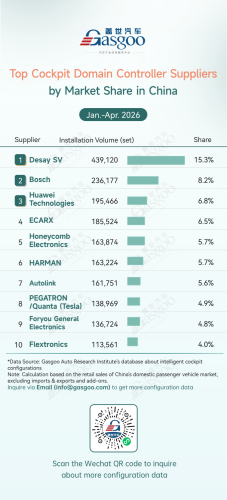

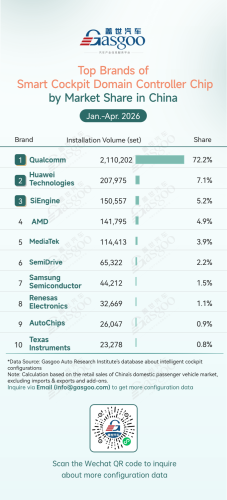

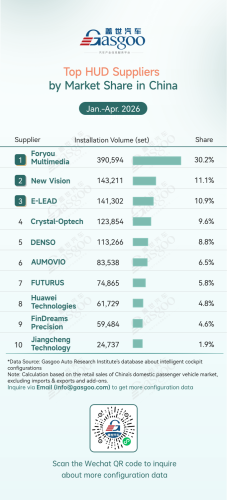

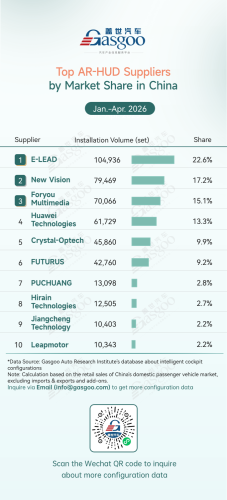

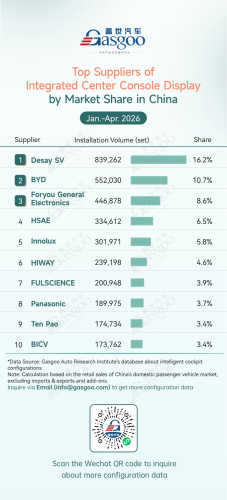

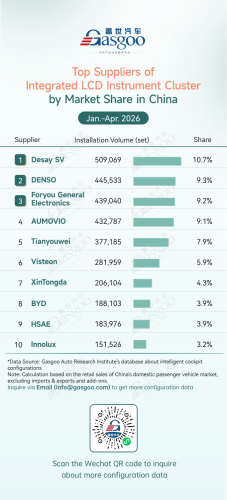

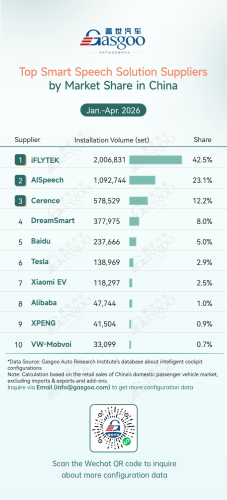

According to data compiled by the Gasgoo Automotive Research Institute, against the backdrop of continued advances in vehicle intelligence and electrification, the smart cockpit has become a key battleground for automakers seeking to differentiate user experience and strengthen market competitiveness. Core segments—including cockpit domain controllers, HUDs, AR-HUDs, and so on—are undergoing simultaneous technological upgrades and competitive restructuring. In domain controllerchip and smart speech solution, market share is becoming increasingly concentrated among leading players, highlighting a "one dominant player with multiple strong challengers" competitive landscape. Meanwhile, the AR-HUD and LCD instrument cluster markets remain highly competitive, with several major suppliers closely matched. Overall, the smart cockpit supply chain is entering a new phase of competition and collaboration.Top cockpit domain controller suppliersDesay SV: 439,120 sets installed, 15.3% market shareBosch: 236,177 sets installed, 8.2% market shareHuawei Technologies: 195,466 sets installed, 6.8% market shareECARX: 185,524 sets installed, 6.5% market shareHoneycomb Electronics: 163,874 sets installed, 5.7% market shareHARMAN: 163,224 sets installed, 5.7% market shareAutolink: 161,751 sets installed, 5.6% market sharePEGATRON /Quanta (Tesla): 138,969 sets installed, 4.9% market shareForyou General Electronics: 136,724 sets installed, 4.8% market shareFlextronics: 113,561 sets installed, 4.0% market shareFrom the January–April 2026 cockpit domain controller supplier rankings, the market continued to be characterized by domestic leadership with multiple competitive tiers. Desay SV ranked first with 439,120 sets installed (15.3% share), further strengthening its leadership through its integrated smart cockpit solutions and large-scale production capabilities. Bosch followed with 236,177 sets installed (8.2%), while Huawei Technologies ranked third with 195,466 sets installed (6.8%). Together, the three suppliers formed the market's leading tier and continued to shape the overall competitive landscape.ECARX, Honeycomb Electronics, HARMAN, Autolink, and PEGATRON/Quanta (Tesla) made up the second tier, with market shares ranging from 4.9% to 6.5%. The relatively narrow gap among these suppliers reflects automakers' growing demand for diverse technology roadmaps and smart cockpit ecosystem solutions.Top brands of smart cockpit domain controller chipQualcomm: 2,110,202 units installed, 72.2% market shareHuawei Technologies: 207,975 units installed, 7.1% market shareSiEngine: 150,557 units installed, 5.2% market shareAMD: 141,795 units installed, 4.9% market shareMediaTek: 114,413 units installed, 3.9% market shareSemiDrive: 65,322 units installed, 2.2% market shareSamsung Semiconductor: 44,212 units installed, 1.5% market shareRenesas Electronics: 32,669 units installed, 1.1% market shareAutoChips: 26,047 units installed, 0.9% market shareTexas Instruments: 23,278 units installed, 0.8% market shareFrom January to April 2026, the cockpit domain controller chip market was characterized by one dominant leader and multiple strong challengers, while China's local substitution continued to gain momentum. Qualcomm maintained its overwhelming leadership with a 72.2% market share, accounting for the vast majority of chip installations and reinforcing its dominant market position. Huawei Technologies ranked second, with installation volumes of its in-house cockpit chips continuing to grow. SiEngine and AMD ranked third and fourth, with 150,557 units installed and 141,795 units installed, respectively. The narrow gap between the two reflects intensifying competition between emerging Chinese chip designers and established global suppliers.MediaTek and SemiDrive occupied the mid-tier, steadily