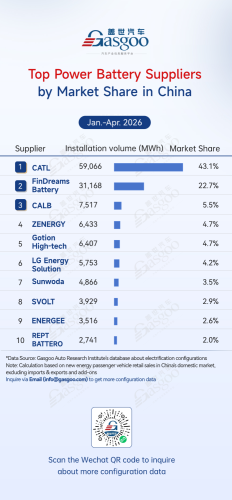

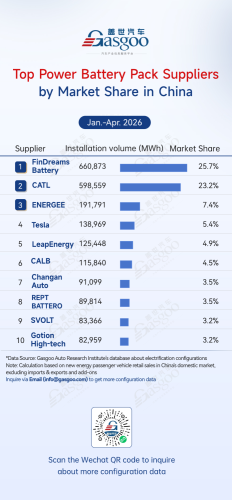

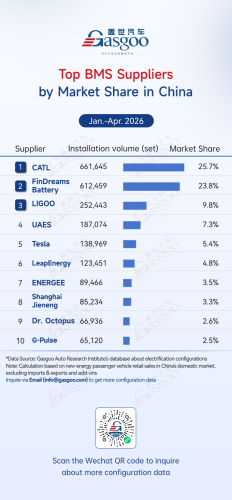

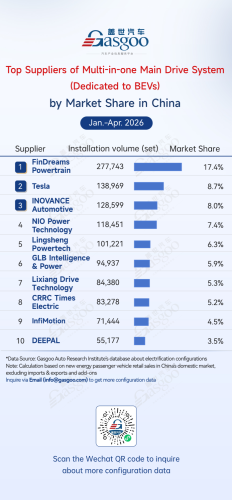

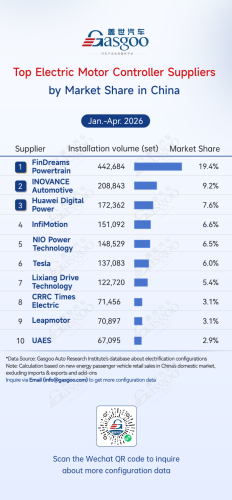

According to data compiled by the Gasgoo Automotive Research Institute, China's new energy rvehicle (NEV) electrification supply chain continued to be characterized by high market concentration and the rapid rise of OEM in-house development during January–April 2026. In key segments such as power batteries and electric drive systems, leading suppliers further strengthened their positions through scale advantages. Meanwhile, in integrated segments including power battery packs and BMS, OEM-developed solutions continued to gain share, reshaping the competitive landscape.Overall, competition is shifting from individual components to system integration, technological capabilities, and in-house development, driving a more diversified market structure.Top power battery suppliersCATL: 59,066 MWh installed, 43.1% market shareFinDreams Battery: 31,168 MWh installed, 22.7% market shareCALB: 7,517 MWh installed, 5.5% market shareZENERGY: 6,433 MWh installed, 4.7% market shareGotion High-tech: 6,407 MWh installed, 4.7% market shareLG Energy Solution: 5,753 MWh installed, 4.2% market shareSunwoda: 4,866 MWh installed, 3.5% market shareSVOLT: 3,929 MWh installed, 2.9% market shareENERGEE: 3,516 MWh installed, 2.6% market shareREPT BATTERO: 2,741 MWh installed, 2.0% market shareFrom January to April 2026, China's power battery market maintained a "dual-leader, multi-tier" competitive landscape. CATL remained the market leader with 59,066 MWh installed (43.1% share), followed by FinDreams Battery with 31,168 MWh and 22.7%. Together, the two companies accounted for more than 65% of the market, reinforcing their dominant positions.Meanwhile, CALB, ZENERGY, and Gotion High-tech formed the second tier, each recording 6,000–8,000 MWh of installed capacity. LG Energy Solution and Sunwoda continued to strengthen their presence through differentiated product strategies. Overall, the market remained highly concentrated with a clearly defined competitive structure.Top power battery pack suppliersFinDreams Battery: 660,873 MWh installed, 25.7% market shareCATL: 598,559 MWh installed, 23.2% market shareENERGEE: 191,791 MWh installed, 7.4% market shareTesla: 138,969 MWh installed, 5.4% market shareLeapEnergy: 125,448 MWh installed, 4.9% market shareCALB: 115,840 MWh installed, 4.5% market shareChangan Auto: 91,099 MWh installed, 3.5% market shareREPT BATTERO: 89,814 MWh installed, 3.5% market shareSVOLT: 83,366 MWh installed, 3.2% market shareGotion High-tech: 82,959 MWh installed, 3.2% market shareChina's power battery pack market was characterized by the coexistence of OEM in-house production and third-party supply during January–April 2026. FinDreams Battery ranked first with 660,873 sets installed (25.7% share), followed by CATL with 598,559 sets installed and 23.2%. Together, the two companies accounted for nearly half of the market.The trend toward OEM-developed battery packs continued to accelerate, with ENERGEE, Tesla, Lingxiao Energy, and Changan Auto all ranking among the top ten. ENERGEE and Tesla held market shares of 7.4% and 5.4%, respectively. Meanwhile, battery suppliers such as CALB and REPT BATTERO maintained stable positions through differentiated OEM partnerships, highlighting a market increasingly defined by head supplier concentration, the rise of OEM in-house production, and a diminishing role for independent third-party pack suppliers.Top BMS suppliersCATL: 661,645 sets installed, 25.7% market shareFinDreams Battery: 612,459 sets installed, 23.8% market shareLIGOO: 252,443 sets installed, 9.8% market shareUAES: 187,074 sets installed, 7.3% market shareTesla: 138,969 sets installed, 5.4% market shareLeapEnergy: 123,451 sets installed, 4.8% market shareENERGEE: 89,466 sets installed, 3.5% market shareShanghai Jieneng: 85,234 sets installed, 3.3% market shareDr. Octopus: 66,936 sets installed, 2.6% market shareG-Pulse: 65,120 sets installed, 2.5% market shareChina's BMS market during January–April 2026 was characterized by two dominant leaders and the rapid rise of OEM-developed solutions. FinDreams Battery ranked first with 661,645 sets installed (25.7% market share), followed by CATL with 612,459 sets installed and 23.8%. Together, the two companies accounted for nearly half of the market, reinforcing their leadership.The trend toward OEM-developed BMS continued to accelerate, with six OEM-affiliated suppliers ranking among the top ten and collectively accounting for more