It’s easy to point fingers at the victim. It’s somewhat natural to have a “serves him/her right” attitude to those in trouble. I’ve been guilty of this, and you probably have as well. But sometimes, you just never know what’s around the corner. Back in 2019, who’d have thought that a pandemic of epic proportions would hit the earth, shut international borders and change our lifestyles forever?

This writer was one 2019 car purchase away from financial ruin in 2020 – handshake done, but the deal somehow fell through – so I dodged a bullet there because my monthly commitments would have been way too much for my 2020 income.

Not many are so lucky. With Covid-19 came lockdowns to keep the virus at bay, and that really hurt the economy. Some sectors were decimated overnight, jobs were lost, and plenty had to start all over again in another field, or set out on their own. New normal income with pre-Covid commitments? Not a good match.

The loan moratorium provided last year helped stop the bleeding, so to speak, and the banks have continued to provide targeted assistance ever since, even though this is not widely known. But for some, a couple of months of deferred payments is merely a plaster for the wound, and some restructuring is needed.

That’s where URUS comes in. Open for application starting November 15, the Financial Management and Resilience Programme (URUS) is a co-created scheme by the Malaysian banking industry and AKPK (Agensi Kaunseling & Pengurusan Kredit), a Bank Negara Malaysia (BNM) agency set up to provide debt management programmes. It is described as a holistic assistance package to assist vulnerable borrowers with prolonged cash flow difficulties due to Covid-19.

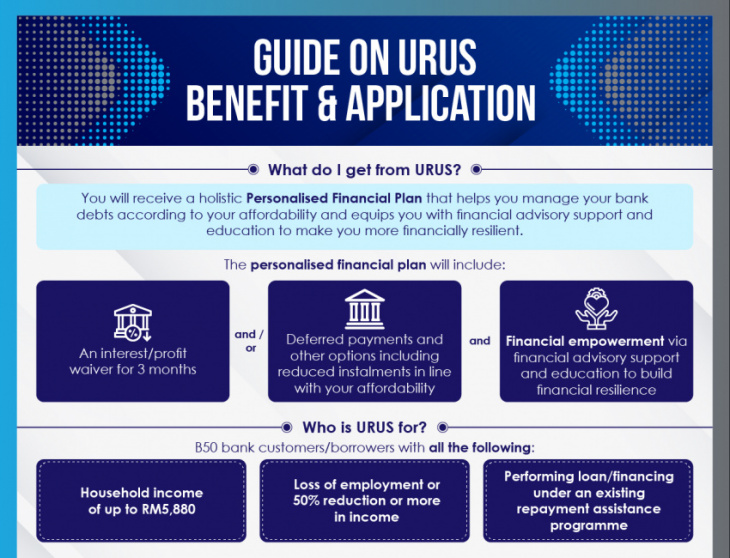

Some would want to know immediately, and yes, URUS includes deferred payments and other options such as reduced instalments to fit your current financial capability. There’s also an interest (or profit for Islamic banking) waiver for three months, but there’s more to URUS than this.

Apart from sticking the plaster, URUS provides personalised financial plans, financial education programmes, and avenues for income supplementation and other support via referrals to the AKPK Social Synergy Network. It is hoped that this assistance will get you back on the right track, financially.

