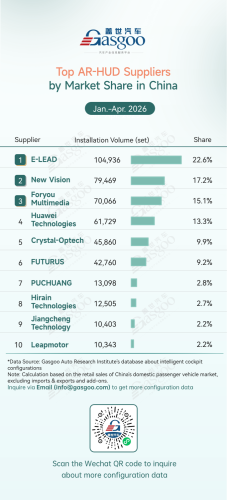

Over the past few years, automotive intelligence in China has been undergoing a profound transition from "functional availability" to "experience-driven value."Around 2022, industry efforts were largely focused on the mass deployment of advanced driver assistance systems (ADAS), upgrades in cockpit display technologies, and the rapid adoption of intelligent features. By 2026, however, competition has increasingly shifted toward user experience, system integration, and real-world performance.During this transition, functions such as Highway NOA (Navigate on Autopilot), Urban NOA, and memory parking have seen accelerated adoption, bringing advanced driving capabilities to a broader range of vehicles. At the same time, the continued evolution of large language models (LLMs), multimodal interaction, and cockpit-driving integration is transforming the smart cockpit from an information interface into a proactive service platform. As a result, the boundaries between intelligent driving and smart cockpit systems are becoming increasingly blurred, with vehicle intelligence evolving toward a more integrated and collaborative architecture.Against this backdrop, ADAS/AD and smart cockpit technologies have become two of the most dynamic and competitive areas of innovation in China's automotive industry.From scale expansion to capability competitionAccording to data compiled by the Gasgoo Automotive Research Institute, penetration rates of ADAS/AD and smart cockpit technologies in China's passenger vehicle market have continued to rise in recent years, with automotive intelligence rapidly expanding from premium models into the mass market.From January to April 2026, China's passenger vehicle ADAS component market maintained strong growth momentum, with installation volumes increasing steadily across key segments. China's local suppliers have gradually established leading positions in areas such as LiDAR, air suspension system, HD maps, and high recision positioning, while market concentration continues to increase.Among these segments, the LiDAR market posted particularly strong growth and has evolved into a clear two-horse race. Hesai Technology ranked first with 456,986 units installed (35.0% share), while Huawei Technologies followed closely with 398,057 units (30.5% share). Together, the two companies accounted for 65.5% of total installations, playing a pivotal role in accelerating the large-scale deployment of advanced intelligent driving systems.The smart cockpit sector has also maintained strong growth momentum. As consumer expectations for interactive experiences, information display, and intelligent services continue to rise, key segments such as HUDs, AR-HUDs, cockpit domain controllers, domain controller chips, center displays, and smart speech solutions are undergoing rapid upgrades.The AR-HUD market provides a representative example. From January to April 2026, E-LEAD ranked first with 104,936 sets installed (22.6% share). New Vision, Foryou Multimedia, and Huawei Technologies followed closely behind. Together, the top four suppliers accounted for more than 68% of the market, highlighting an increasingly concentrated yet highly competitive landscape led by multiple major players.From a technology evolution perspective, the focus of industry competition is also shifting. Intelligent driving has moved beyond competition based on standalone features and is increasingly centered on overall system capabilities. Leading suppliers are evolving from hardware-focused providers into developers of domain controllers, algorithm platforms, and full-stack solutions, leveraging software-hardware integration to enhance system performance and development efficiency.Meanwhile, the smart cockpit is transitioning from a phase centered on display and voice-function upgrades to one driven by AI-powered experience transformation. Large language model (LLM)-based interaction, multimodal perception, cross-device ecosystem integration, and AI agent applications are being rapidly adopted, accelerating the evolution of the cockpit from an information interface into an intelligent service platform.Against this backdrop, competitive differentiation is increasingly defined by measurable system capabilities and real-world performance across diverse user scenarios.For the intelligent driving sector, evaluation criteria have shifted from feature availability to real-world performance. As functions such as Urban NOA and memory parking gain wider adoption, greater emphasis is being placed on a system's ability to handle complex scenarios and maintain operational stability. Key metrics now include long-tail scenario handling, driver takeover frequency, path-planning reliability, and end-to-end response efficiency. At the same time, as ADAS move into the mass market, cost optimization and large-scale production capabilities have become critical competitive factors.The same trend is evident in the smart cockpit sector. With the growing adoption of large language models (LLMs) and multimodal interaction technologies, competition is increasingly focused on user experience quality and system collaboration efficiency. Important indicators include voice recognition accuracy, interaction latency, multi-application coordination, cross-ecosystem integration, and OTA update efficiency. Looking ahead, competition is expected to extend further into AI agent capabilities and proactive service functions, driving the next phase of cockpit intelligence.Building on these trends, the convergence of intelligent driving and smart cockpit technologies is reshaping the system architecture of smart vehicles. ADAS and smart cockpit systems are evolving from relatively independent functional domains toward coordinated optimization at the computing platform, data pipeline, and software stack levels. With the development of centralized computing platforms and domain-integrated architectures, cross-domain resource allocation and unified system capabilities are emerging as key directions for technological advancement, providing new pathways to improve both system efficiency and the consistency of the in-vehicle user experience.Among this year's award submissions, an increasing number of companies are focusing their innovations on addressing real industry needs. Innovations that combine technological breakthroughs with tangible industry value are precisely the type of achievements highlighted by this year's Gasgoo Awards.For the judging panel, leading technical specifications remain important, but a technology's ability to address industry challenges, achieve mass production, and create real-world value is equally critical. Whether improving the safety and reliability of intelligent driving systems or enhancing the user experience of smart cockpits, innovations that drive industry progress and deliver meaningful benefits to end users will receive the greatest recognition.Gasgoo Awards 2026 & China Automotive Industry Innovation CasebookThe Gasgoo Awards was initiated by Gasgoo, aiming at "promoting outstanding companies, propagate Innovative technologies, and facilitate the success of automotive professionals." With the theme of "Top 100 Players of China's New Automotive Supply Chain", It focuses on ten sub - sectors: Advanced Driver Assistance Systems/Autonomous Driving (ADAS/AD), smart cockpit, intelligent chassis, automotive software and artificial intelligence, automotive-grade chips, powertrain and charging and battery swapping, body and interior and exterior trim,new materials and advanced manufacturing, embodied Intelligence and cross-industry technologies (new focus area). The Gasgoo Awards is committed to identifying and evaluating outstanding enterprises and advanced technical solutions. By presenting these remarkable enterprises and industry leaders to the academic community and the broader industry, it aims to jointly drive the sustainable development and advancement of China's automotive industry.Leveraging a supply chain database covering more than 320,000 companies, as well as years of industry research and innovation case studies accumulated through the Gasgoo Awards, Gasgoo has officially launched the China Automotive Industry Innovation Casebook. The initiative aims to document China's automotive innovation journey and serve as a global window into the country's technological and industrial capabilities.Focusing on key sectors such as ADAS, electric propulsion, intelligent cockpits, and thermal management, the Casebook will provide data-driven insights into leading companies, technology trends, and industry best practices. It is designed to help global OEMs, Tier 1 suppliers, and investors better understand the innovation, engineering, and mass-production capabilities of Chinese automotive suppliers, while supporting deeper international collaboration across the industry.