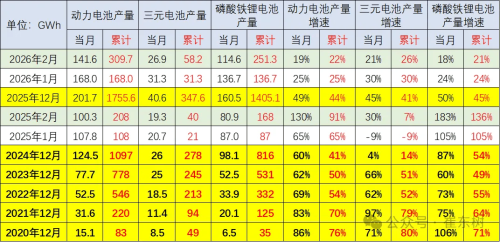

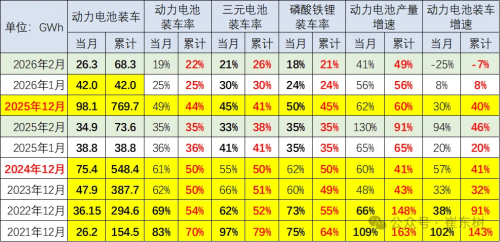

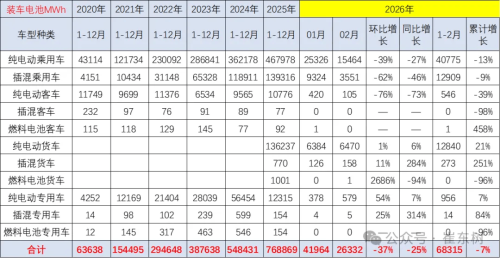

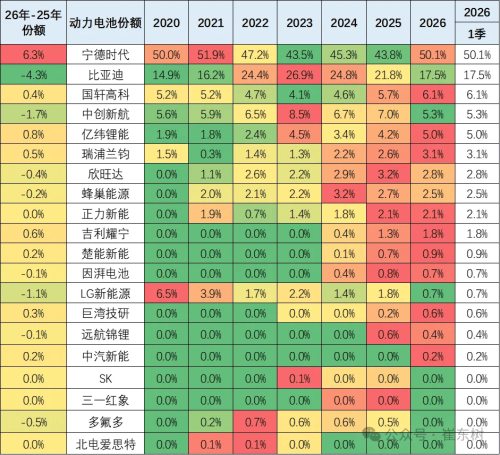

China’s power battery output reached 142 GWh in February 2026, up 19% year-on-year, according to data disclosed by Cui Dongshu, secretary general of the China Passenger Car Association. Among them, ternary batteries accounted for 26.9 GWh, while lithium iron phosphate (LFP) batteries contributed 114.6 GWh. Cumulative output for January-February stood at 310 GWh, representing a 22% increase year-on-year. Battery output for different battery types from December 2020 to February 2026 From an installation perspective, the ratio of battery output installed in vehicles has declined sharply. In 2025, around 44% of battery production was installed, but this dropped to 25% in January and further to 19% in February. While supply continues to expand, demand has weakened significantly, highlighting a growing supply-demand mismatch. Battery installation for different battery types from December 2020 to February 2026 Structurally, the installation rate for ternary batteries stood at 21%, while LFP batteries recorded 18%, both indicating historically low utilization levels. This trend is reflected in the end market. Domestic new energy vehicle installations in February totaled 370,000 units, down 47% year-on-year. Among them, battery electric passenger vehicles reached 236,000 units, down 41%, while plug-in hybrid passenger vehicles fell 61% to 100,000 units, underscoring pressure on consumer demand. For January-February, overall battery installations declined by 7%, although the commercial vehicle segment showed resilience. In February, battery electric trucks grew 6% year-on-year, while plug-in hybrid trucks surged 284%. EV battery installations across various vehicle types from 2020 to 2026 On the technology front, battery performance continues to improve. In the first quarter, the share of models with energy density above 160 Wh/kg rose to 15%, up from 9% in 2025, while products below 125 Wh/kg have largely exited the market, accelerating the phase-out of low-end capacity. In terms of competition, market concentration remains high. In the first quarter, CATL held a 50.1% market share, followed by BYD at 17.5%, with the two accounting for a combined 68%. Market share of different battery enterprises from 2020 to 2026 Among second-tier players, Gotion High-Tech, CALB, and EVE Energy held shares of 6.1%, 5.3%, and 5.0%, respectively. Notably, as BYD continues its full transition toward LFP technology, the remaining market space for ternary batteries is increasingly being absorbed by other manufacturers. Meanwhile, recent growth in high-end plug-in hybrid models has provided some support for the recovery of the ternary segment.