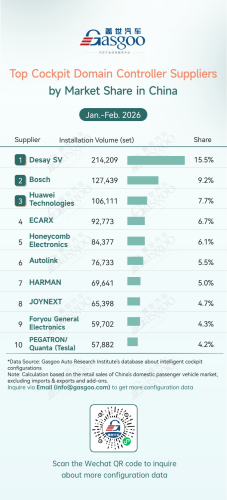

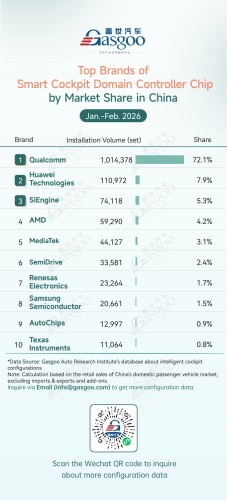

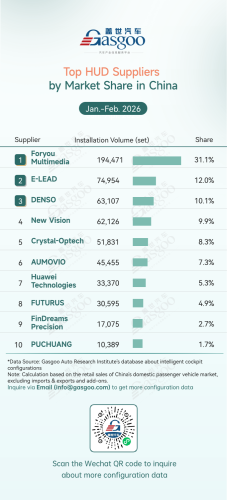

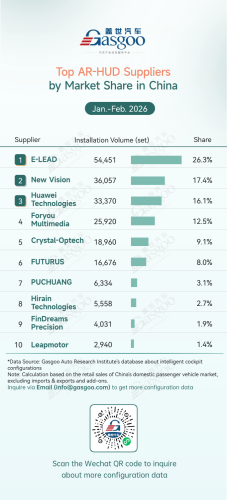

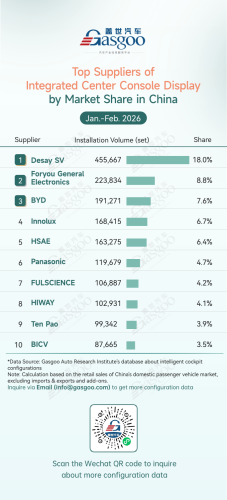

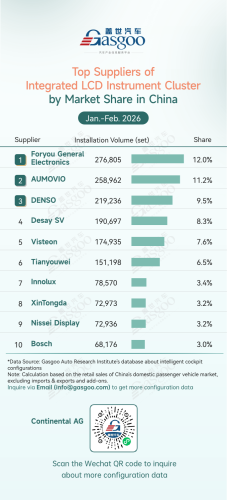

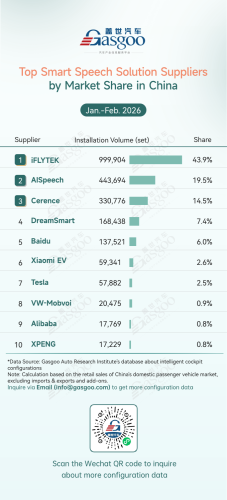

According to Gasgoo Research Institute, as automotive intelligence and electrification continue to deepen, the smart cockpit has become a core battlefield for automakers to differentiate products and enhance user experience. Key segments such as cockpit domain controllers, domain control chips, HUDs, in-vehicle displays, and voice systems are undergoing simultaneous technological upgrades and structural reshaping.The January–February 2026 installation rankings across sub-segments show the strong rise of domestic supply chains and diverging concentration among leading players, marking a new phase of competition in the smart cockpit ecosystem.Top cockpit domain controller suppliersDesay SV: 214,209 sets installed, 15.5% market shareBosch: 127,439 sets installed, 9.2% market shareHuawei Technologies: 106,111 sets installed, 7.7% market shareECARX: 92,773 sets installed, 6.7% market shareHoneycomb Electronics: 84,377 sets installed, 6.1% market shareAutolink: 76,733 sets installed, 5.5% market shareHARMAN: 69,641 sets installed, 5.0% market shareJOYNEXT: 65,398 sets installed, 4.7% market shareForyou General Electronics: 59,702 sets installed, 4.3% market sharePEGATRON/Quanta (Tesla): 57,882 sets installed, 4.2% market shareFrom January to February 2026, Desay SV led the cockpit domain controller market with 214,209 sets installed and a 15.5% share, significantly ahead of its peers. Bosch (127,439 sets installed, 9.2%) and Huawei Technologies (106,111 sets installed, 7.7%) ranked second and third, respectively. Mid-tier suppliers such as ECARX, Honeycomb Electronics, Autolink, and HARMAN held shares between 5% and 7%, reflecting a relatively balanced competitive landscape. JOYNEXT, Foryou General Electronics, and PEGATRON/Quanta (Tesla) also entered the top ten with individual shares above 4%, indicating a moderately concentrated market where leading players maintain clear advantages, while others seek growth through innovation and strategic partnerships.Top brands of smart cockpit domain controller chipQualcomm: 1,014,378 units installed, 72.1% market shareHuawei Technologies: 110,972 units installed, 7.9% market shareSiEngine: 74,118 units installed, 5.3% market shareAMD: 59,290 units installed, 4.2% market shareMediaTek: 44,127 units installed, 3.1% market shareSemiDrive: 33,581 units installed, 2.4% market shareRenesas Electronics: 23,264 units installed, 1.7% market shareSamsung Semiconductor: 20,661 units installed, 1.5% market shareAutoChips: 12,997 units installed, 0.9% market shareTexas Instruments: 11,064 units installed, 0.8% market shareFrom January to February 2026, the cockpit domain controller chip market showed high concentration at the top alongside a rising share of domestic players. Qualcomm dominated with 1.01 million units installed and a 72.1% market share, forming a clear "single-leader" structure. Huawei Technologies and SiEngine ranked second and third with shares of 7.9% and 5.3%, respectively, as domestic chipmakers accelerated large-scale vehicle adoption. Meanwhile, AMD, MediaTek, and SemiDrive