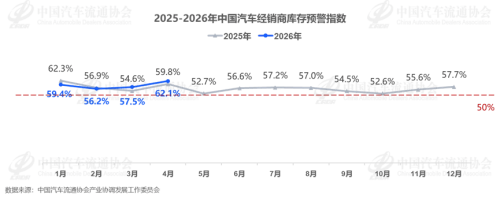

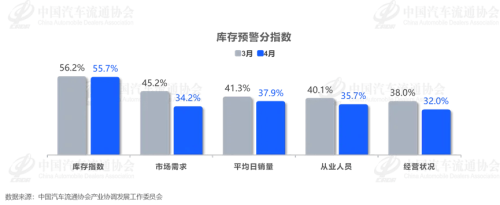

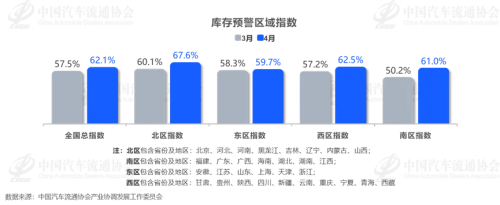

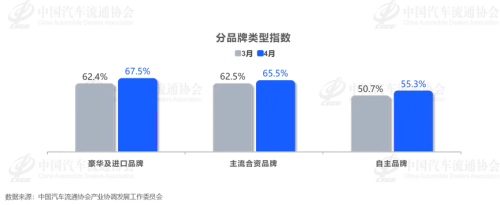

The latest “Vehicle Inventory Alert Index” released by the China Automobile Dealers Association shows that China’s auto dealer inventory warning index stood at 62.1% in April 2026, up 2.3 percentage points year‑on‑year and 4.6 percentage points from the previous month. 2025-2026 China Auto Dealer Inventory Warning Index The report points out that the auto market faced multiple pressures in April. On the one hand, the effective sales period in early April was shortened by the Qingming holiday and the spring break for primary and secondary schools; on the other hand, the concentrated sales push by dealers at the end of the first quarter pulled forward some car‑buying demand, leading to a marked slowdown in transaction pace in April. Although the auto show in late April provided early promotion and multiple new models were launched, actual showroom traffic did not show significant growth. The survey shows that over 60% of dealers saw their sales decline month‑on‑month in April, with only a few outlets achieving modest growth. Based on comprehensive forecasts, terminal retail sales of passenger vehicles in April are estimated at about 1.45 million units. Li Auto Store At the same time, the report also highlights the operational difficulties currently faced by domestic dealers, including: Inventory pressure. Dealers are assigned excessive vehicle pickup targets, inventory levels remain relatively high, and the share of long‑aging models is rising, further intensifying capital occupation and turnover strain. Continued price inversion at the terminal level, squeezing new‑vehicle gross profit margins. Increasing difficulty in customer acquisition. Showroom traffic and valid leads are declining, customers are in a strong wait‑and‑see mode, and transaction cycles are lengthening. To speed up inventory reduction, many dealers have adopted various countermeasures, including offline financial schemes, limited‑time promotions, and value‑added giveaways, as well as online live streaming and short‑video traffic generation. Inventory Warning Index Looking at the sub‑indices of the inventory warning index, affected by weak market demand and sluggish end‑user spending power, the inventory sub‑index fell slightly month‑on‑month in April. However, sub‑indices for market demand, average daily sales, employee conditions, and business performance all declined simultaneously, suggesting a broad deterioration in market sentiment. Inventory Warning Index by Region In terms of regional indices, the national composite index stood at 62.1%. Among regions, the northern region faced the greatest pressure with an index of 67.6%, while the western and southern regions both recorded indices above 60%. Index by Brand Type By brand type, the April indices for luxury & imported, mainstream joint‑venture, and domestic independent brands all rose month‑on‑month, indicating rising inventory pressure across all segments. Among them, pressure on luxury & imported brands was relatively higher, with their index jumping 5.1 percentage points from March. The report notes that dealers are generally cautious in their outlook for the May market. Intent orders accumulated during the Beijing Auto Show at the end of April are expected to be converted in May‑June, but the concentrated launch of new models may also divert customer traffic and lead to choice overload. The China Automobile Dealers Association forecasts that a significant rebound in the auto market in May is unlikely. This survey shows that nearly 80% of dealerships expect second‑quarter sales to decline year‑on‑year, with 41.4% projecting a drop of more than 10%. Only 22.7% expect sales to grow.