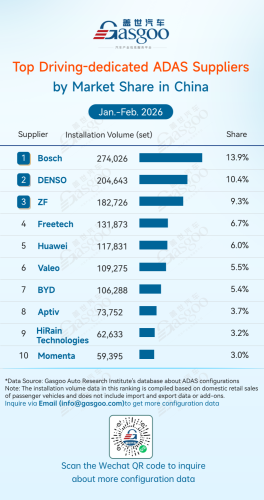

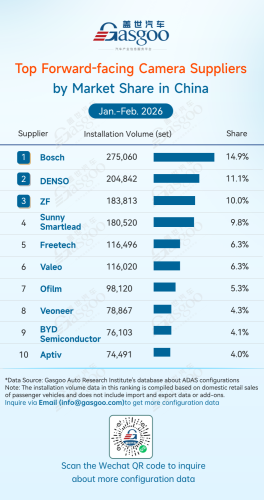

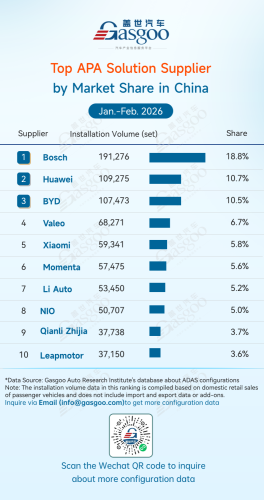

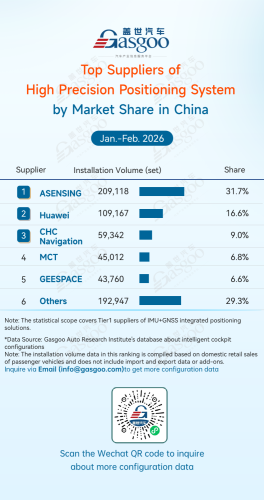

According to the Gasgoo Automotive Research Institute, China's core passenger vehicle component market remained stable from January to February 2026, with differentiated competitive dynamics across segments. In air suspension, LiDAR, HD maps, and high-precision positioning, China's local players have established clear leadership, with top suppliers dominating through dvantages in technology, capacity, and cost. In contrast, driving-dedicated ADAS, and APA solution are still led by international players, while domestic suppliers are accelerating their expansion and steadily gaining market share, showing strong growth potential.This landscape reflects China's automotive industry moving deeper into the integration of electrification and intelligence, with the core component supply chain accelerating toward greater self-reliance. The rise of Chinese suppliers alongside global players is driving technology upgrades and strengthening the foundation for advanced intelligent vehicles, while also offering clear insights into industry competition and future trends.Top air suspension system suppliersTuopu Group: 75,362 sets installed, 34.1% market shareKH Automotive Technologies: 71,017 sets installed, 32.1% market shareBaolong Automotive: 58,779 sets installed, 26.6% market shareVibracoustic: 7,124 sets installed, 3.2% market shareAUMOVIO: 5,680 sets installed, 2.6% market shareOthers: 3,005 sets installed, 1.4% market shareFrom January to February 2026, China's air suspension system market continued to see the strong rise of domestic players and a highly concentrated competitive landscape. Tuopu Group ranked first with 75,362 units installed and a 34.1% market share, further consolidating its leading position through large-scale supply capabilities and integrated solutions. KH Automotive Technologies and Baolong Automotive followed with 71,017 units and 58,779 units, holding 32.1% and 26.6% market share, respectively. Together, the top three accounted for over 92% of the market, forming a clear and stable tiered structure that dominates the domestic air suspension supply chain.Top LiDAR suppliersHuawei Technologies: 225,337 units installed, 37.1% market shareHesai Technology: 199,934 units installed, 32.9% market shareSeyond: 99,584 units installed, 16.4% market shareRoboSense: 64,674 units installed, 10.6% market shareOthers: 18,565 units installed, 3.1% market shareFrom January to February 2026, China's LiDAR market saw strong growth, with a highly concentrated structure led by domestic players. Huawei Technologies ranked first with a 37.1% market share (225,337 units installed), benefiting from strengths in perception accuracy, cost control, and automotive-grade reliability, making it a key choice for advanced ADAS solutions among multiple OEMs. Hesai Technology followed with a 32.9% share, bringing the combined share of the top two China's local players to 70%, firmly dominating the market. Seyond and RoboSense ranked third and fourth with 16.4% and 10.6% shares, respectively, together forming the core supplier matrix of China's LiDAR market.Top driving-dedicated ADAS suppliersBosch: 274,026 sets installed, 13.9% market shareDENSO: 204,643 sets installed, 10.4% market shareZF: 182,726 sets installed, 9.3% market shareFreetech: 131,873 sets installed, 6.7% market shareValeo: 117,831 sets installed, 6.0% market shareHuawei: 109,275 sets installed, 5.5% market shareBYD: 106,288 sets installed, 5.4% market shareAptiv: 73,752 sets installed, 3.7% market shareHirain Technologies: 62,633 sets installed, 3.2% market shareMomenta: 59,395 sets installed, 3.0% market shareFrom January to February 2026, China's driving-dedicated ADAS market continued to be led by global players, while domestic suppliers steadily increased their share. Bosch ranked first with 274,026 sets installed (13.9% share), with its mature and reliable solutions remaining a key choice for many OEMs. DENSO and ZF followed with 10.4% and 9.3%, respectively, forming the leading tier alongside Bosch. China's local players such as Freetech, Huawei, and BYD also ranked among the top. Freetech placed fourth with a 6.7% share, while Huawei and BYD ranked sixth and seventh with 5.5% and 5.4%, respectively. Hirain Technologies and Momenta also entered the top ten with 