held shares in the 2%–4.5% range, competing in a crowded mid-tier, while Renesas Electronics, Samsung Semiconductor, AutoChips, and Texas Instruments also secured top-ten positions.Top HUD suppliersForyou Multimedia: 194,471 sets installed, 31.1% market shareE-LEAD: 74,954 sets installed, 12.0% market shareDENSO: 63,107 sets installed, 10.1% market shareNew Vision: 62,126 sets installed, 9.9% market shareCrystal-Optech: 51,831 sets installed, 8.3% market shareAUMOVIO: 45,455 sets installed, 7.3% market shareHuawei Technologies: 33,370 sets installed, 5.3% market shareFUTURUS: 30,595 sets installed, 4.9% market shareFinDreams Precision: 17,075 sets installed, 2.7% market sharePUCHUANG: 10,389 sets installed, 1.7% market shareFrom the January–February 2026 HUD supplier rankings, the market showed a clear structure of one dominant leader, strong Chinese presence, and well-defined tiers. Foryou Multimedia ranked first with 194,471 sets installed and a 31.1% share, firmly leading the mainstream market with its scale and cost advantages. In the second tier, E-LEAD, DENSO, and New Vision each held around 10% share, with similar volumes and close competition. Crystal-Optech and AUMOVIO followed in the mid-tier with shares of around 7%–8%. Meanwhile, suppliers such as Huawei Technologies and FUTURUS are accelerating their expansion in intelligent and AR-HUD products, further strengthening their market presence.Top AR-HUD suppliersE-LEAD: 54,451 sets installed, 26.3% market shareNew Vision: 36,057 sets installed, 17.4% market shareHuawei Technologies: 33,370 sets installed, 16.1% market shareForyou Multimedia: 25,920 sets installed, 12.5% market shareCrystal-Optech: 18,960 sets installed, 9.1% market shareFUTURUS: 16,676 sets installed, 8.0% market sharePUCHUANG: 6,334 sets installed, 3.1% market shareHirain Technologies: 5,558 sets installed, 2.7% market shareFinDreams Precision: 4,031 sets installed, 1.9% market shareLeapmotor: 2,940 sets installed, 1.4% market shareFrom the January–February 2026 AR-HUD supplier rankings, the market showed a multi-player competitive landscape with relatively fragmented concentration. E-LEAD ranked first with 54,451 sets installed and a 26.3% market share. New Vision and Huawei Technologies followed with shares of 17.4% and 16.1%, respectively, with relatively small gaps among leading players and intense competition. Foryou Multimedia and Crystal-Optech formed the second tier, holding shares between 9% and 12.5%. Other suppliers such as PUCHUANG, Hirain Technologies, FinDreams Precision, and Leapmotor also entered the top ten, mainly driven by project-based supply or in-house deployment. Overall, the AR-HUD market has yet to produce a clear dominant leader. As demand for immersive interaction and intelligent driving visualization continues to grow, the competitive landscape is expected to remain dynamic.Top suppliers of integrated center console displayDesay SV: 455,667 sets installed, 18.0% market shareForyou General Electronics: 223,834 sets installed, 8.8% market shareBYD: 191,271 sets installed, 7.6% market shareInnolux: 168,415 sets installed, 6.7% market shareHSAE: 163,275 sets installed, 6.4% market sharePanasonic: 119,679 sets installed, 4.7% market shareFULSCIENCE: 106,887 sets installed, 4.2% market shareHIWAY: 102,931 sets installed, 4.1% market shareTen Pao: 99,342 