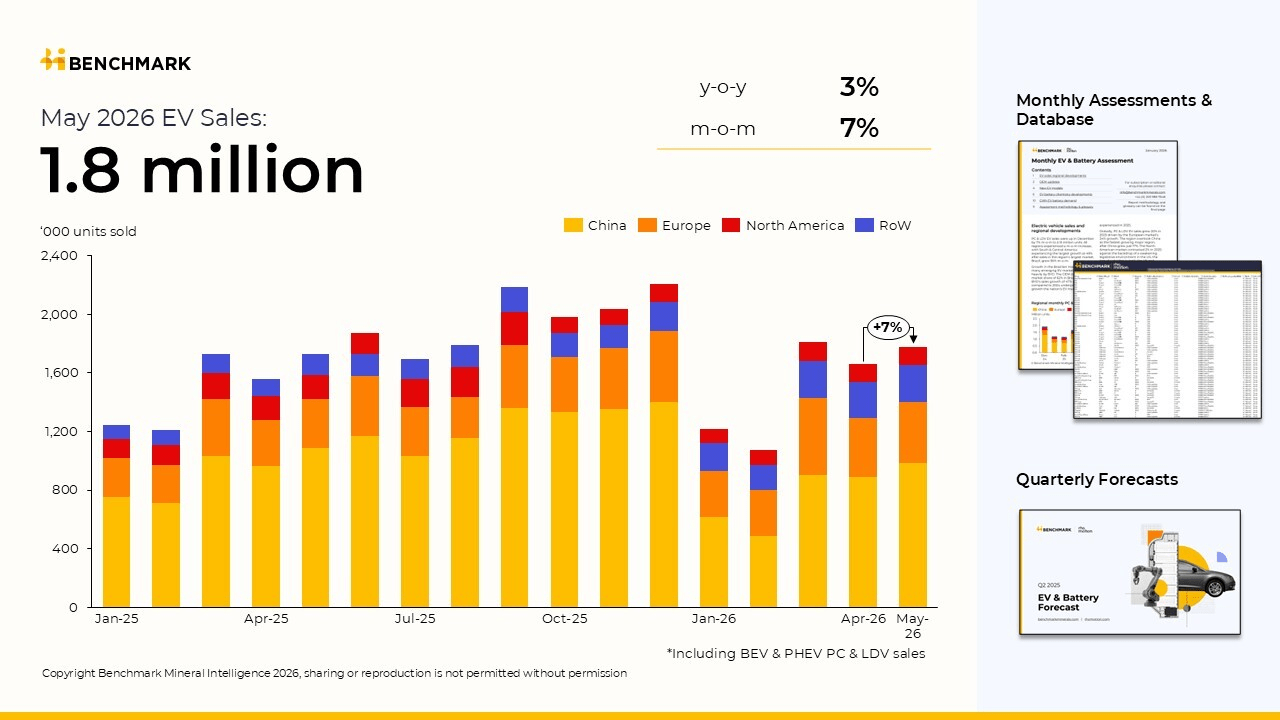

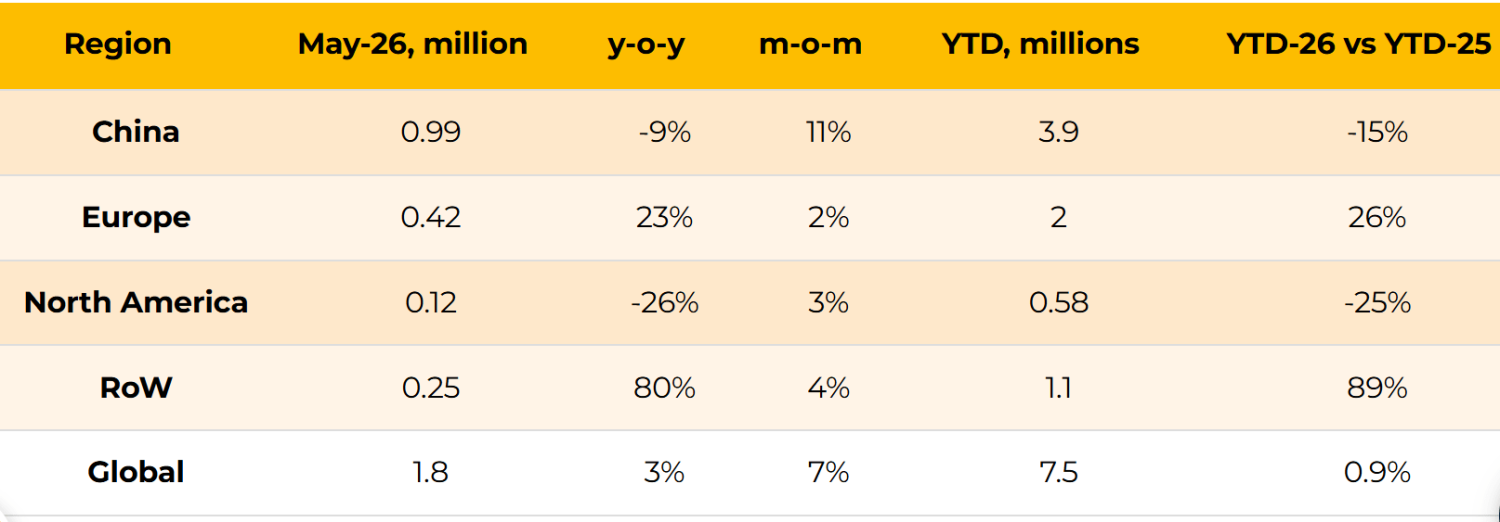

Benchmark Mineral Intelligence (BMI) data show global electric vehicle sales reached approximately 1.8 million units in May, up 3% year-on-year and 7% month-on-month. For the first five months of the year, cumulative global EV sales totaled around 7.5 million units, with growth easing to 0.9% year-on-year, indicating a market still in a low-speed recovery phase. Global EV sales in May 2026 Regional performance continues to diverge. China remains the largest single market, though domestic demand remains under pressure. In May, EV sales in China stood at approximately 990,000 units, down 9% year-on-year but up 11% month-on-month, accounting for roughly 55% of global sales. On a year-to-date basis, China’s EV sales have declined about 15% to 3.9 million units, with earlier demand weakness weighing on overall performance. In contrast, China’s export performance continues to strengthen. In May, EV exports approached 450,000 units, setting a new record, with both battery electric vehicles (BEVs) and plug-in hybrid electric vehicles (PHEVs) maintaining growth momentum. The trend of automakers using overseas markets to absorb domestic excess capacity has intensified this year, making exports a key stabilizing factor for the sector. Global EV sales across different regions in May 2026 and YTD Europe continued to post relatively strong growth. EV sales in May reached approximately 420,000 units, up 23% year-on-year and 2% month-on-month. Year-to-date sales increased 26% to around 2 million units, significantly