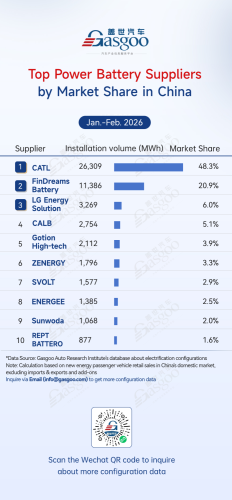

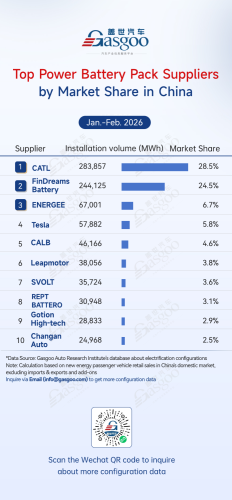

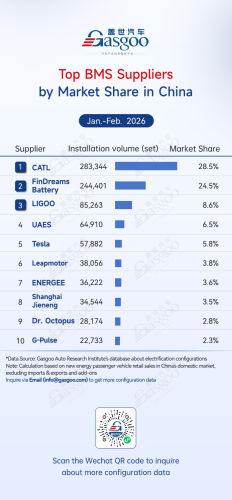

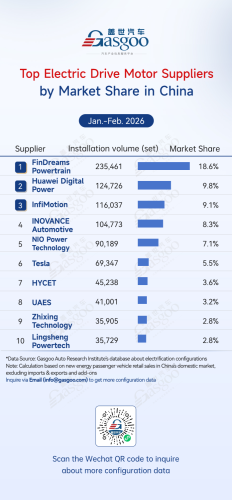

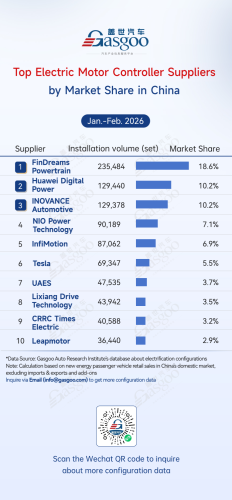

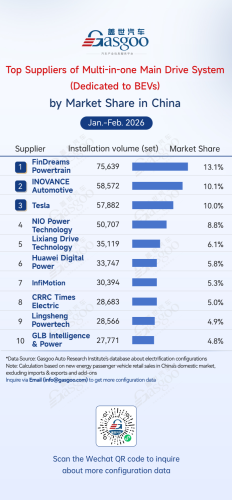

According to data compiled by the Gasgoo Automotive Research Institute, China's new energy vehicle (NEV) electrification core segments from January to February 2026 continued to show a pattern of entrenched leadership and intensifying tiered competition.Across six key areas—power batteries, power battery packs, BMS, electric drive motors, electrical motor controllers, and power semiconductor device (dedicated to e-drive)—installation data highlights a clear trend: industry resources are increasingly concentrated in leading companies with full-chain capabilities, strong technological barriers, and large-scale supply capacity. At the same time, two development paths—automakers' vertical integration and specialized suppliers—are evolving in parallel with growing divergence.Top power battery suppliersCATL: 26,309 MWh installed capacity, 48.3% market shareFinDreams Battery: 11,386 MWh installed capacity, 20.9% market shareLG Energy Solution: 3,269 MWh installed capacity, 6.0% market shareCALB: 2,754 MWh installed capacity, 5.1% market shareGotion High-tech: 2,112 MWh installed capacity, 3.9% market shareZENERGY: 1,796 MWh installed capacity, 3.3% market shareSVOLT: 1,577 MWh installed capacity, 2.9% market shareENERGEE: 1,385 MWh installed capacity, 2.5% market shareSunwoda: 1,068 MWh installed capacity, 2.0% market shareREPT BATTERO: 877 MWh installed capacity, 1.6% market shareFrom the January to February 2026, China's power battery market continued to show a "one dominant player with several strong followers" structure, with leading players further strengthening their positions. CATL ranked first with a 48.3% market share and 26,309 MWh installed, leveraging its full value chain integration, technological iteration, and large-scale capacity to reinforce its leadership and remain the core driver of battery installations in China.FinDreams Battery followed with 11,386 MWh installed (20.9% share). Supported by its deep integration with BYD and strong vertical integration capabilities, it maintained steady growth, although its installation volume faced some pressure amid a slowdown in BYD’s vehicle sales growth.Top power battery pack suppliersCATL: 283,857 sets installed, 28.5% market shareFinDreams Battery: 244,125 sets installed, 24.5% market shareENERGEE: 67,001 sets installed, 6.7% market shareTesla: 57,882 sets installed, 5.8% market shareCALB: 46,166 sets installed, 4.6% market shareLeapmotor: 38,056 sets installed, 3.8% market shareSVOLT: 35,724 sets installed, 3.6% market shareREPT BATTERO: 30,948 sets installed, 3.1% market shareGotion High-tech: 28,833 sets installed, 2.9% market shareChangan Auto: 24,968 sets installed, 2.5% market shareFrom January to February 2026, the power battery pack market continued to show a "dual-leader with tiered differentiation" pattern, with the top two suppliers accounting for over 53% combined, indicating high industry concentration. CATL ranked first with a 28.5% market share and 283,857 sets installed, maintaining its lead over FinDreams Battery. Leveraging strengths in standardized PACK solutions, technical adaptability, and large-scale supply capabilities, CATL continues to expand its coverage among mainstream OEMs. FinDreams Battery followed with 244,125 sets installed (24.5% share), supported by BYD's vertically integrated model, which ensures stable internal demand and strong organic growth momentum.Top BMS suppliersCATL: 283,344 sets installed, 28.5% market shareFinDreams Battery: 244,401 sets installed, 24.5% market shareLIGOO: 85,263 sets installed, 8.6% market shareUAES: 64,910 sets installed, 6.5% market shareTesla: 57,882 sets installed, 5.8% market shareLeapmotor: 38,056 sets installed, 3.8% market shareENERGEE: 36,222 sets installed, 3.6% market shareShanghai Jieneng: 34,544 sets installed, 3.5% market shareDr. Octopus: 28,174 sets installed, 2.8% market shareG-Pulse: 22,733 sets installed, 2.3% market shareFrom the Jan–Feb 2026 BMS installation data, the market is