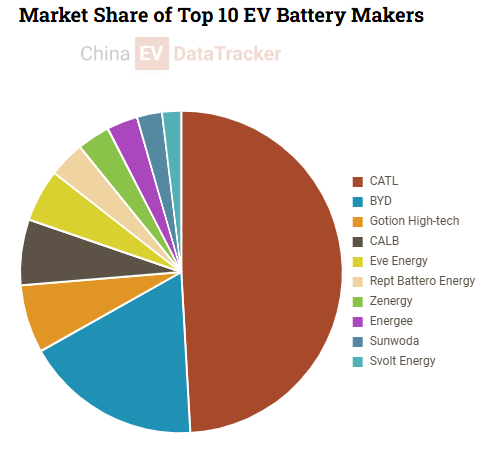

Visitors at the Svolt booth during CIBF 2026 in Shenzhen. Credit: EastMoney Understand China EV’s Market Real-time notifications when critical EV data is released All important data in one place 2,000,000+ data points Become a member China’s largest battery industry exhibition, the China International Battery Fair (CIBF 2026), opened in Shenzhen with packed booths from CATL, BYD, and hundreds of supply chain companies. But the most important developments at the event were not necessarily the flagship battery cells displayed by the industry’s biggest names. Instead, the strongest technical and commercial momentum came from deeper inside the supply chain, where equipment makers, electrolyte specialists, and mid-tier battery firms pushed manufacturing tools, compliance-ready production lines, and large-scale commercialisation plans rather than concept displays. Held from May 13 to 15 at the Shenzhen World Exhibition & Convention Centre in Bao’an, the event covered more than 280,000 square meters and drew over 350,000 professional visitors and buyers, according to organisers and industry statements released during the exhibition. The exhibition also reflected a broader shift inside China’s battery sector. Industry discussions shifted away from aggressive price competition that dominated 2025 toward production scaling, delivery schedules, certification requirements, and manufacturing standardisation for overseas markets. The toolmakers behind solid-state batteries More than 200 companies across the solid-state battery supply chain attended the exhibition, but the industrial focus shifted beyond prototype cells displayed in glass cases. Chinese equipment suppliers, including Microna, Hosong Group, and GaoNeng ShuZao, showcased dry-room systems, glovebox setups, dispersing equipment, and dry-electrode processing machinery designed for sulfide and halide electrolyte production lines. The equipment push comes as multiple companies move toward 400 Wh/kg-class semi-solid and solid-liquid battery architectures. Gotion High-Tech displayed a 161 kWh battery pack, while companies including Weilan and China National Battery presented 400 Wh/kg sample cells aimed at robotics, low-altitude aircraft, and specialised mobility applications. Electrolyte suppliers, including Langu, Youyan Guangdong, Kunlun, and Jiuwu Hi-Tech, demonstrated parallel development routes involving oxide, sulfide, and halide systems rather than a single dominant chemistry path. One of the more closely watched startups at the exhibition was Pure Lithium New Energy, which recently demonstrated a solid-state battery continuing to operate after a cut test and announced plans to reach 500 MWh of production capacity. ESS standardisation accelerates While flagship EV battery products from CATL and BYD remained largely familiar from earlier launches, the strongest commercial competition at CIBF centred on energy storage systems. The industry increasingly converged around 587Ah and 588Ah large-format ESS cells. CATL and Haisen pushed 587Ah products into scaled delivery, while companies including CALB, Rept Battero, and Sunwoda aligned around 588Ah platforms planned for 2026 deployment. BYD also expanded deliveries of its 2,710Ah ESS Blade battery cell for utility-scale grid projects. Several mid-tier firms drew attention with alternative technical approaches. Changzhou Changsheng promoted all-tabs cylindrical battery designs, while Zhongqi Xinneng displayed large cylindrical cells integrating lithium-rich manganese materials. A separate BYD Blade battery teardown published just after the exhibition period also highlighted how Chinese battery companies increasingly use public durability demonstrations as industrial marketing tools. The teardown revealed a 170-cell battery pack after a 40-hour freeze test, while the dismantling team later defended its eight-hour disassembly process amid online criticism. Market share of top 10 EV battery makers in China (April 2026). Credit: China EV DataTracker Sodium-ion moves toward practical niches Sodium-ion battery companies adopted a more restrained commercial stance than in previous industry cycles. Rather than directly challenging lithium iron phosphate batteries, companies including CATL, Pengwei, and Na-Bat Group focused on two-wheelers, starter-lighting-ignition systems, and small-scale energy applications, with energy density levels generally stabilising above 100 Wh/kg. At the same time, carbon nanotube suppliers expanded aggressively as ultra-fast charging development continued across China’s EV sector. According to China EV DataTracker’s latest battery installation data from April 2026, CATL remained China’s largest EV battery supplier with 29.06 GWh installed and a 47.2% market share, while BYD ranked second with 10.49 GWh and a 17.1% share. Gotion High-Tech, CALB, Eve Energy, Rept Battero, Zenergy, Energee, Sunwoda, and Svolt Energy completed the top ten rankings for the latest reported period. The broader message from CIBF 2026 was less about a single breakthrough battery chemistry and more about manufacturing infrastructure. While overseas automakers and consortia continue evaluating long-term solid-state battery pathways, Chinese suppliers are already commercialising the production tools, pilot lines, and compliance-ready industrial systems required to build them at scale. Sources: STCN, XHBY, Eastmoney Battery suppliers at CIBF 2026 focused on manufacturing infrastructure, solid-state development, and practical sodium-ion battery applications.

![BYD launches 4-seat ultra-luxe flagship SUV for $215,000 [Images]](https://cdn.topcarnews.net/thumb/id/aHR0cHM6Ly9pMC53cC5jb20vZWxlY3Ry-ZWsuY28vd3AtY29udGVudC91cGxvYWRz-L3NpdGVzLzMvMjAyNi8wOC9CWUQtWWFu-Z3dhbmctVThMLTQtc2VhdC5qcGVnP3c9-MTUwMCZhbXA7cXVhbGl0eT04MiZhbXA7-c3RyaXA9YWxsJmFtcDtzc2w9MQ/968bb80271e248ee95003667e96d87fa.jpeg?t=20260807&post_id=52016)