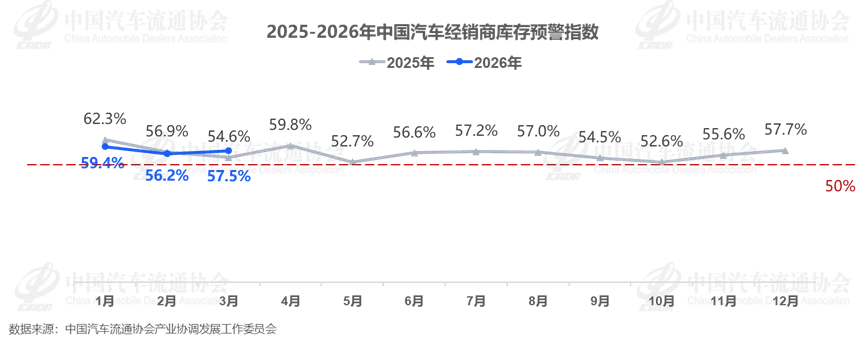

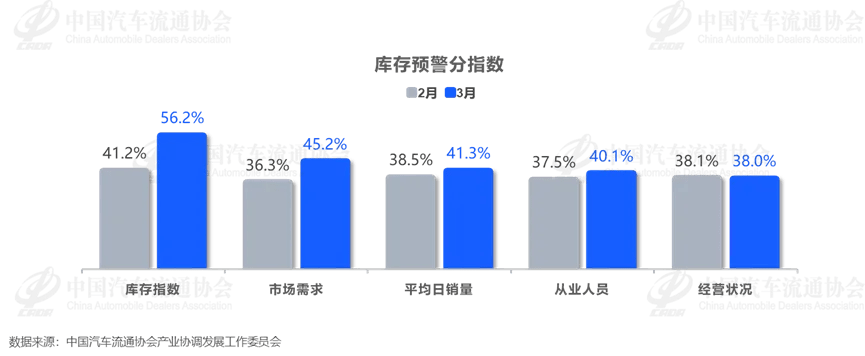

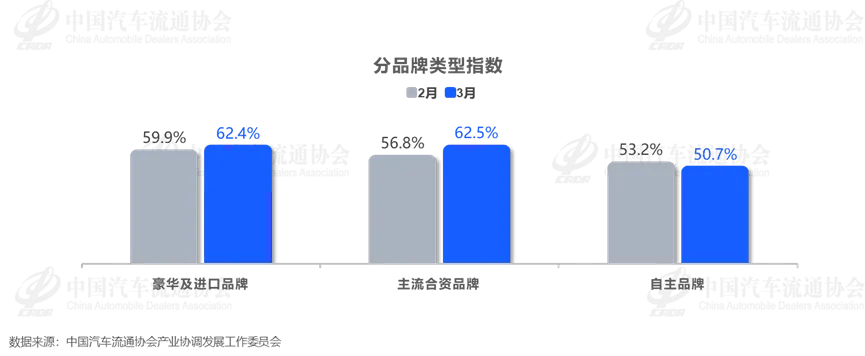

The latest data from the China Automobile Dealers Association (CADA) show that China’s Vehicle Inventory Alert Index (VIA) stood at 57.5% in March 2026, up 2.9 percentage points year-on-year and 1.3 percentage points month-on-month, remaining above the boom-bust threshold. From a timing perspective, the weak start to the year laid the groundwork for March’s rebound. In January and February, terminal demand was subdued due to policy transitions and cautious consumer sentiment. China VIA index trends from 2025 to 2026 Entering March, the rollout of consumption vouchers in multiple regions, a wave of new model launches, and the release of post-holiday demand drove a phase of market recovery. Industry estimates place passenger vehicle retail sales at around 1.8 million units for the month. However, inventory pressure at dealerships has become increasingly evident. Survey data show that 35.7% of dealers face moderate inventory pressure, 23.6% face relatively high pressure, and 14.3% are experiencing severe overstock, while only 12.1% remain within a reasonable range. China VIA index trends between February and March 2026 At the core of the issue is the persistent mismatch between supply and demand. On one hand, automakers stepped up wholesale deliveries after the Chinese New Year, forcing dealers to replenish inventory, pushing up the inventory sub-index. On the other hand, although showroom traffic has recovered, it remains insufficient to meet sales targets, resulting in limited conversion efficiency. Price system distortions continue to intensify. Price inversion—where transaction prices fall below invoice levels—has become widespread, with dealers relying on discounts to clear inventory, directly compressing profit margins. The operating conditions sub-index remained broadly stable, but underlying profitability continues to deteriorate, particularly among mainstream joint-venture and luxury brands. Regional divergence persists. In March, the northern region index reached 60.1%, significantly higher than the overall index of 57.5%, as well as the southern region at 50.2%, the eastern region at 58.3%, and the western region at 57.2%. China’s VIA index across different brand levels between February and March 2026 At the brand level, inventory pressure increased month-on-month for luxury & imported and mainstream joint-venture brands, with VIA all rising to above 62%. Meanwhile, the VIA index for domestic brands declined to 50.7%, indicating divergence in channel pressure across different segments. Looking ahead to April, although auto shows, subsidies, and new product launches will continue, seasonal factors are beginning to emerge, and dealers remain generally cautious about the second-quarter outlook. Survey results show that only 35% of dealers are optimistic about the second quarter, 44.3% hold a neutral view, and 20.7% explicitly express a lack of confidence. CADA noted that as supportive policies continue to take effect, the auto market is expected to see marginal improvement and a gradual recovery in the second quarter.