characterized by high concentration at the top, clear tier differentiation, and accelerating OEM in-house development. CATL ranked first with a 28.5% market share and 283,344 sets installed, leveraging its strong expertise in battery management and full value chain integration to achieve broad coverage across mainstream OEMs, making it the core player in the market. FinDreams Battery followed with 244,401 sets installed (24.5% share). Supported by BYD's vertically integrated model, its in-house BMS is deeply integrated with its vehicle lineup, sustaining strong organic growth momentum.Top electric drive motor suppliersFinDreams Powertrain: 235,461 sets installed, 18.6% market shareHuawei Digital Energy: 124,726 sets installed, 9.8% market shareStarDrive Technology: 116,037 sets installed, 9.1% market shareInovance Automotive: 104,773 sets installed, 8.3% market shareNIO Power Technology: 90,189 sets installed, 7.1% market shareTesla: 69,347 sets installed, 5.5% market shareHoneycomb Easy Creation: 45,238 sets installed, 3.6% market shareUAES: 41,001 sets installed, 3.2% market shareZhixin Technology: 35,905 sets installed, 2.8% market shareLingsheng Powertrain: 35,729 sets installed, 2.8% market shareFrom the Jan.–Feb. 2026 drive motor supplier landscape, the market shows a pattern of tiered differentiation, with OEM in-house production and specialized suppliers developing in parallel. FinDreams Powertrain ranked first with 235,461 sets installed (18.6% share), leveraging BYD's vertically integrated model. Its drive motors are deeply integrated with vehicle platforms, giving it clear advantages in large-scale supply and cost control. Huawei Digital Power, StarDrive Technology, INOVANCE Automotive, and NIO Power Technology followed, forming the core competitive tier of the market.Top electric motor controller suppliersFinDreams Powertrain: 235,484 sets installed, 18.6% market shareHuawei Digital Power: 129,440 sets installed, 10.2% market shareINOVANCE Automotive: 129,378 sets installed, 10.2% market shareNIO Power Technology: 90,189 sets installed, 7.1% market shareInfiMotion: 87,062 sets installed, 6.9% market shareTesla: 69,347 sets installed, 5.5% market shareUAES: 47,535 sets installed, 3.7% market shareLi Auto Drive Technology: 43,942 sets installed, 3.5% market shareCRRC Times Electric: 40,588 sets installed, 3.2% market shareLeapmotor: 36,440 sets installed, 2.9% market shareFrom the Jan–Feb 2026 motor controller data, the market shows a mix of OEM in-house production and specialized suppliers. FinDreams Powertrain ranked first with an 18.6% share and 235,484 sets, leveraging strong integration with BYD's platforms and advantages in scale and cost control. Huawei Digital Power and INOVANCE Automotive followed, both at 10.2%, competing closely with strengths in power electronics and system integration. Notably, OEM-affiliated players account for over 44% of the top ten, highlighting the growing role of in-house development in e-drive systems.Top suppliers of power semiconductor device (dedicated to e-drive)FinDreams Powertrain: 75,639 sets installed, 13.1% market shareINOVANCE Automotive: 58,572 sets installed, 10.1% market shareTesla: 57,882 sets installed, 10.0% market shareNIO Power Technology: 50,707 sets installed, 8.8% market shareLi Auto Drive Technology: 35,119 sets installed, 6.1% market shareHuawei Digital Power: 33,747 sets installed, 5.8% market shareInfiMotion: 30,394 sets installed, 5.3% market shareCRRC Times Electric: 28,683 sets installed, 5.0% market shareLingsheng Powertech: 28,566 sets installed, 4.9% market shareGLB Intelligence & Power: 27,771 sets installed, 4.8% market shareFrom January to February 2026, the power semiconductor device (dedicated to e-drive market appears more fragmented compared to the drive motor segment. FinDreams Powertrain ranked first with a 13.1% market share and 75,639 sets installed, leveraging BYD's vertical integration to maintain advantages in system integration, cost efficiency, and large-scale application. INOVANCE Automotive followed with 58,572 sets (10.1% share), while Tesla ranked third with 57,882 sets (10.0% share). The top three together accounted for over 33% of the market, forming the leading group.