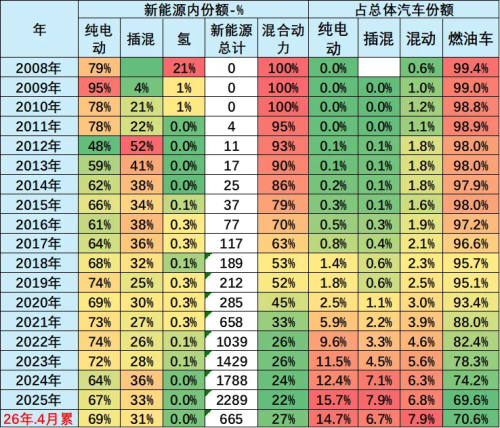

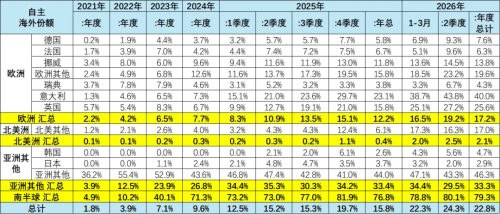

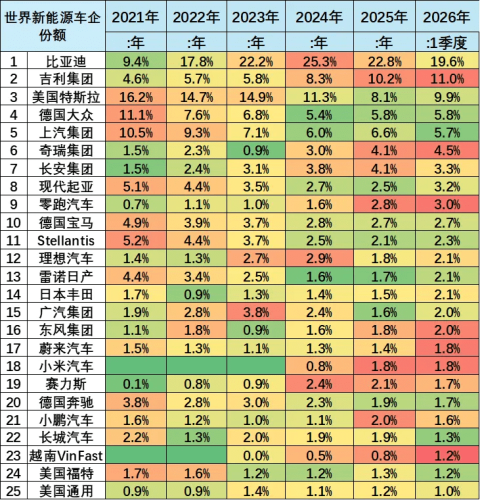

Cui Dongshu, Secretary General of the China Passenger Car Association, released an analysis report on the global new energy vehicle market for January-April 2026. Data shows that after years of rapid growth, the global NEV market is entering a new phase of divergence. China continues to lead the world with over 60% of the global market share, while Europe is seeing a clear recovery. In contrast, the U.S. market is contracting under the dual pressures of subsidy cuts and high tariffs. Global NEV Performance in 2026 According to the data, global total vehicle sales reached 30.96 million units in January-April 2026, of which 6.65 million were new energy vehicles, achieving a penetration rate of 21.4%. By segment, battery electric vehicles (BEVs) accounted for 14.7%, plug-in hybrids (PHEVs) for 6.7%, and conventional hybrids (HEVs) accounted for 7.9% – surpassing PHEVs for the first time. Looking at historical data, global NEV sales reached 17.88 million units in 2024, and further increased to 22.89 million units in 2025, representing a year-on-year growth of 28%. However, growth slowed significantly to around 8% in the first four months of 2026. April alone saw sales of 1.91 million units, up 12% year-on-year – far below the normal levels of previous years. Global Automotive Energy Mix China remains the anchor of the global NEV market. In January-April 2026, China’s share of global new energy passenger vehicle sales reached 61% – 56% for BEVs and as high as 71% for PHEVs. Looking at historical trends, China’s global share of NEV passenger cars peaked at 69% in 2024, then edged down to 68.3% in 2025, and fell to 61% in the first four months of 2026 due to Lunar New Year factors. However, the report notes that this “early-year weakness” is a seasonal fluctuation, and a rebound is expected later. In terms of contribution to global NEV growth, China accounted for 66% of incremental global NEV sales in 2025, followed by Germany (6%) and India (4%). In recent years, China has contributed roughly 70% to 80% of global NEV growth, making it the core battleground for global NEV competition. On penetration rates, China’s cumulative NEV penetration reached 42% in January-April 2026, far exceeding the global average of 21.5%. By comparison, Germany stood at 31%, Norway 80%, the UK 33%, the US only 7%, and Japan only 3% – highlighting stark regional imbalances in global NEV development. Global NEV Passenger Vehicle Performance Meanwhile, the presence of Chinese independent brands in overseas NEV markets is rising rapidly. In 2023, Chinese independent brands held only a 7.1% share of overseas NEV passenger car markets. That rose to 9.6% in 2024, 15.8% in 2025, and further jumped to 22.8% in January-April 2026 – an increase of about 7 percentage points year-on-year. Regionally, Chinese independent brands perform particularly strongly in emerging markets: they hold over 80% of the NEV market share in South America and 46% in Southeast Asia. In Europe, their share has also been steadily increasing, reaching 17.2% of the European market in January-April 2026. Chinese Brands’ Overseas Market Share Looking at the competitive landscape among automakers, the first four months of 2026 saw BYD leading the global NEV market with a 19.6% share, followed by Geely Group (11%) and Tesla (9.9%). In terms of BEV market share, BYD’s share has been on a steady upward trend – rising from 7% in 2021 to 18% in 2025, before dipping to 14.6% in January-April 2026 due to seasonal factors. Tesla’s share has declined from 23% in 2021 to 13.5%. Geely Group’s BEV share has risen from 4% in 2019 to 9% in 2026. NEV Market Share Trends by Manufacturer China also holds an advantage in the PHEV segment. China accounted for 76.4% of the global PHEV market in 2025, and 71% in January-April 2026, with BYD maintaining a roughly 31% share of the global PHEV market, continuing to play a leading role. Notably, the HEV market is heating up again. In 2026, the U.S. accounted for 29% of the global HEV market, while China’s share rebounded to 15.5%. Toyota, Honda, Nissan, and Hyundai together held 84% of the global HEV market, highlighting the continued strength of Japanese and Korean automakers in this segment.