than 45% of the market. Tesla, ENERGEE, and Shanghai Jieneng held market shares of 5.4%, 3.5%, and 3.3%, respectively. Meanwhile, independent suppliers such as LIGOO and UAES maintained solid market positions through their technological strengths, reflecting a market increasingly defined by the parallel development of OEM in-house solutions and third-party suppliers.Top electric drive motor suppliersFinDreams Powertrain: 630,243 sets installed, 23.6% market shareInfiMotion: 269,433 sets installed, 10.1% market shareHuawei Digital Power: 169,433 sets installed, 6.3% market shareINOVANCE Automotive: 157,627 sets installed, 5.9% market shareNIO Power Technology: 148,529 sets installed, 5.6% market shareTesla: 137,083 sets installed, 5.1% market shareGLB Intelligent Power: 94,287 sets installed, 3.5% market shareHYCET: 79,778 sets installed, 3.0% market shareCRRC Times Electric: 72,407 sets installed, 2.7% market shareLingsheng Powertech: 71,258 sets installed, 2.7% market shareFrom January to April 2026, China's electric drive motor market 2026 was characterized by a dominant market leader and an increasingly competitive second tier. FinDreams Powertrain retained the top position with 630,243 sets installed (23.6% share). InfiMotion climbed to second with 269,433 sets installed and a 10.1% share, reshaping the competitive landscape among leading suppliers.Huawei Digital Power, INOVANCE Automotive, and NIO Power Technology followed closely, with market shares ranging from 5% to 7%, alongside OEM-developed suppliers such as Tesla and HYCET, which also maintained solid installation volumes. Overall, the market continues to be defined by strong leadership at the top, intense competition among second-tier suppliers, and the coexistence of OEM in-house production and third-party suppliers.Top suppliers of multi-in-one main drive system (dedicated to BEVs)FinDreams Powertrain: 277,743 sets installed, 17.4% market shareTesla: 138,969 sets installed, 8.7% market shareINOVANCE Automotive: 128,599 sets installed, 8.0% market shareNIO Power Technology: 118,451 sets installed, 7.4% market shareLingsheng Powertech: 101,221 sets installed, 6.3% market shareGLB Intelligence & Power: 94,937 sets installed, 5.9% market shareLixiang Drive Technology: 84,380 sets installed, 5.3% market shareCRRC Times Electric: 83,278 sets installed, 5.2% market shareInfiMotion: 71,444 sets installed, 4.5% market shareDEEPAL: 55,177 sets installed, 3.5% market shareChina's multi-in-one main drive system market for NEV was characterized by a clear market leader and a relatively fragmented competitive landscape during January–April 2026. FinDreams Powertrain ranked first with 277,743 sets installed and a 17.4% market share. Tesla and INOVANCE Automotive followed with 138,969 sets installed (8.7%) and 128,599 sets installed (8.0%), respectively.Compared with individual electric drive components, the all-in-one electric drive system market remains more fragmented. OEM-developed suppliers and third-party vendors—including NIO Power Technology, Lingsheng Powertech, and Lixiang Drive Technology—each held market shares ranging from 3.5% to 7.4%, demonstrating that companies with different technology approaches and supply models have all secured positions in this rapidly evolving segment.Top electric motor controller suppliersFinDreams Powertrain: 442,684 sets installed, 19.4% market shareINOVANCE Automotive: 208,843 sets installed, 9.2% market shareHuawei Digital Power: 172,362 sets installed, 7.6% market shareInfiMotion: 151,092 sets installed, 6.6% market shareNIO Power Technology: 148,529 sets installed, 6.5% market shareTesla: 137,083 sets installed, 6.0% market shareLixiang Drive Technology: 122,720 sets installed, 5.4% market shareCRRC Times Electric: 71,456 sets installed, 3.1% market shareLeapmotor: 70,897 sets installed, 3.1% market shareUAES: 67,095 sets installed, 2.9% market shareFrom January to April 2026, China's electric motor controller market was characterized by a dominant market leader and the rapid rise of OEM-developed solutions. FinDreams Powertrain retained the top position with 634,683 sets installed and a 19.9% market share. INOVANCE Automotive ranked second with 288,762 sets installed (9.0%), followed by InfiMotion with 233,929 sets installed (7.3%).The trend toward OEM-developed motor controllers continued to strengthen, with OEM-affiliated suppliers accounting for half of the top ten rankings and more than 50% of total market share. Overall, the market is characterized by strong leadership at the top, intense multi-tier competition, and the continued expansion of OEM in-house development.