expanding their presence in entry- and mid-range vehicle models. Meanwhile, Samsung Semiconductor, Renesas Electronics, AutoChips, and Texas Instruments all remained in the top ten, maintaining their positions through established customer relationships and strengths in specific market segments.Top HUD suppliersForyou Multimedia: 390,594 sets installed, 30.2% market shareNew Vision: 143,211 sets installed, 11.1% market shareE-LEAD: 141,302 sets installed, 10.9% market shareCrystal-Optech: 123,854 sets installed, 9.6% market shareDENSO: 113,266 sets installed, 8.8% market shareAUMOVIO: 83,538 sets installed, 6.5% market shareFUTURUS: 74,865 sets installed, 5.8% market shareHuawei Technologies: 61,729 sets installed, 4.8% market shareFinDreams Precision: 59,484 sets installed, 4.6% market shareJiangcheng Technology: 24,737 sets installed, 1.9% market shareFrom January to April 2026, China's passenger vehicle HUD market remained firmly dominated by domestic suppliers. Foryou Multimedia ranked first with 390,594 sets installed (30.2% share), establishing a commanding lead and reinforcing its position as the clear market leader. New Vision, E-LEAD, Crystal-Optech, and DENSO formed the second tier, with market shares ranging from 8.8% to 11.1%, reflecting intense competition among the leading challengers.AUMOVIO, FUTURUS, Huawei Technologies, FinDreams Precision, and Hefei Jiangcheng Technology ranked sixth through tenth, with market shares ranging from 6.5% to 1.9%. Among them, Huawei Technologies and FinDreams Precision have been gaining momentum rapidly by leveraging close collaboration within their respective automotive ecosystems.Top AR-HUD suppliersE-LEAD: 104,936 sets installed, 22.6% market shareNew Vision: 79,469 sets installed, 17.2% market shareForyou Multimedia: 70,066 sets installed, 15.1% market shareHuawei Technologies: 61,729 sets installed, 13.3% market shareCrystal-Optech: 45,860 sets installed, 9.9% market shareFUTURUS: 42,760 sets installed, 9.2% market sharePUCHUANG: 13,098 sets installed, 2.8% market shareHirain Technologies: 12,505 sets installed, 2.7% market shareJiangcheng Technology: 10,403 sets installed, 2.2% market shareLeapmotor: 10,343 sets installed, 2.2% market shareFrom the January–April 2026 AR-HUD supplier rankings, the market was characterized by intense competition among multiple leading players, with no clear dominant supplier. E-LEAD ranked first with 104,936 sets installed and a 22.6% market share. New Vision followed with 79,469 sets installed (17.2%), while Foryou Multimedia ranked third with 70,066 sets installed (15.1%). Huawei Technologies placed fourth with 61,729 sets installed and a 13.3% share. Together, the top four suppliers accounted for more than 68% of the market, forming the industry's core competitive group.Crystal-Optech and FUTURUS ranked fifth and sixth with 45,860 sets installed (9.9%) and 42,760 sets installed (9.2%), respectively, representing a solid second tier. PUCHUANG, Hirain Technologies, Hefei Jiangcheng Technology, and Leapmotor ranked seventh through tenth, each holding market shares between 2.2% and 2.8%. Although their current volumes remain relatively modest, these emerging suppliers and OEM-developed solutions have established a meaningful presence in the AR-HUD market.Top suppliers of integrated center console displayDesay SV: 839,262 sets installed, 16.2% market shareBYD: 552,030 sets installed, 10.7% market shareForyou General Electronics: 446,878 sets installed, 8.6% market shareHSAE: 334,612 sets installed, 6.5% market shareInnolux: 301,971 sets installed, 5.8% market shareHIWAY: 239,198 sets installed, 4.6% market shareFULSCIENCE: 200,948 sets installed, 3.9% market sharePanasonic: 189,975 sets installed, 3.7% market shareTen Pao: 174,734 sets installed, 3.4% market shareBICV: 173,762 sets installed, 3.4% market shareFrom January to April 2026, the China's integrated center console displaymarket remained dominated by local suppliers. Desay SV ranked first with 839,262 sets installed (16.2% share), maintaining a clear lead and demonstrating strong capabilities in