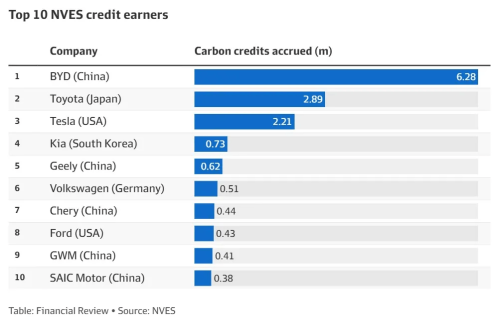

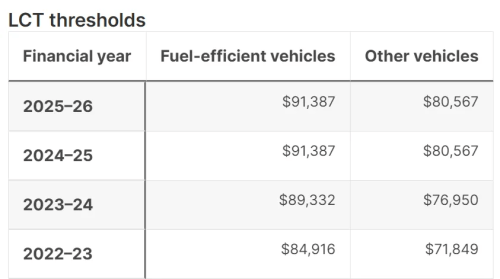

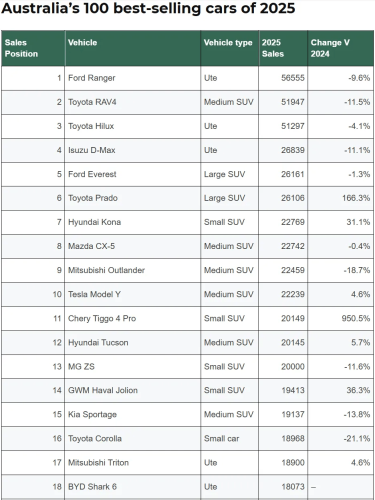

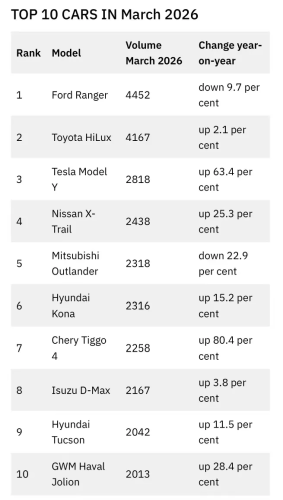

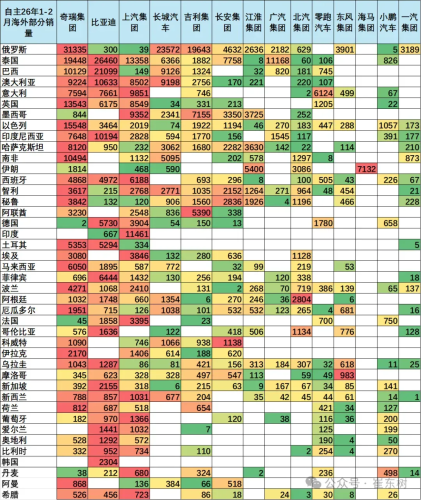

Many local Chinese and Chinese-Australian consumers have complained on social media that BYD sales staff have changed their approach—from previously urging quick orders with “immediate delivery” promises, to being less responsive, or even advising customers to think carefully before placing an order. As recently as February, debate had centered on whether BYD’s accumulation of 6.28 million net emission credits—generated from importing 39,603 new-energy vehicles in the second half of 2025 under Australia’s NVES regulatory framework—reflected inventory buildup or genuine demand. Top 10 NVES credit earners from Australia’s NVES The latest global energy crisis has driven up fuel costs, triggering a surge in overseas demand for new-energy vehicles and pushing Chinese EV brands into the spotlight—particularly those entering Australia in large numbers. From Great Wall Motor’s early entry in 2009 to the wave of Chinese NEV brands since 2019, Australia is now experiencing a rare period of supply tightness for Chinese automakers. On the surface, this appears to be an opportunity driven by global volatility. However, a broader view shows that even before the crisis, Chinese NEVs were already outperforming in Australia relative to other overseas markets, with higher strategic prioritization by automakers. Favored by brands such as BYD, Geely, Chery, Great Wall Motor and Xpeng, China’s share of Australia’s auto market has surged from 1.7% in 2019 to around 17% in 2025. BYD Atto3 In February and March, China overtook Japan for two consecutive months as the largest source of vehicle imports. This dynamic resembles Australia’s ecological history: invasive species like rabbits and camels either perish under harsh conditions or dominate the landscape. The same binary outcome may apply to automakers entering the market. So how long can this surge last? Three key themes help explain: an unprotected market, a transition vacuum, and a closing window. An open market with minimal barriers To understand why Chinese automakers have clustered in Australia, one must grasp the significance of an “unprotected” market. For Australia’s auto trade, this goes beyond openness—it effectively removes barriers altogether. Since July 1, 2022, Australia has exempted EVs, plug-in hybrids (with a 5% tariff reinstated from April 1, 2025), and hydrogen vehicles priced below the luxury car tax threshold from import duties. The luxury car tax threshold is indexed to CPI, set at AUD 91,387 (approximately RMB 435,000 (63,700)) for the 2025–2026 fiscal year, with a 33% tax applied above that level. Luxury Car Tax (LCT) thresholds by financial year from 2022 to 2026 Following the China–Australia Free Trade Agreement signed in 2015, qualifying Chinese vehicles gradually saw tariffs reduced to zero by 2019. This near-total openness contrasts sharply with the EU and U.S., where high barriers limit Chinese EV entry. Even during the Biden administration, scrutiny toward Chinese NEVs remained stringent. Australia’s openness stems from a different reality: it has little domestic industry left to protect. Unlike the EU and U.S., where Chinese EVs could disrupt entrenched supply chains and employment tied to brands like Volkswagen, Mercedes-Benz, GM and Ford, Australia’s automotive manufacturing base has largely disappeared. Australia’s EVs In the 1980s, when Toyota, Ford and GM operated plants locally, tariffs were as high as 57.5%. Over time, however, companies found Australia’s geography and resource structure unsuitable for manufacturing. Factors such as relatively low annual demand (around 1 million units), geographic isolation, a strong currency driven by mining, high labor costs, limited habitable land, and fragmented supply chains all constrained development. After GM’s Holden closed its final plant in 2017, Australia ceased domestic vehicle production entirely, leaving imports to dominate and rendering protectionist policies unnecessary. The result is a market without natural barriers but with strong economic fundamentals—highly attractive to global automakers. Ford Ranger Super Duty For carmakers, Australia represents