimum future value (GMFV).

The GMFV is set based on what the minimum amount the car will be worth at the end of the contract (as set by the finance firm).

At this point customers also have two options. If they want to buy another car and their current car is worth more than the GMFV then this difference can be used as a deposit (or part of a deposit) for the next car, or they can simply hand the car back and start again.

Advantages

The advantage of a PCP agreement over other forms of finance are that monthly payments are often lower than a standard loan or hire purchase agreement, this makes cars – particularly those with strong used values – seem more affordable.

Alongside a lower monthly payment, PCPs offer buyers a safety net on the value of their car. Because the agreement includes a minimum value, if the car’s value falls below this point by the end of the agreement the customer won’t lose out – instead the finance company will take any additional hit.

Disadvantages

Oddly, this advantage can also be a disadvantage. Because used car values can change, you can start a PCP agreement expecting the car to be worth more than the GMFV so that you will have enough for a deposit on your next car, but if the market changes this may not be the reality when you come to change cars.

A good PCP deal will leave a good safety buffer between the GMFV and what the car should be worth at the end of the contract. That way you’ll be able to use that difference as the deposit for you next car. Without that buffer, you’ll need to find an all new deposit from scratch (or rather, your savings).

Start of a PCP

When looking at PCP agreements there are lots of things to consider.

On new cars, manufacturers often promote vehicles with incentives. In the world of PCPs this can be a low interest rate, or it could be a ‘deposit contribution’ – sometimes also known as a ‘dealer contribution’ or a ‘deposit allowance’. In reality, this is a discount on the price of the new car.

The larger the initial deposit or discount, the smaller the monthly payment – because the amount you need to finance between the total price and the GMFV is decreased.

What also changes the monthly payment is if the GMFV is changed on paper. The only way this happens is if you change the expected mileage. Obviously, used car prices vary with mileage; so more miles equal a lower value. In other words, if you know you’re going to do 9,000 miles a year, don’t go for an agreement where you’re paying on the expectation of 12,000 miles. On the flipside, in this example, if you agree to a 6,000 miles a year agreement and end up doing 9,000 a year, then you’ll be hit for excess mileage costs. The details of which should be clearly set out in the contract.

Early termination

Like any finance agreement, there are very strict rules about what can and can’t be done with a PCP. Handing the car back early is possible.

If you’ve paid more than half of the contract then you can terminate the agreement. If you’ve not yet paid half, then you can go for an early settlement which means you pay off (and then fully own) the car. In this circumstance you won’t be charge for the remaining interest.

More switched on dealers will often call customers well in advance of the contract end to offer a new car if they need used car stock or know they can move you into a new car at no cost to yourself. However, this will depend on the value of the car you’re in and the one you want to buy (or they want to sell).

End of a PCP

Aside from checking the mileage at the end of your PCP, the other main influence on the car’s value will be its condition.

This will have to be within prescribed limits. In other words, you can’t expect to get away with damage on the car at the end of the contract as this will be taken into account. However, fair wear and tear is fine; this is the kind of damage that is almost unavoidable. For example, a car at 30,000 miles could be expected to have a few stone-chips on the bonnet.

Keyword: Everything you need to know about PCP car finance