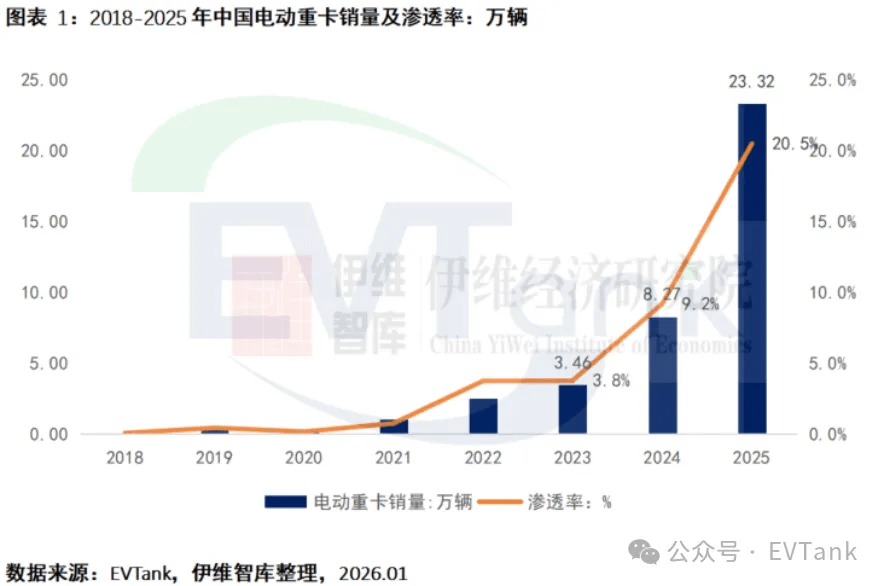

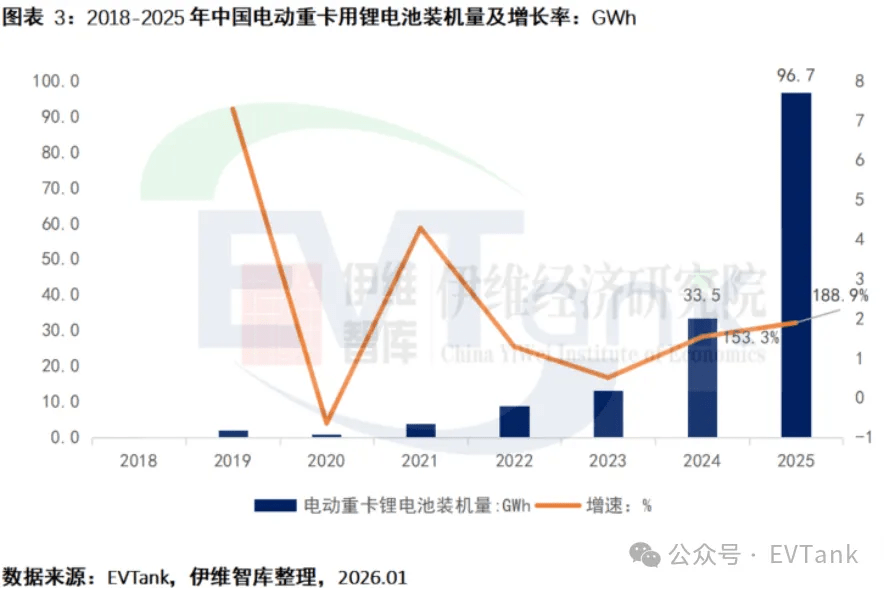

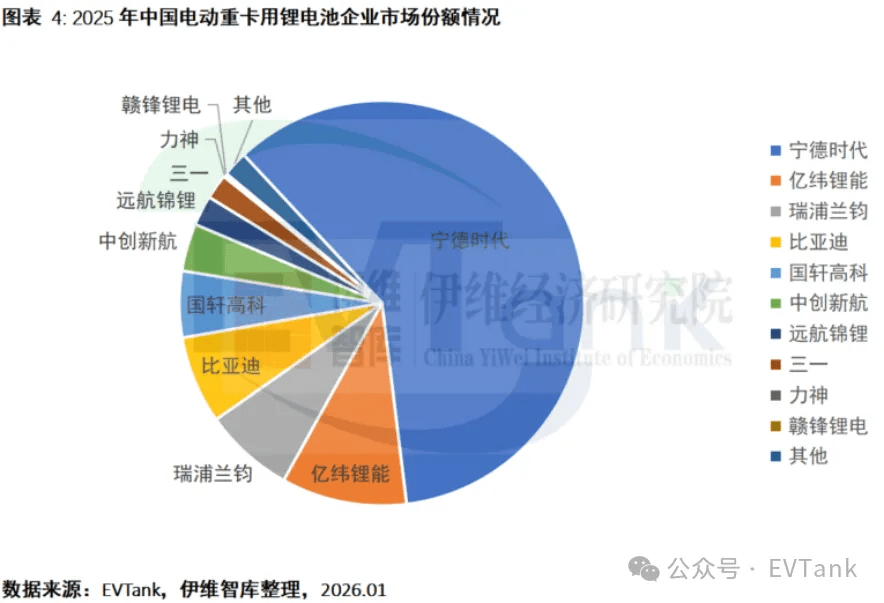

On the battery front, LFP remains dominant, accounting for over 99% of installations, while CATL retained the top supplier position with a 60% share, followed by EVE Energy, REPT Battero and BYD. On January 29, EVTank, together with the China YiWei Institute of Economics, released the China Electric Heavy-Duty Truck Industry Development White Paper (2026). According to the report, China’s electric heavy-duty truck market recorded a significant leap in 2025, with annual sales reaching 233,200 units, up 181.9% year on year. Driven by strong sales growth, the overall electrification rate of the heavy-duty truck sector rose to 20.5% in 2025, an increase of 11.3 percentage points from 2024, making it the fastest-growing new energy segment after passenger vehicles. Sales volume and penetration rate of electric heavy-duty trucks in China from 2018 to 2025 In terms of OEM competition, XCMG Group ranked first in 2025 with a market share of 15.4%, followed by SANY Group and FAW Jiefang. Together, the top three manufacturers accounted for 42.9% of total market sales. On the battery side, lithium-ion batteries remained the mainstream solution for electric heavy-duty trucks. Prismatic LFP batteries accounted for more than 99% of installations, supported by advantages in safety, cycle life and cost. In 2025, total lithium battery installations for electric heavy-duty trucks reached 96.7 GWh, up 188.9% year on year. LFP battery installations for electric heavy-duty trucks in China from 2018 to 2025 At the same time, fuel cell heavy-duty truck sales climbed to 7,282 units, also driving growth in fuel cell system installations. Among battery suppliers, CATL maintained its leading position with a 60.0% market share, although its dominance eased compared with previous years. EVE Energy, REPT Battero and BYD followed, with market shares of 10.0%, 7.2% and 7.0%, respectively. Market share of battery manufacturers in China for electric heavy-duty trucks in 2025 In terms of supply relationships, CATL supplies nearly all major heavy-duty truck manufacturers, while other battery makers have formed relatively stable partnerships with leading OEMs. The report also highlighted intensifying competition around charging efficiency. In 2025, ultra-fast charging batteries, high-voltage platforms and megawatt-level fast chargers were rolled out at pace, including BYD’s Tianxing battery, Sunwoda’s Gen2 solutions, and EVE Energy’s LF230P 453 kWh battery. As charging infrastructure continues to improve, high-capacity electric heavy-duty trucks are increasingly penetrating long-haul transport scenarios. EVTank expects long-haul logistics to emerge as a new growth driver for electric heavy-duty trucks in 2026.