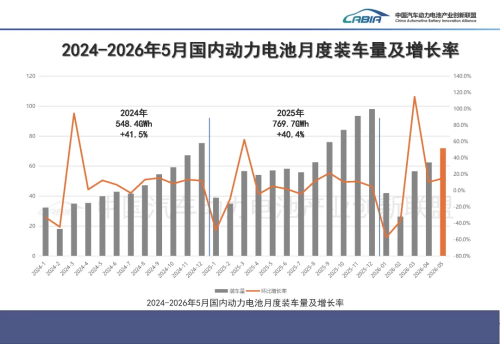

China’s Automotive Battery Innovation Alliance (CABIA) released its monthly battery industry report on June 11, showing continued growth across production, sales and installations in May 2026. Data showed that China’s combined production of power batteries and energy storage batteries reached 191.7 GWh in May, up 55.2% year-on-year and 4.2% from April. Cumulative production for January-May totaled 863 GWh, representing a 51.9% increase from a year earlier. Production and growth rates of China’s EV batteries from 2014 to May 2026 Total sales of power and energy storage batteries reached 182.2 GWh in May, up 11.0% month-on-month and 47.4% year-on-year. Of the total, power battery sales amounted to 127 GWh, accounting for 69.7% of overall battery sales, while energy storage battery sales reached 55.2 GWh. Combined sales for the first five months of the year totaled 783.4 GWh, up 48.5% year-on-year. Exports remained a key growth driver for the industry. China exported 29.3 GWh of power and energy storage batteries in May, up 42% year-on-year, although down 7.6% from April. Export and growth rates of China’s EV batteries from 2014 to May 2026 Power battery exports accounted for 20.1 GWh, while energy storage battery exports totaled 9.2 GWh. Cumulative battery exports during January-May reached 145.1 GWh, an increase of 41% from the same period last year. China’s new energy vehicle (NEV) market also maintained strong momentum in May. NEV production and sales reached 1.554 million and 1.496 million units, up 22.4% and 14.4% year-on-year respectively. NEVs accounted for 56.9% of total new vehicle sales during the month. Supported by robust NEV demand, domestic power battery installations continued to expand. Power battery installations reached 71.9 GWh in May, up 15.2% from April and 25.9% year-on-year. China’s EV battery installations and growth rates from 2024 to May 2026 From a technology perspective, lithium iron phosphate (LFP) batteries further strengthened their dominance. LFP battery installations reached 58.4 GWh in May, accounting for 81.2% of total installations, while ternary batteries recorded 13.4 GWh. During the first five months of 2026, cumulative domestic power battery installations reached 259.1 GWh, up 7.3% year-on-year. LFP batteries contributed 208.2 GWh, while ternary batteries accounted for 50.8 GWh. By vehicle type, battery electric vehicles (BEVs) remained the largest source of battery demand, accounting for 84.6% of installations in May, compared with 15.4% for plug-in hybrid vehicles. Industry concentration continued to increase. A total of 33 battery manufacturers supplied installed capacity during May, four fewer than a year earlier and one fewer than in April. China’s Top 15 battery manufacturers in battery installation volume in May 2026 The top 10 suppliers collectively accounted for 67.4 GWh of installations, representing 93.8% of the market. Contemporary Amperex Technology Co. Limited (CATL) maintained a commanding lead with 33.08 GWh of installed capacity in May, equivalent to a 46.14% market share. BYD ranked second with 11.87 GWh and a 16.56% market share. Together, CATL and BYD accounted for 62.7% of China’s power battery installation market, meaning more than six out of every 10 batteries installed in Chinese NEVs came from the two companies. They were followed by Gotion High-Tech, CALB and EVE Energy, which recorded power battery installations of 4.44 GWh, 4.30 GWh and 3.23 GWh respectively during the month.

![BYD confirms new flagship EV has a range of 1,008 km [Video]](https://cdn.topcarnews.net/thumb/id/aHR0cHM6Ly9pMC53cC5jb20vZWxlY3Ry-ZWsuY28vd3AtY29udGVudC91cGxvYWRz-L3NpdGVzLzMvMjAyNi8wNy9CWUQtR3Jl-YXQtSGFuLUZsYWdzaGlwLUVWLmpwZWc_-dz0xNTAwJmFtcDtxdWFsaXR5PTgyJmFt-cDtzdHJpcD1hbGwmYW1wO3NzbD0x/c37374468f3a539ee1e0ce2b627e08d0.jpeg?t=20260724&post_id=48318)