The electric vehicle revolution has passed its point of no return, and the latest market share predictions could soon become obsolete.

- Analysts now expect the US EV market to reach at least 30% by 2030.

- California’s 2035 ZEV rule could push most EV sales to 16 states, with the other 34 leaning heavier toward internal combustion.

- There is hope for breakthroughs in scarce material procurement and North American battery production.

In March 2020, just before the COVID-19 pandemic shut down businesses across the globe, General Motors offered Wall Street analysts and auto journalists a sneak peek at its future EV portfolio, including the GMC Hummer and Cadillac Lyriq and Celestiq. CEO Mary Barra said GM would sell 1 million EVs by 2025—though that’s worldwide, mostly in China. Before her announcement, hardly anyone in the business predicted the US market for EVs would breach the 10% level by 2030.

Today, such a forecast would be obsolete.

Since then, future EVs from startup Tesla competitors and legacy automakers alike have taken over the new car-and-truck conversation. By 2030, all new Ford Mustangs, Lincolns, Chevrolet Camaros, replacements for Dodge’s Charger and Challenger, all Buicks and Volvos, a new-age VW Microbus, and some percentage of Corvettes will be battery-electric.

Just last week, the California Air Resources Board announced its latest emissions-fighting rule banning anything but zero-emissions vehicles by 2035. According to CARB’s estimates, California and the 15 other states that usually hitchhike the state’s waiver exempting it from US Environmental Protection Agency emissions standards account for 36.5% of the nation’s auto market.

Ford and GM have since issued statements in support of California’s 2035 rules, shortly after CARB passed them on Aug. 25.

Ford F-150 Lightning.

Ford

AutoForecast Solutions estimates 5.27% of new vehicles sold in the US this year will be all-electric, and that will jump to 9.23% in 2023, nearly tripled from 3.28% in 2021, and up from 1.41% in 2019.

“The future is already here,” says Michael Dunne from automotive global intelligence firm ZoZoGo. “It’s just unevenly distributed. We’re not looking at mass adoption yet.” At an average price of $66,000 for EVs, and two-thirds of them Teslas in California, “we’re really talking about a premium market.”

EV tax credits extended in the recently passed Inflation Reduction Act, which establish as-yet unobtainable standards for US and trade-partner manufacturing, processing, and materials mining, will be available on EV cars with MSRPs up to $55,000 and EV trucks and vans up to $80,000.

Slightly mitigating spikes in Tesla and Ford F-150 Lightning MSRPs (due to rare material and parts shortages) are a similar spike in the price of conventional internal-combustion-powered vehicles—now more than $48,000 on average—and the summer’s gas price hike to more than $5 per gallon after Russia’s invasion of Ukraine.

“From our latest bi-monthly Fuel Price Impact Survey, consumer intention for purchasing an EV rose from 4% in 2020 to 10% in 2021 and 11% in 2022,” says Paul Waatti, AutoPacific’s manager for industry analysis.

AutoPacific expects EVs will represent 17.5% of the US auto market by 2027. And while China and Europe are expected both to reach 50% EV share by 2030, “the US will likely be closer to the 30-40% range,” Waatti says.

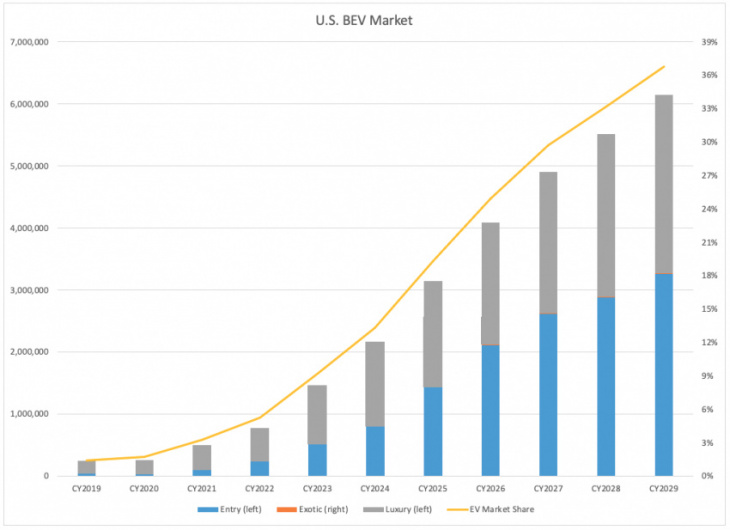

AutoForecast Solutions is more EV-optimistic, expecting US market share to reach 29.71% in 2027 and 36.7% in 2029—a sufficiently large market to satisfy the expected 16-state ZEV standard six years ahead of time.

ZoZoGo’s prognostication comes in absolute numbers: 14 million BEVs in China, 7 million in Europe, and 4 million in the US by 2030, Dunne says. US share will depend on how the entire market shakes out after four straight years of 17-million-plus sales in the late-‘10s to under 14 million annually since the pandemic—between 28.6% and 23.5%, respectively.

The shortcomings of this post-industrial paradigm shift from ICE to BEV does not happen in a vacuum, of course. California’s 100%-ZEV mandate does nothing about the millions of cars and trucks sold there through December 2034 (revive Cash for Clunkers, anyone?).

While 16 states buying all those EVs should make a dent in greenhouse gas emissions, we’ll still have huge fleets of airliners and private jets and, presumably, a bitcoin market. So long as EV materials and production are limited, most of the 2030-35 production will have to go to those 16 states, with consumers in the remaining 34 states leaning toward ICE vehicles. It all depends how quickly—and how extensively—automakers tool up to manufacture EVs.

European version of VW ID. Buzz.

Volkswagen

Continuous development of battery technology could help solve that last issue and further fuel the industry’s ongoing conversion. According to ZoZoGo’s Dunne, two potential battery chemistry breakthroughs—nickel-cobalt-magnesium and lithium-iron-phosphate—could help solve the scarce material problem before decade’s end.

Volkswagen Group and Mercedes-Benz already have signed pacts with the government of Canada, one of our chief trade partners, to “explore deeper cooperation across all stages of the automotive value chain” that will include battery production and material extraction.

Despite all these shortcomings in the technology—or perhaps because of them—the electric vehicle revolution has passed its point of no return, and these latest market share predictions could become obsolete in a few more years.

Keyword: California’s 2035 Zero-Emissions Mandate Is Just Keeping Up with the Industry