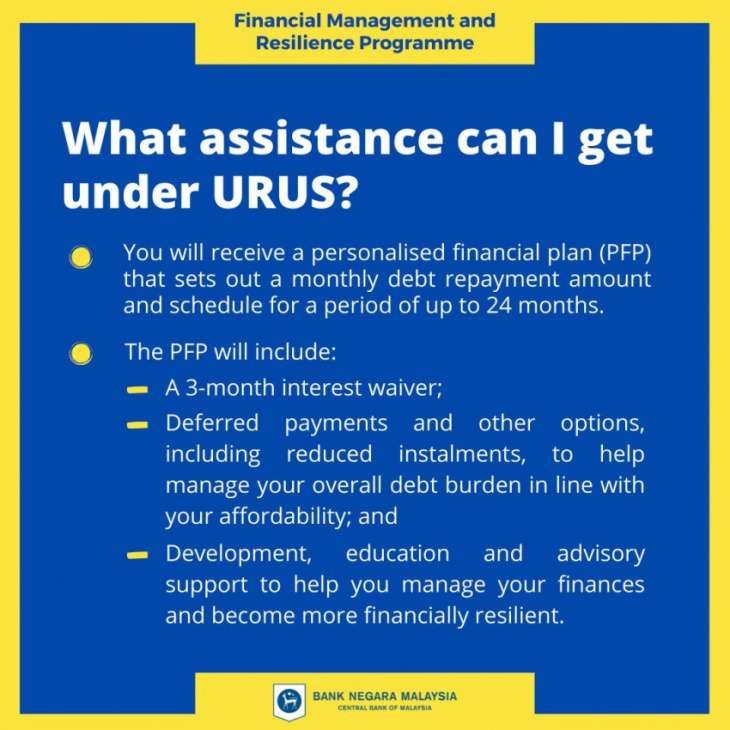

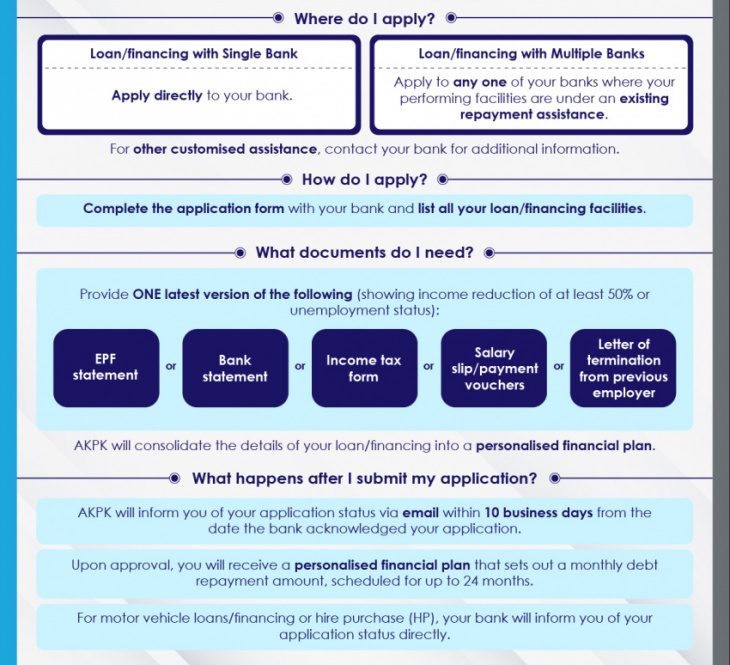

Sign up for URUS anytime from now till January 31, 2022 and you’ll receive a Personalised Financial Plan (PFP) that sets out a monthly debt repayment amount and schedule for up to 24 months. The plan will take into account all your existing obligations and the portion of income you can currently afford to set aside for debt repayment, after providing for living expenses.

The PFP will include an interest waiver for a period of three months; an additional option for deferred payments and other options, including reduced instalments to help manage your overall debt burden; and development, education and advisory support to help you manage your finances and be more financially resilient in the long-term.

Those under URUS will also have access to AKPK financial advisors to review their PFP or seek advice on financial management issues. The experts will also help borrowers deal with their banks on matters relating to their loan repayments under URUS.

It’s never too late to learn good financial planning, and this could be a good time to start afresh. The education element in URUS comes in the form of free online learning to enhance your financial management knowledge and skills. Topics covered include goal setting, cash flow management, borrowing/financing basics, managing debt and wealth management.

Last but not least is AKPK’s Social Synergy Network, which is a collaborative effort between various agencies such as Perkeso, MDEC, Tekun and Giatmara. This network enables you to obtain assistance via referrals to relevant agencies, including avenues for income supplementation via employment opportunities, financial aids and benefits, digital training and business platforms, business funding, upskilling and reskilling training, and even emotional advisory support.

So who’s eligible to apply for URUS? The programme is targeted at B50 customers who are already under an existing repayment assistance programme (it can be Targeted Repayment Assistance, Pemerkasa Plus, Pemulih or a bank’s own rescheduling and restructuring) as at September 30, 2021.

Your gross household income has to be no more than RM5,880, and your loan/financing must still be performing (not in arrears exceeding 90 days) as at the date of application. Loss of employment or at least a 50% reduction in income is also a requirement.

Loans and financing eligible for URUS includes housing loan, personal loan (including ASB loan, education loan), vehicle hire purchase loan, and credit card balances (or other revolving credit lines such as overdraft or trade credit facilities) that have been converted into term loan/financing.

You don’t need a stack of documents – only simple ones such as your EPF or bank statement, income tax form, payslip or termination letter are required to prove your unemployed status or income reduction of at least 50%. Those who have loans from multiple banks will only need to apply to one of their banks with the common URUS application form, listing down the full list of loans, and AKPK will help consolidate the details and do the rest. AKPK’s services, including URUS, are free of charge.

What if you’re tight financially but not eligible for URUS? Not many seem to realise, but the banks are still providing assistance to those who need it, in targeted form rather than a blanket moratorium. Don’t be shy to approach your bank for other forms of repayment assistance suitable to your financial circumstances.

If you’re in a tight spot financially, don’t be embarrassed to seek help. Juggling it around and doing the minimum will only compound the debt, and deep down we know the odds for a windfall to wipe the slate clean is very slim. Acknowledging the problem is the first step, and programmes such as URUS are designed to help “reboot” the situation and stop the slide.

If you face problems from your bank in applying for URUS, you can lodge a complaint to BNM by filling up this online form. For more info on URUS, click here.

Keyword: More than just loan deferment, URUS by Malaysian banks, AKPK is a holistic assistance plan for the B50