3.2% and 3.0%, highlighting the strong advantages of local suppliers in algorithm iteration, vertical integration, and market responsiveness.Top forward-facing camera suppliersBosch: 275,060 sets installed, 14.9% market shareDENSO: 204,842 sets installed, 11.1% market shareZF: 183,813 sets installed, 10.0% market shareSunny Smartlead: 180,520 sets installed, 9.8% market shareFreetech: 116,496 sets installed, 6.3% market shareValeo: 116,020 sets installed, 6.3% market shareOfilm: 98,120 sets installed, 5.3% market shareVeoneer: 78,867 sets installed, 4.3% market shareBYD Semiconductor: 76,103 sets installed, 4.1% market shareAptiv: 74,491 sets installed, 4.0% market shareFrom January to February 2026, China's forward-facing camera market continued to be led by global players, while Chinese suppliers steadily gained share. Bosch ranked first with 275,060 sets installed (14.9% share), remaining the industry benchmark thanks to its strong technical foundation and global supply capabilities. DENSO and ZF followed with 11.1% and 10.0%, respectively, forming the leading tier alongside Bosch, with a combined market share of 36.0%. Sunny Smartlead ranked fourth with a 9.8% share, emerging as a leading local player and demonstrating strengths in optical sensing technology and production capacity. Other Chinese suppliers, including Freetech, Ofilm, and BYD Semiconductor, also secured key positions, ranking among the top ten with shares of 6.3%, 5.3%, and 4.1%, respectively.Top APA solution suppliersBosch: 191,276 sets installed, 18.8% market shareHuawei: 109,275 sets installed, 10.7% market shareBYD: 107,473 sets installed, 10.5% market shareValeo: 68,271 sets installed, 6.7% market shareXiaomi: 59,341 sets installed, 5.8% market shareMomenta: 57,475 sets installed, 5.6% market shareLi Auto: 53,450 sets installed, 5.2% market shareNIO: 50,707 sets installed, 5.0% market shareQianli Zhijia: 37,738 sets installed, 3.7% market shareLeapmotor: 37,150 sets installed, 3.6% market shareFrom January to February 2026, China's APA market was led by global players, while domestic suppliers continued to gain share. Bosch ranked first with 191,276 sets and an 18.8% share, followed by Huawei and BYD with 10.7% and 10.5%. China's local players such as Xiaomi, Momenta, Li Auto, and NIO also ranked among the top, competing through strengths in algorithms and user experience. Overall, competition is shifting from basic functionality to scenario coverage and performance, with local players accelerating their rise.Top HD map suppliersAutoNavi: 149,509 sets installed, 43.8% market shareTencent: 50,707 sets installed, 14.9% market shareLangge Technology: 50,284 sets installed, 14.7% market shareNavInfo: 30,759 sets installed, 9.0% market shareOthers: 60,116 sets installed, 17.6% market shareFrom January to February 2026, China's HD map market continued to be led by AutoNavi, with domestic players dominating the landscape. AutoNavi ranked first with a 43.8% market share and 149,509 sets installed, benefiting from strengths in data accuracy, update frequency, and automotive-grade integration, making it a key partner for advanced ADAS solutions. Tencent, Langge Technology, and NavInfo followed with shares of 14.9%, 14.7%, and 9.0%, respectively, forming a competitive second tier. Other suppliers accounted for a combined 17.6%, indicating the presence of a long-tail market.Top suppliers of high precision positioning systemASENSING: 209,118 sets installed, 31.7% market shareHuawei: 109,167 sets installed, 16.6% market shareCHC Navigation: 59,342 sets installed, 9.0% market shareMCT: 45,012 sets installed, 6.8% market shareGEESPACE: 43,760 sets installed, 6.6% market shareOthers: 192,947 sets installed, 29.3% market shareFrom January to February 2026, China's high precision positioning market saw accelerating adoption of fusion-based positioning solutions, with Chinese players dominating the competitive landscape. ASENSING ranked first with a 31.7% market share and 209,118 sets installed, demonstrating strong scale advantages and deep customer penetration in automotive-grade positioning. Huawei, CHC Navigation, MCT, and GEESPACE followed, each building differentiated positions across various application scenarios. Leveraging strengths in sensor fusion algorithms, multi-source perception integration, and automotive-grade reliability, these China's local suppliers have become key partners for advanced ADAS solutions among OEMs.