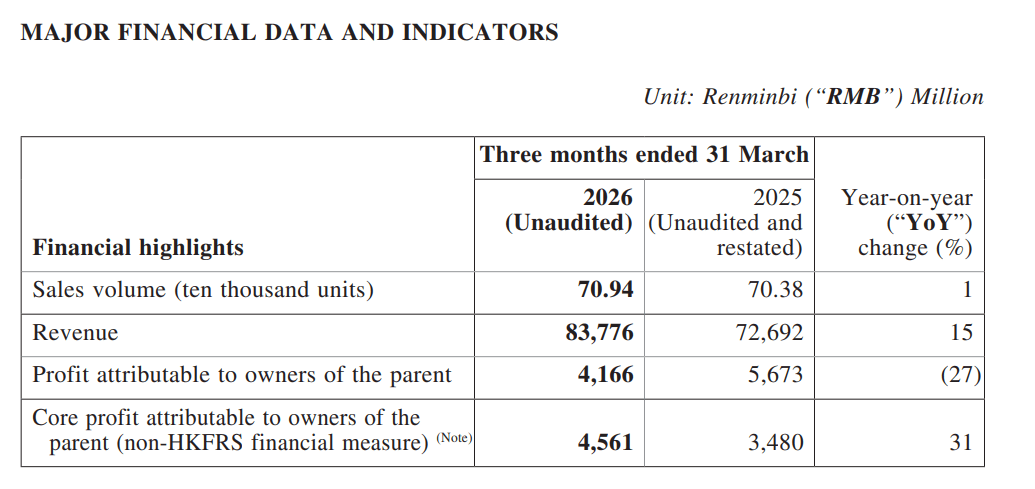

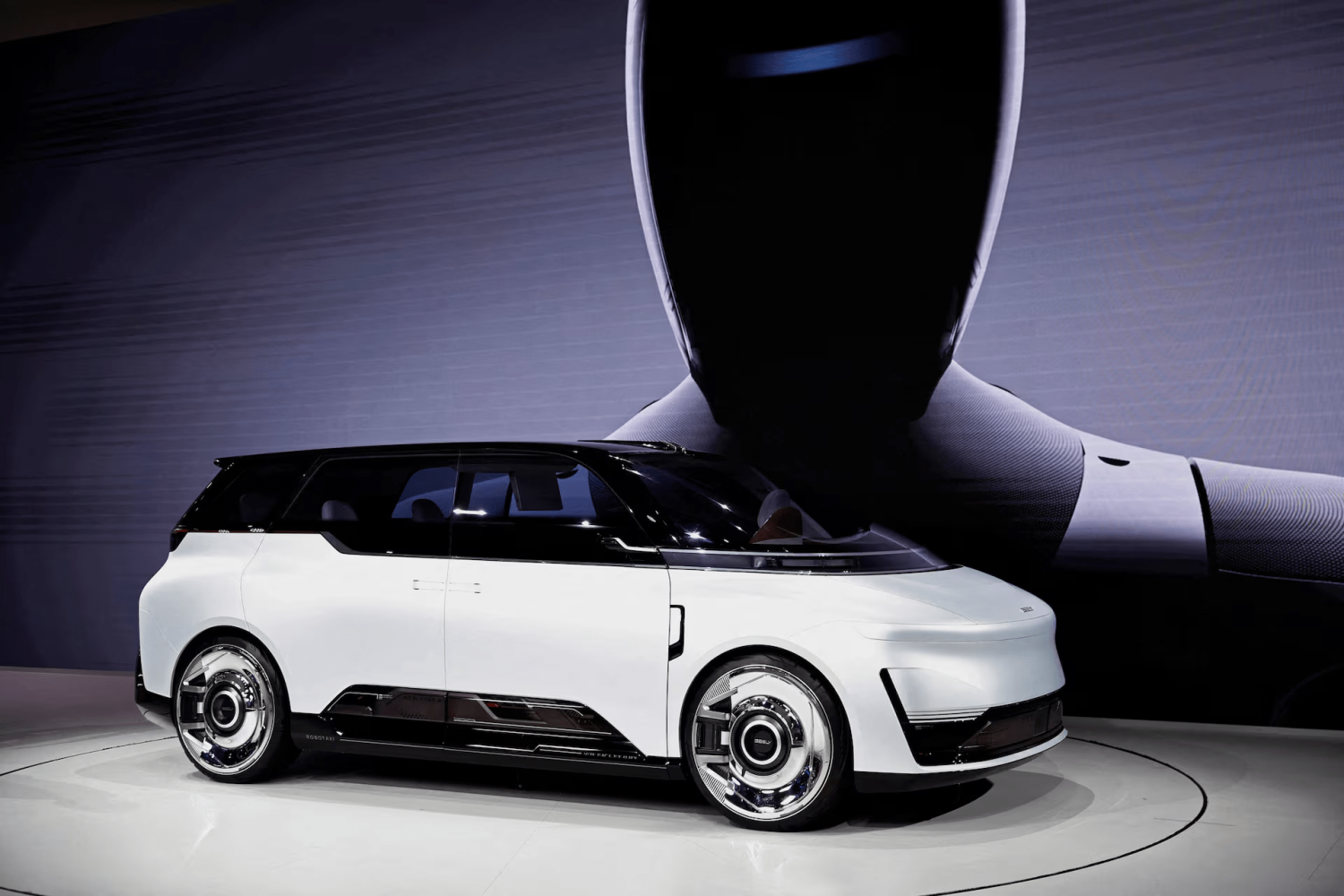

Geely Auto reported its first-quarter 2026 results on April 29, posting total revenue of RMB 83.8 billion ($12.26 billion), up 15% year-on-year. Core net profit attributable to shareholders reached RMB 4.56 billion ($667 million), up 31% year-on-year, with profit growth outpacing revenue expansion. Gross margin improved to 17.5%, up 11% year-on-year. During the quarter, both the administrative expense ratio and R&D spending ratio declined, falling 18% and 17% respectively. Cost compression combined with scale effects contributed to stronger profit release. As of the end of the quarter, the company held cash reserves of RMB 60.2 billion ($8.80 billion). Geely’s total vehicle sales reached 709,000 units in the first quarter, lifting its market share to 11.95% and making it the top-selling Chinese domestic brand. New energy vehicle sales—including Geely, Lynk & Co and Zeekr—totaled 369,000 units, up 9% year-on-year, with NEVs accounting for more than 52% of total sales. By brand, Geely is forming a clearer tiered structure. Zeekr is targeting the premium segment, and Lynk & Co remains positioned in the upper mid-range. Zeekr 8X displayed at Beijing Auto Show Galaxy focuses on the mass-market NEV segment, while the “China Star” lineup continues to anchor the internal combustion engine business. Overseas operations are emerging as a second growth engine. First-quarter exports reached 203,000 units, up 126% year-on-year. To date, Geely has expanded into more than 100 countries and regions, with over 1,900 sales and service outlets. The company has raised its internal export target to 750,000 units, up 17% from the previous goal of 640,000 units. On the technology front, Geely’s investments in intelligent driving are entering the commercialization phase. Its driver-assistance system “Qianli Haohan” has surpassed 600,000 users. Geely’s Robotaxi prototype, Eva Cab, displayed at Beijing Auto Show At the Beijing Auto Show, Geely unveiled China’s first purpose-built Robotaxi prototype, the Eva Cab, with plans to achieve L4 deployment by 2027. Capital markets have responded positively to the results. Major domestic and international investment banks, including JPMorgan, Morgan Stanley, Citi and BOCOM International, have recently issued “overweight” or “buy” ratings on the company.