a “no predators” environment with a clean competitive slate—precisely what Chinese brands have been seeking. A pure competitive landscape Australia’s competitive environment is defined by two factors: a transition vacuum among incumbents in the NEV sector, and consumer preferences that prioritize product capability over brand origin. This combination is particularly advantageous for Chinese automakers, which have rapidly advanced in electrification technologies. Transition vacuum of EV giants Unlike in China, where competition is intensifying, Japanese, Korean and U.S. brands remain dominant in Australia. Toyota, Mazda, Mitsubishi, Isuzu, Hyundai and Ford consistently rank among the top-selling brands, driven largely by pickups and SUVs. Toyota led the market in 2025 with 239,800 units, far ahead of Ford at 94,339 units. However, weaknesses are emerging. Toyota’s bZ4X sold fewer than 1,000 units in 2025, while Mazda, Mitsubishi and Isuzu have minimal NEV offerings. Meanwhile, Chinese brands are aggressively expanding across both ICE and electrified segments. This shift has already impacted legacy players, with brands like Ford, Mitsubishi, Mazda and Isuzu recording varying degrees of sales decline in 2025. At the model level, most top-selling ICE vehicles also saw declines, except for fully refreshed models like the Toyota Prado and Hyundai Kona. For example, the Ford Ranger fell 9.6% to 56,555 units, and the Toyota RAV4 dropped 11.5% to 51,947 units. Australia’s 100 best-selling cars of 2025 Looking ahead, demand for rugged SUVs and pickups will remain strong given Australia’s geography, but policy pressures are mounting. Australia aims for NEVs to account for 30% of sales by 2030 and introduced the New Vehicle Efficiency Standard in July 2025, effectively a carbon credit system that increases compliance costs for ICE-heavy brands. This policy shift directly benefits NEVs. Tesla Model Y ranked tenth among Australia’s best-selling vehicles in 2025 with 4.6% growth, and in March recorded a 63.4% increase, ranking third for the month—the only EV in the top rankings. Australia’s top 10 car models in March 2026 In March, total vehicle sales fell 3.3% year-on-year to 105,100 units, while EV sales surged 88.9% to 15,839 units, raising penetration from 7.5% to 14.6%. Within this, although BYD had no single model in the top 10, it ranked third among brands with 7,217 units, behind Toyota and Kia. Great Wall Motor (5,680 units) and Chery (4,018 units) ranked sixth and tenth respectively. Australia’s top 10 car brands in March 2026 With legacy players in transition, ICE demand under regulatory pressure, and limited NEV offerings from incumbents, Australia presents a rare level playing field—an ideal window for Chinese brands. Environment and consumer behavior Beyond competition, Australia’s consumer environment also supports Chinese automakers’ expansion. The IMF forecasts Australia’s per capita GDP at around $65,000 in 2025 (approximately RMB 444,000), higher than traditional developed economies like the UK and Germany. However, entry-level prices for top-selling vehicles in Australia typically start around RMB 150,000 (22,000), lower than Germany’s RMB 200,000 (29,300) benchmark. Additionally, Australia’s top 100 best-selling models are dominated entirely by SUVs and pickups, unlike Germany’s more diverse mix. This reflects Australia’s geography: a vast landmass of 7.69 million square kilometers, with population concentrated along eastern and southern coasts and long intercity distances—Sydney to Melbourne is about 870 km, while Perth to Adelaide exceeds 2,600 km. Such conditions amplify requirements for range, reliability and operating cost, favoring durable, high-capacity vehicles like SUVs and pickups. Meanwhile, conditions for EV adoption are improving. Fast-charging networks along the east coast have become increasingly connected between 2024 and 2025, reducing station spacing to under 150 km. Over 70% of households are detached homes, with about 30% equipped with solar panels, lowering home charging costs. Model Y Australia’s population structure is also unique. As of June 30, 2024, Australia had around 27.2 million residents, including 8.6 million born overseas, accounting for 31.5% of the population. The Chinese diaspora alone reached nearly 1.4 million in the 2021 