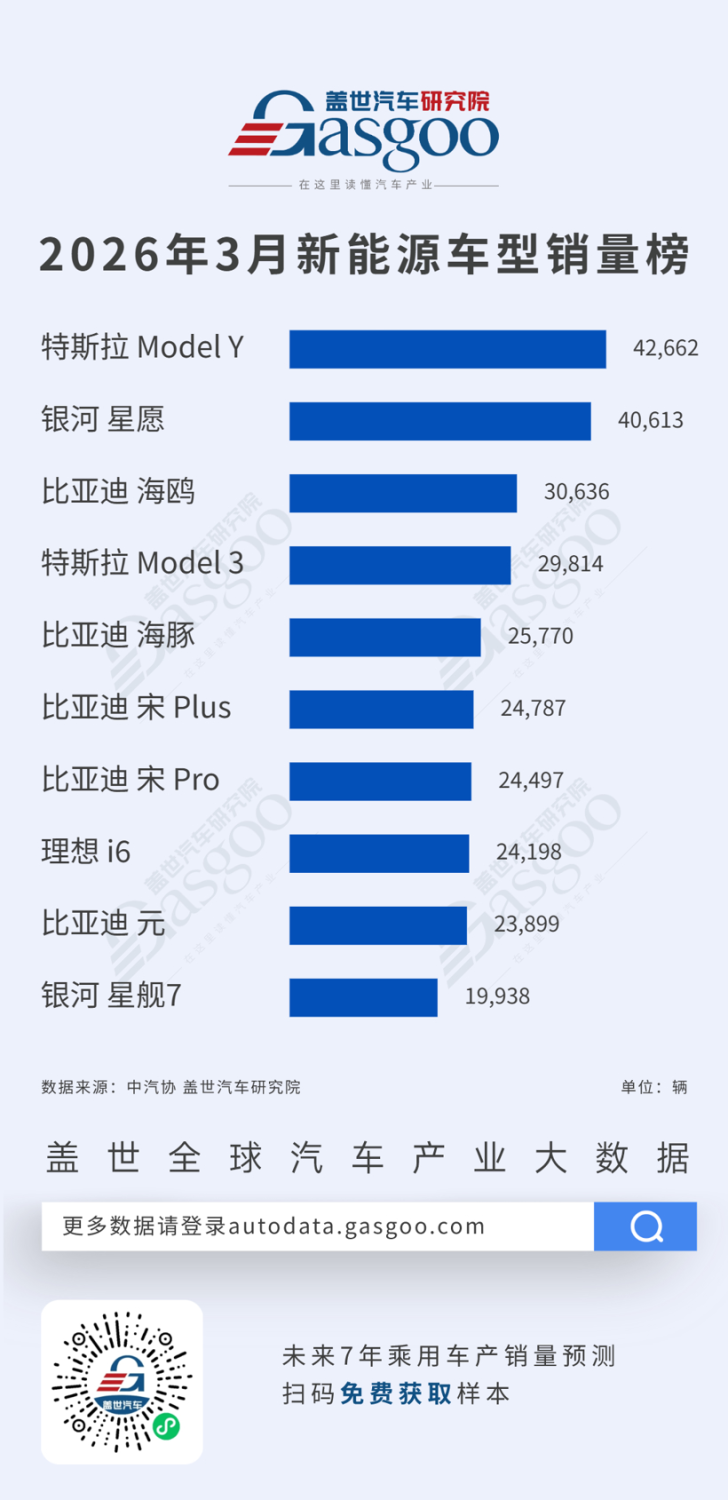

Gasgoo Munich-Data from Gasgoo Automotive Institute reveals a split market landscape in March 2026. Internal combustion engine (ICE) sales remain steady, with domestic brands holding sway and tight competition across models. In the new-energy sector, however, the market is top-heavy: Tesla’s Model Y and Geely’s Galaxy Star Wish both surged past 40,000 units, while BYD landed five models in the top ten to lead the brands. Together, these powertrains serve distinct consumer needs, forming the backbone of China’s passenger vehicle market.March 2026 ICE Passenger Vehicle Sales RankingFirst place, Nissan Sylphy, March sales 27,514 unitsSecond place, Changan Eado/Eado Plus, March sales 23,960 unitsThird place, Chery Tiggo 7/7 Plus, March sales 23,838 unitsFourth place, Geely Binyue/Binyue Pro, March sales 20,872 unitsFifth place, Geely Xingyue L, March sales 20,590 unitsSixth place, Chery Explore 06, March sales 20,553 unitsSeventh place, Changan CS75 Plus, March sales 19,945 unitsEighth place, Volkswagen Lavida, March sales 19,528 unitsNinth place, Volkswagen Tayron, March sales 19,342 unitsTenth place, Chery Tiggo 8/8 Plus/Pro, March sales 18,609 unitsThe top ten ICE models showed resilience in March 2026. Nissan’s Sylphy took the crown with 27,514 units, followed closely by the Changan Eado series at 23,960 and the Chery Tiggo 7 lineup at 23,838. Geely’s Binyue and Xingyue L, along with Chery’s Explore 06, all breached the 20,000-unit mark to round out the middle of the pack. The field is remarkably tight: the gap between first and tenth place is under 9,000 units, while positions two through seven are squeezed into a narrow 20,000 to 24,000-unit band.Domestics dominate the brand landscape, claiming seven of the top ten spots. Chery stands out with three entries—the Tiggo 7 series, Explore 06, and Tiggo 8 series—combining for roughly 63,000 sales. Changan held its ground with the Eado series and CS75 Plus, while Geely’s Binyue and Xingyue L cemented their market appeal. Joint ventures are losing ground; only Volkswagen managed two entries. SUVs remain the absolute majority here, accounting for seven of the top ten, with sedans represented solely by the Sylphy, Eado, and Lavida.Even as new-energy vehicles encroach on market share, the ICE sector retains significant scale and steady demand. Domestic brands are expanding their slice of the SUV and sedan segments through upgraded products and aggressive