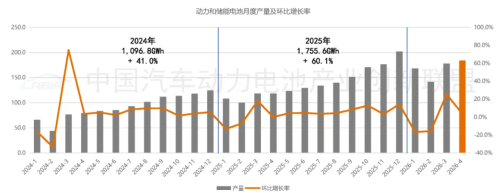

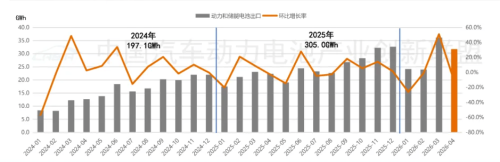

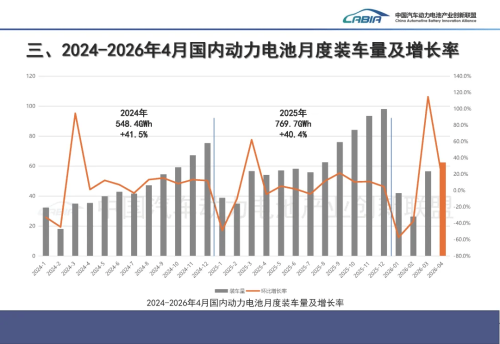

On May 11, the China Automotive Battery Innovation Alliance released its monthly battery industry data for April 2026. China’s power and energy storage battery sector continued to expand in April. Total production of power and storage batteries reached 183.9 GWh, up 3.5% month-on-month and up 55.6% year-on-year. Cumulative output for the January-April period totaled 671.3 GWh, an increase of 51%. Output and growth rates of China’s EV batteries from 2014 to April 2026 In terms of sales, combined power and storage battery sales reached 164.2 GWh in April, down 6.2% month-on-month but up 39.0% year-on-year. Power battery sales accounted for 108.9 GWh, representing 66.4% of total sales volume, while energy storage battery sales reached 55.2 GWh. Combined sales for the first four months of the year totaled 601.2 GWh, up 48.9% year-on-year. Exports remained a major growth driver for the industry. China exported 31.7 GWh of power and storage batteries in April, up 42% year-on-year, although exports fell 12.3% from March due to adjustments in export tax rebate policies. Export and growth rates of China’s EV batteries from 2014 to April 2026 Of the total, power battery exports reached 20.2 GWh, while storage battery exports stood at 11.4 GWh. Cumulative exports during January-April reached 115.8 GWh, up 38.1% year-on-year. Driven by continued demand for new energy vehicles, battery installations remained the market’s key indicator. Domestic EV battery installations reached 62.4 GWh in April, up 10.4% month-on-month and 15.2% year-on-year. From a technology perspective, lithium iron phosphate (LFP) batteries continued to strengthen their dominance. China’s battery installations from 2024 to April 2026 LFP battery installations reached 50.8 GWh in April, accounting for 81.5% of the market, while ternary lithium batteries accounted for 11.5 GWh. In the first four months of 2026, cumulative battery installations in China reached 187.2 GWh, up 1.6% year-on-year. LFP batteries accounted for 149.8 GWh, while ternary batteries totaled 37.4 GWh. By vehicle type, battery electric vehicles remained the largest source of battery demand. BEVs accounted for 83% of battery installations in April, compared with 17% for plug-in hybrid vehicles. Industry concentration continued to increase toward leading manufacturers. A total of 34 battery makers achieved installation volumes in April, down six from a year earlier but up three from March. Top 15 battery manufacturers in battery installation volume for April 2026 in China The top 10 companies accounted for 59.2 GWh of installations, representing 94.9% of the market. CATL maintained its dominant position, with April installations reaching 29.06 GWh and a market share of 46.64%. BYD ranked second with 10.49 GWh and a 16.83% market share. Combined, CATL and BYD accounted for 63.47% of China’s EV battery installation market, meaning more than 60% of domestic installations came from the two companies. They were followed by Gotion High-Tech, CALB and EVE Energy, with installation volumes of 4.05 GWh, 3.9 GWh and 3.11 GWh, respectively.