census. Concentrated in New South Wales, Victoria and Queensland—Australia’s largest auto markets—this demographic is more receptive to Chinese EVs, reducing marketing barriers for automakers. These factors allow Chinese brands, sharpened by intense domestic competition, to leverage strengths in smart technology and cost control, while adapting products and localization strategies effectively. Opportunity or peak? Globally, Australia is not among the largest auto markets. In 2025, it sold 1.241 million vehicles, up 0.3% year-on-year, comparable to markets like Mexico, South Korea and the UK. This pales in comparison to China’s 34.4 million units (including 8.324 million exports) and the U.S. at 16.72 million units. Toyota RAV4 However, Australia stands out for its structural transformation. In December 2025, NEV sales reached 35,058 units, narrowly surpassing ICE vehicles (34,559 units) for the first time. For the full year, EV sales rose 13.1% to 103,300 units, while PHEVs surged 130.9% to 53,500 units—far outpacing the overall market growth of 0.3%. NEV penetration climbed from 0.8% in 2020 to 13.1% in 2025, marking the inflection point for Chinese brands. Initially, Chinese EVs entered Australia through BEVs such as BYD’s Yuan Plus, but limited model availability and low brand awareness constrained early growth. BYD Atto 3 Evo electric SUV The turning point came in 2025, as demand for PHEVs surged globally, including Australia. Chinese brands responded quickly with models like BYD Shark 6 and Chery Tiggo series, filling gaps faster than Japanese, Korean and U.S. competitors. As a result, BYD models such as Shark 6, Sealion 06 and Sealion 07 quickly entered best-seller lists, with the brand’s sales rising 156.2%, moving from 16th to 8th place. Chery Tiggo 4 Pro also posted a 950.5% increase to 20,149 units, ranking 11th overall. Both models entered Australia’s top 20 best-selling vehicles in 2025, driven by China’s hallmark value-for-money advantage. For instance, the BYD Shark 6 was priced at AUD 57,900 (launch price for the first 4,000 units, later AUD 59,900), undercutting comparable Ford Ranger variants priced at AUD 71,300 and AUD 66,100. BYD Shark 6 Lower energy costs, 2,500 kg towing capacity, and vehicle-to-load functionality further enhanced its appeal. This shift is also reshaping perceptions. Media coverage of the BYD Shark 6 frequently highlights its advanced smart features and strong value proposition, even drawing interest from U.S. consumers. Chinese brands have also adapted their market strategy, focusing on a light-asset approach—prioritizing dealer networks and aftersales services rather than local manufacturing. In July 2025, BYD transitioned from a third-party importer model to direct operations, consolidating pricing, inventory and brand control. Great Wall Motor and Chery are pursuing similar channel integration. This indicates a broader strategy: not just selling vehicles, but building brand and distribution influence. After the surge Recent developments point to continued momentum. China surpassed Japan as Australia’s largest vehicle import source in February and March. According to industry data, brands such as Chery, BYD, Great Wall Motor and SAIC each recorded over 8,000 overseas sales in early 2026. Oveaseas sales of China’s automakers across different countries in Jan-Feb 2026 Australia’s lack of protectionism, absence of domestic automakers, and product-focused consumer base provide a testing ground—and a training arena for eventual expansion into markets like Europe. Success depends on how quickly automakers capture this window, adapt product portfolios, and refine channel strategies. However, long-term challenges remain: aftersales service, brand perception, and limited pricing power. The transition vacuum will not last indefinitely. Toyota and Hyundai are accelerating NEV rollouts, and competition from Japanese and Korean brands is likely to intensify. For Chinese automakers, the real test is not entering the window—but sustaining growth after it closes, evolving from cost advantage to brand loyalty. In a market without protection, long-term success will depend less on being “cheap” and more on being “worth it.” When delivery lead times shrink from three months to three weeks, the true verdict on Chinese EVs in Australia will begin to emerge.