sets installed, 3.9% market shareBICV: 87,665 sets installed, 3.5% market shareFrom the January–February 2026 integrated center console display supplier rankings, the market showed a leading top player with overall fragmented competition. Desay SV ranked first with 455,667 sets installed and an 18.0% market share, maintaining a clear scale advantage but without absolute dominance. In the second tier, Foryou General Electronics, BYD, and Innolux held shares between 7% and 9%, with relatively close installation volumes and intense competition. HSAE and Panasonic formed the mid-tier, each maintaining a 5%–7% market share, while FULSCIENCE, HIWAY, and Ten Pao stayed around 4%. BICV entered the top ten with a 3.5% share, reflecting its continued expansion in the smart cockpit sector.Top suppliers of integrated LCD instrument clusterForyou General Electronics: 276,805 sets installed, 12.0% market shareAUMOVIO: 258,962 sets installed, 11.2% market shareDENSO: 219,236 sets installed, 9.5% market shareDesay SV: 190,697 sets installed, 8.3% market shareVisteon: 174,935 sets installed, 7.6% market shareTianyouwei: 151,198 sets installed, 6.5% market shareInnolux: 78,570 sets installed, 3.4% market shareXinTongda: 72,973 sets installed, 3.2% market shareNissei Display: 72,936 sets installed, 3.2% market shareBosch: 68,176 sets installed, 3.0% market shareFrom the January–February 2026 integrated LCD instrument cluster supplier rankings, the market showed a close top tier and overall fragmented competition. Foryou General Electronics led with 276,805 sets installed and a 12.0% market share, followed closely by AUMOVIO and DENSO, both exceeding 200,000 units, indicating intense competition among the leading players. Desay SV and Visteon formed the second tier with market shares of 7%–8%, while Tianyouwei ranked sixth with 6.5%, maintaining a stable position. In the lower tier, Innolux, XinTongda, Nissei Display, and Bosch each held less than 4%, reflecting a moderately concentrated market structure.Top smart speech solution suppliersiFLYTEK: 999,904 units installed, 43.9% market shareAISpeech: 443,694 units installed, 19.5% market shareCerence: 330,776 units installed, 14.5% market shareDreamSmart: 168,438 units installed, 7.4% market shareBaidu: 137,521 units installed, 6.0% market shareXiaomi EV: 59,341 units installed, 2.6% market shareTesla: 57,882 units installed, 2.5% market shareVW-Mobvoi: 20,475 units installed, 0.9% market shareAlibaba: 17,769 units installed, 0.8% market shareXPENG: 17,229 units installed, 0.8% market shareFrom the January–February 2026 smart speech solution supplier rankings, the market showed high concentration with a clear leading tier. iFLYTEK led with 999,904 units installed and a 43.9% market share, maintaining a significant advantage driven by strong capabilities in in-vehicle speech algorithms, customer coverage, and large-scale deployment. AISpeech and Cerence ranked second and third with shares of 19.5% and 14.5%, forming the core competitive group in the speech market. DreamSmart and Baidu held relatively stable positions in the 6%–7% range, while Xiaomi EV expanded its speech system deployment through in-house vehicle models. In the tail segment, Tesla, VW-Mobvoi, Alibaba, and XPENG each held less than 2%, primarily supporting self-developed solutions or project-based integration.