center display integration and large-scale OEM supply. BYD, supported by its in-house development and manufacturing model, ranked second, while Foryou General Electronics placed third, underscoring the strong presence of China's local suppliers at the top of the market.HSAE and Innolux formed the mid-tier, serving both traditional automakers and emerging EV brands. HIWAY, FULSCIENCE, and Panasonic held comparable market shares, highlighting continued competition between China's local and global suppliers. Ten Pao and BICV rounded out the top ten, supported by stable mass-production capabilities and long-standing customer relationships.Top suppliers of integrated LCD instrument clusterDesay SV: 509,069 sets installed, 10.7% market shareDENSO: 445,533 sets installed, 9.3% market shareForyou General Electronics: 439,040 sets installed, 9.2% market shareAUMOVIO: 432,787 sets installed, 9.1% market shareTianyouwei: 377,185 sets installed, 7.9% market shareVisteon: 281,959 sets installed, 5.9% market shareXinTongda: 206,104 sets installed, 4.3% market shareBYD: 188,103 sets installed, 3.9% market shareHSAE: 183,976 sets installed, 3.9% market shareInnolux: 151,526 sets installed, 3.2% market shareFrom January to April 2026 LCD instrument cluster supplier rankings, the market exhibited a highly competitive yet relatively fragmented landscape. Desay SV ranked first with 509,069 sets installed (10.7% share). DENSO, Foryou General Electronics, and AUMOVIO followed closely, with 445,533, 439,040, and 432,787 sets installed, respectively. Each held a market share of around 9%, leaving only a narrow gap among the top four suppliers and highlighting the intense level of competition.Meanwhile, Tianyouwei and Visteon formed the second tier with market shares of 7.9% and 5.9%, respectively. Together, they accounted for more than 13% of the market, reinforcing their positions as important players in the LCD instrument cluster segment.Top smart speech solution suppliersiFLYTEK: 2,006,831 sets installed, 42.5% market shareAISpeech: 1,092,744 sets installed, 23.1% market shareCerence: 578,529 sets installed, 12.2% market shareDreamSmart: 377,975 sets installed, 8.0% market shareBaidu: 237,666 sets installed, 5.0% market shareTesla: 138,969 sets installed, 2.9% market shareXiaomi EV: 118,297 sets installed, 2.5% market shareAlibaba: 47,744 sets installed, 1.0% market shareXPENG: 41,504 sets installed, 0.9% market shareVW-Mobvoi: 33,099 sets installed, 0.7% market shareFrom January to April 2026, China's passenger vehicle smart speech solution supplier market exhibited a highly concentrated competitive landscape dominated by two leading players. iFLYTEK maintained its leading position with 2,006,831 sets installed (42.5% share), accounting for nearly half of the market and reinforcing its dominant industry position. AISpeech ranked second with 1,092,744 sets installed (23.1% share). Together, the two companies captured more than 65% of the market, forming a clear first-tier group. Cerence ranked third with 578,529 sets installed (12.2%), remaining the only global supplier among the top three.DreamSmart and Baidu ranked fourth and fifth with 377,975 sets installed (8.0%) and 237,666 sets installed (5.0%), respectively, forming the second tier. Notably, OEM-developed voice solutions from Tesla (2.9%), Xiaomi EV (2.5%), and XPENG (0.9%) also entered the top ten, reflecting a growing trend among NEV manufacturers to bring smart speech solution technologies in-house as part of their self-developed intelligent cockpit ecosystems.

![Smart, CarNewsChina introduces smart newsletter for its readers [new CNC feature]](https://cdn.topcarnews.net/thumb/id/aHR0cHM6Ly9jYXJuZXdzY2hpbmEuY29t-L3dwLWNvbnRlbnQvdXBsb2Fkcy8yMDI2-LzA3L25ld3NsZXR0ZXItMS5qcGc/f2d591743a8b921b50d8fff9a705ad9a.jpg?t=20260811&post_id=49158)

![Smart, CarNewsChina introduces smart newsletter for its readers [new CNC feature]](https://cdn.topcarnews.net/thumb/id/aHR0cHM6Ly9jYXJuZXdzY2hpbmEuY29t-L3dwLWNvbnRlbnQvdXBsb2Fkcy8yMDI2-LzA3L25ld3NsZXR0ZXIuanBn/423a2f6b9180da0e013301c4c4af3962.jpg?t=20260811&post_id=49158)