outpacing the global average. Ongoing subsidy support, combined with higher oil prices driven by geopolitical tensions in the Middle East, remained key demand drivers. Notably, the share of Chinese-made EVs in Europe continued to rise. In 2025, Chinese brands accounted for around 19% of Europe’s EV market. Heading into 2026, this share has continued to increase despite tightening EU tariff measures. In the UK market, Chinese-origin models account for 32%, compared with 14% in Germany and 10% in France. As penetration of Chinese EVs in Europe expands, automakers including Dongfeng Motor and Leapmotor have announced plans to utilize underused European manufacturing capacity to establish localized production. Leapmotor T03 and C10 In contrast, the North American market remains weak. EV sales in May fell 26% year-on-year to around 120,000 units, while year-to-date volumes declined 25% to 580,000 units. The expiration of tax credit incentives and a slowdown in automaker electrification strategies are cited as key factors. Canada’s tariff quota system for Chinese EVs has created limited market access opportunities. It allows up to 49,000 units of Chinese-made EVs annually under preferential tariff treatment, replacing the previous 100% additional tariff regime. Against this shifting policy and market backdrop, Chinese automakers are accelerating overseas expansion. BYD announced plans to enter the Canadian market by the end of 2026, targeting more than 20 dealerships across Toronto, Vancouver, Montreal, and Calgary, with initial models including the Yuan Plus, Seal, Dolphin, and Seagull.