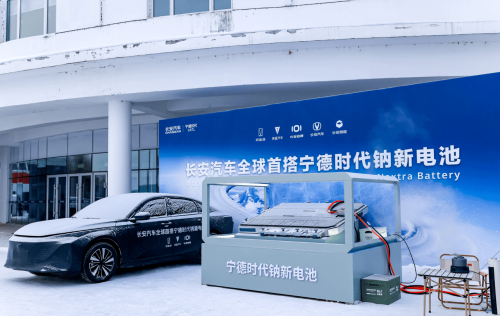

The commercialization of sodium-ion batteries is accelerating rapidly in China. Chinese new energy materials company Pret said at a recent earnings briefing that multiple sodium-ion battery products have already entered mass shipment stage, with applications covering energy storage, backup power, vehicle start-stop systems and specialty vehicles. At the same time, the company is building a sodium battery production base in Neijiang, Sichuan province. The first-phase 2 GWh production line is expected to begin operations in the second half of this year. Compared with previous years, when sodium-ion batteries remained largely at the laboratory stage, more companies are now moving toward mass production. At the end of April, CATL signed a three-year 60 GWh sodium-ion energy storage battery supply agreement with HyperStrong, currently the world’s largest sodium battery order. CTAL’s sodium-ion battery Days later, CATL subsidiary Fuding Times disclosed a new sodium-ion battery expansion project with total investment of RMB 5 billion ($735 million), adding 40 GWh of new capacity. From an industry perspective, sodium batteries are beginning to shift from “technology validation” to “scale manufacturing.” Compared with lithium batteries, sodium batteries’ biggest advantages are not performance, but lower costs and more stable resource availability. At present, sodium battery energy density is around 175 Wh/kg, still below mainstream lithium iron phosphate (LFP) batteries. This makes it difficult for sodium batteries to enter premium long-range EV segments. LFP battery However, they are becoming increasingly attractive in cost-sensitive markets such as compact EVs, A00-segment vehicles and energy storage systems. Raw material economics are a key factor. Lithium carbonate prices experienced extreme volatility over recent years, surging from tens of thousands of yuan per ton to more than RMB 600,000 ($88,300) per ton before falling sharply. In contrast, battery-grade sodium carbonate prices have remained relatively stable, while sodium resources are significantly more abundant than lithium. That stability is particularly important for the low-margin small EV market. According to CPCA data, combined sales of China’s A0- and A00-segment new energy vehicles exceeded 2.35 million units in 2025, accounting for roughly 15% of the country’s NEV market. Geely Xingyuan Although profit margins in this segment are relatively thin, the associated battery demand remains substantial. Over the past few years, nearly all major small EV hits — including the Geely Galaxy Xingyuan, BYD Seagull and Wuling Bingo — have used LFP batteries. But that landscape could begin to change as sodium batteries approach commercialization. In February, Changan and CATL jointly unveiled a global sodium battery strategy. Changan’s Deepal, Avatr and Nevo brands are all expected to launch sodium battery models in 2026. Changan’s first EV equipped with CATL’s Naxtra battery will launch in mid-2026 Meanwhile, Chery, GAC, Seres, SAIC-GM-Wuling and BAIC have also joined CATL’s sodium battery and battery-swapping cooperation network. Sodium battery cell costs are now approaching those of LFP batteries, and further declines are expected as production scales up. For small battery EVs priced between RMB 50,000 ($7,360) and RMB 100,000 ($14,700), lower and more stable battery costs could provide greater pricing flexibility and stronger profit buffers.