pricing, while joint ventures lean on established platforms and legacy reputations to defend their turf. Looking ahead, as hybrid technology blends further with traditional powertrains, the battle for the ICE market will hinge on overall value and user experience.March 2026 New-Energy Passenger Vehicle Sales RankingFirst place, Tesla Model Y, March sales 42,662 unitsSecond place, Galaxy Star Wish, March sales 40,613 unitsThird place, BYD Seagull, March sales 30,636 unitsFourth place, Tesla Model 3, March sales 29,814 unitsFifth place, BYD Dolphin, March sales 25,770 unitsSixth place, BYD Song Plus, March sales 24,787 unitsSeventh place, BYD Song Pro, March sales 24,497 unitsEighth place, Li Auto i6, March sales 24,198 unitsNinth place, BYD Yuan, March sales 23,899 unitsTenth place, Galaxy Starship 7, March sales 19,938 unitsTesla’s Model Y led the NEV chart in March with 42,662 deliveries, while Geely’s Galaxy Star Wish followed at 40,613—the only two models to top 40,000 units. The BYD Seagull (30,636) and Tesla Model 3 (29,814) took the next two spots. Positions five through nine were locked in a fierce battle between 23,000 and 26,000 units. Overall, a clear hierarchy is emerging among the top sellers, even as the market fragments across different segments.BYD remains the dominant force by volume, placing five models in the top ten—the Seagull, Dolphin, Song Plus, Song Pro, and Yuan—which collectively moved roughly 129,600 units. Tesla followed with two models totaling about 72,500. Geely’s Galaxy sub-brand is making rapid strides, with the Star Wish and Starship 7 combining for over 60,000 sales.The NEV sector is shifting its focus from relying on a single blockbuster to leveraging multi-product synergies. Domestic players like Geely Galaxy and BYD are expanding their reach across niches with broad portfolios. Tesla continues to draw strength from its Model Y and Model 3, while brands like Li Auto hold ground through differentiated positioning. As penetration rates climb, the deciding factors for sales success will increasingly be comprehensive product competitiveness and brand ecosystem strength.

![BYD confirms new flagship EV has a range of 1,008 km [Video]](https://cdn.topcarnews.net/thumb/id/aHR0cHM6Ly9pMC53cC5jb20vZWxlY3Ry-ZWsuY28vd3AtY29udGVudC91cGxvYWRz-L3NpdGVzLzMvMjAyNi8wNy9CWUQtR3Jl-YXQtSGFuLUZsYWdzaGlwLUVWLmpwZWc_-dz0xNTAwJmFtcDtxdWFsaXR5PTgyJmFt-cDtzdHJpcD1hbGwmYW1wO3NzbD0x/c37374468f3a539ee1e0ce2b627e08d0.jpeg?t=20260727&post_id=48318)