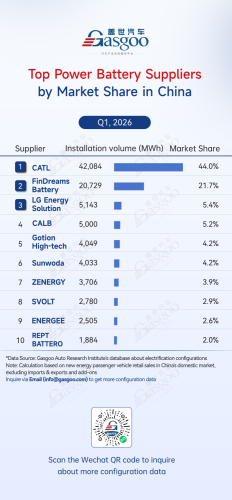

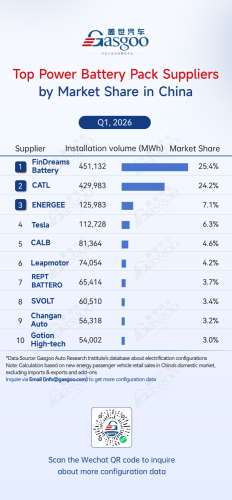

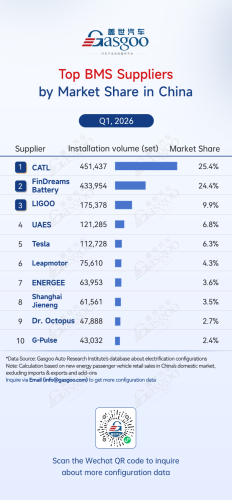

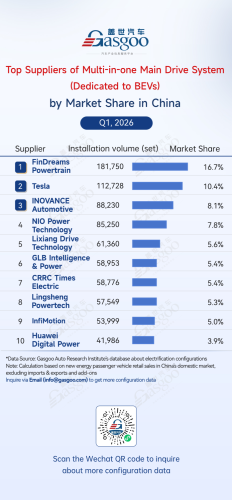

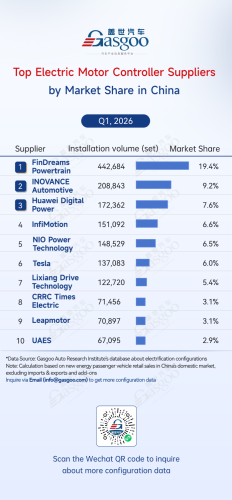

According to data compiled by the Gasgoo Automotive Research Institute, in Q1 2026, China's new energy vehicle (NEV) electrification core segments exhibited a pattern of entrenched leadership, intensifying tier-based competition, and deepening vertical integration.Across six key areas—including power batteries, BMS, and drive motors—installation data shows that leading enterprises continue to concentrate resources through technological and scale advantages. Meanwhile, OEM in-house development and the supply chain ecosystem are diverging in parallel, with China's local suppliers maintaining a firmly dominant position.Second-tier and specialized niche players are achieving differentiated breakthroughs, further driving the industry toward greater self-reliance, higher integration efficiency, and continuous technological iteration. These dynamics provide an important basis for assessing the competitive landscape and structural evolution of the automotive components industry.Top power battery suppliersCATL: 42,084 MWh installed capacity, 44.0% market shareFinDreams Battery: 20,729 MWh installed capacity, 21.7% market shareLG Energy Solution: 5,143 MWh installed capacity, 5.4% market shareCALB: 5,000 MWh installed capacity, 5.2% market shareGotion High-tech: 4,049 MWh installed capacity, 4.2% market shareSunwoda: 4,033 MWh installed capacity, 4.2% market shareZENERGY: 3,706 MWh installed capacity, 3.9% market shareSVOLT: 2,780 MWh installed capacity, 2.9% market shareENERGEE: 2,505 MWh installed capacity, 2.6% market shareREPT BATTERO: 1,884 MWh installed capacity, 2.0% market shareIn Q1 2026, China's NEV power battery market maintained a competitive landscape characterized by "one dominant leader and multiple strong players," with leading companies further strengthening their advantages. CATL ranked first with a 44.0% market share and 42,084 MWh of installed capacity, continuing to consolidate its leadership through its full industry-chain presence, rapid technology iteration, and large-scale production capacity.FinDreams Battery ranked second with a 21.7% share and 20,729 MWh of installed capacity, sustaining steady growth through its deep integration with BYD and strong vertical integration capabilities, supported by stable in-house demand.LG Energy Solution ranked third with a 5.4% market share, making it the only foreign supplier among the top ten. CALB, Gotion High-tech, Sunwoda, and ZENERGY ranked fourth to seventh, with market shares ranging from 3.9% to 5.2%, reflecting particularly intense competition within the mid-tier group. Meanwhile, SVOLT, ENERGEE, and REPT BATTERO ranked eighth to tenth, each holding less than 3% market share, showing a relatively significant gap compared with the leading players.Top power battery pack suppliersFinDreams Battery: 451,132 sets installed, 25.4% market shareCATL: 429,983 sets installed, 24.2% market shareENERGEE: 125,983 sets installed, 7.1% market shareTesla: 112,728 sets installed, 6.3% market shareCALB: 81,364 sets installed, 4.6% market shareLeapmotor: 74,054 sets installed, 4.2% market shareREPT BATTERO: 65,414 sets installed, 3.7% market shareSVOLT: 60,510 sets installed, 3.4% market shareChangan Auto: 56,318 sets installed, 3.2% market shareGotion High-tech: 54,002 sets installed, 3.0% market shareIn Q1 2026, the battery pack market showed a clear two-leader structure with well-defined competitive tiers, as the top two suppliers together accounted for nearly 50% of the market. FinDreams Battery overtook CATL to rank first with 451,132 sets installed (25.4% share). Backed by BYD's vertically integrated vehicle manufacturing system, its pack products maintain strong compatibility with vehicle platforms, while robust in-house demand continued to drive installation growth.CATL ranked second with a 24.2% market share and 429,983 sets installed, continuing to expand its external customer base through standardized pack solutions, multi-model adaptability, and broad OEM partnerships.ENERGEE, Tesla, and CALB formed the industry's second tier. Among them, ENERGEE stood out in specialized supply segments with a 7.1% market share. Notably, self-developed supplier systems from automakers such as FinDreams Battery, ENERGEE, Tesla, Leapmotor, SVOLT, and Changan Automobile appeared frequently in the rankings, reflecting the growing trend of OEMs strengthening in-house pack production to better control core component costs and technologies.Top BMS suppliersCATL: 451,437 sets installed, 25.4% market shareFinDreams Battery: 433,954 sets installed, 24.4% market shareLIGOO: 175,378 sets installed, 9.9% market shareUAES: 121,285 sets installed, 6.8% market shareTesla: 112,728 sets installed, 6.3% market shareLeapmotor: 75,610 sets installed, 4.3% market shareENERGEE: 63,953 sets installed, 3.6% market shareShanghai Jieneng: 61,561 sets installed, 3.5% market shareDr. Octopus: 47,888 sets installed, 2.7% market shareG-Pulse: 43,032 sets installed, 2.4% market shareIn Q1 2026, China's BMS market showed a structure dominated by two leading players, alongside an acceleration in OEM self-developed solutions. FinDreams Battery led the market with 451,437 sets installed (25.2% share), leveraging BYD's vertically integrated R&D and manufacturing system. Its BMS solutions are tightly aligned with in-house vehicle platforms, providing strong compatibility and stability, which further reinforces its market position.CATL followed closely with a 24.2% share, supported by long-standing expertise in battery management systems and a broad customer base across major automakers, maintaining a solid and stable core market footprint.LIGOO, UAES, Tesla, and Leapmotor ranked third to sixth with market shares of 10.4%, 6.8%, 6.3%, and 4.2%, respectively. Notably, OEMs such as Tesla and Leapmotor continue to pursue in-house BMS development, steadily increasing the share of internal supply. In addition, automaker-affiliated suppliers including ENERGEE and Shanghai Jieneng also entered the top ten, further highlighting the accelerating trend of major OEMs integrating BMS into their core self-developed systems. Dr. Octopus ranked tenth with a 2.4% share, maintaining stable supply capability in niche segments.Top electric drive motor suppliersFinDreams Powertrain: 442,633 sets installed, 19.4% market shareInfiMotion: 197,670 sets installed, 8.7% market shareHuawei Digital Power: 167,248 sets installed, 7.3% market shareINOVANCE Automotive: 159,690 sets installed, 7.0% market shareNIO Power Technology: 148,529 sets installed, 6.5% market shareTesla: 137,083 sets installed, 6.0% market shareHYCET: 76,898 sets installed, 3.4% market shareLingsheng Powertech: 69,435 sets installed, 3.0% market shareCRRC Times Electric: 64,719 sets installed, 2.8% market shareLixiang Drive Technology: 61,360 sets installed, 2.7% market shareIn Q1 2026, the drive motor market showed a clear trend of OEM-driven in-house systems with increasingly differentiated competitive tiers. Leveraging BYD's full vehicle ecosystem, FinDreams Powertrain built strong advantages in cost control, vehicle integration, and mass-production capability, reinforcing its leading position and forming a durable competitive barrier that remains difficult to challenge.InfiMotion ranked second with 197,670 units installed and an 8.7% market share, supported by stable backing from the Chery Group, securing its position within the leading tier.Huawei Digital Power, INOVANCE Automotive, NIO Power Technology, and Tesla ranked third to sixth with market shares of 7.3%, 7.0%, 6.5%, and 6.0%, respectively, reflecting a highly competitive and closely clustered middle tier.In addition, HYCET, Lingsheng Powertech, CRRC Times Electric, and Lixiang Drive Technology also entered the top ten, forming a differentiated competitive landscape alongside leading players and jointly driving technological upgrades and improvements in system-level integration capabilities across the drive motor industry.Top suppliers of power semiconductor device (dedicated to e-drive)FinDreams Powertrain: 181,750 sets installed, 16.7% market shareTesla: 112,728 sets installed, 10.4% market shareINOVANCE Automotive: 88,230 sets installed, 8.1% market shareNIO Power Technology: 85,250 sets installed, 7.8% market shareLixiang Drive Technology: 61,360 sets installed, 5.6% market shareGLB Intelligence & Power: 58,953 sets installed, 5.4% market shareCRRC Times Electric: 58,776 sets installed, 5.4% market shareLingsheng Powertech: 57,549 sets installed, 5.3% market shareInfiMotion: 53,999 sets installed, 5.0% market shareHuawei Digital Power: 41,986 sets installed, 3.9% market shareIn Q1 2026, the power semiconductor device (dedicated to e-drive) market showed a relatively fragmented structure, with small gaps between competitive tiers and intense industry competition. FinDreams Powertrain ranked first with a 16.7% market share and 181,750 sets installed. Leveraging BYD's vertically integrated e-drive ecosystem, its multi-in-one drive solutions maintain strong advantages in system integration, cost efficiency, and large-scale deployment, continuously supporting the company's in-house vehicle demand.Tesla followed in second place with 112,728 sets installed and a 10.4% market share, while INOVANCE Automotive ranked third with 88,230 sets and an 8.1% share. The top three players together accounted for over 35% of the market, leading the industry landscape.NIO Power Technology, Lixiang Drive Technology, and GLB Intelligence & Power ranked fourth to sixth with market shares ranging from 5.4% to 7.8%, forming the second tier. CRRC Times Electric, Lingsheng Powertech, InfiMotion, and Huawei Digital Power followed closely, with shares concentrated between 3.9% and 5.4%, indicating intense competition and minimal gaps among players.Top electric motor controller suppliersFinDreams Powertrain: 442,684 sets installed, 19.4% market shareINOVANCE Automotive: 208,843 sets installed, 9.2% market shareHuawei Digital Power: 172,362 sets installed, 7.6% market shareInfiMotion: 151,092 sets installed, 6.6% market shareNIO Power Technology: 148,529 sets installed, 6.5% market share]Tesla: 137,083 sets installed, 6.0% market shareLixiang Drive Technology: 122,720 sets installed, 5.4% market shareCRRC Times Electric: 71,456 sets installed, 3.1% market shareLeapmotor: 70,897 sets installed, 3.1% market shareUAES: 67,095 sets installed, 2.9% market shareIn Q1 2026, the motor controller market exhibited a diversified competitive landscape. FinDreams Powertrain ranked first with a 19.4% market share and 442,684 units installed, continuing to leverage its deep integration with BYD's vehicle platforms. Supported by full vertical integration across the supply chain, it maintains strong competitiveness in large-scale deployment and cost control, further reinforcing its leadership position in OEM in-house electric control systems.INOVANCE Automotive and Huawei Digital Power ranked second and third with market shares of 9.2% and 7.6%, respectively. Leveraging strong expertise in motor control technologies, power semiconductors, and system integration, both companies maintain broad compatibility across multiple OEM platforms, supporting a relatively stable competitive position in the market ranking.Notably, the top ten list includes multiple OEM in-house suppliers such as FinDreams Powertrain, InfiMotion, and NIO Power Technology. Together, these automaker-affiliated players account for over half of the total market, underscoring the accelerating trend of OEMs strengthening self-developed capabilities in core e-drive components and reinforcing their technological autonomy.