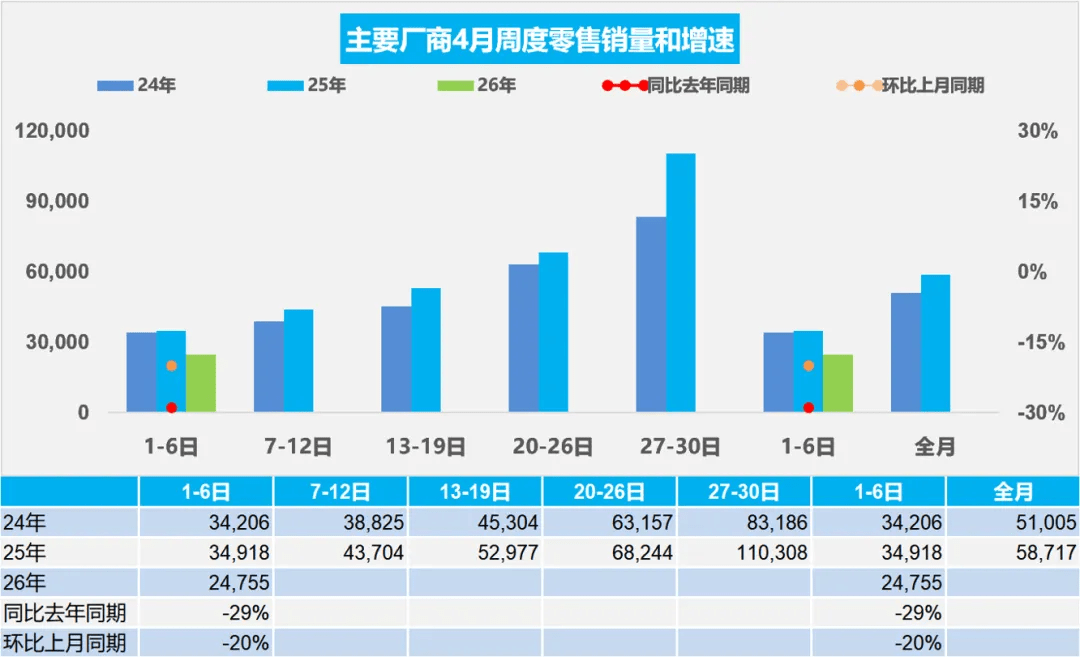

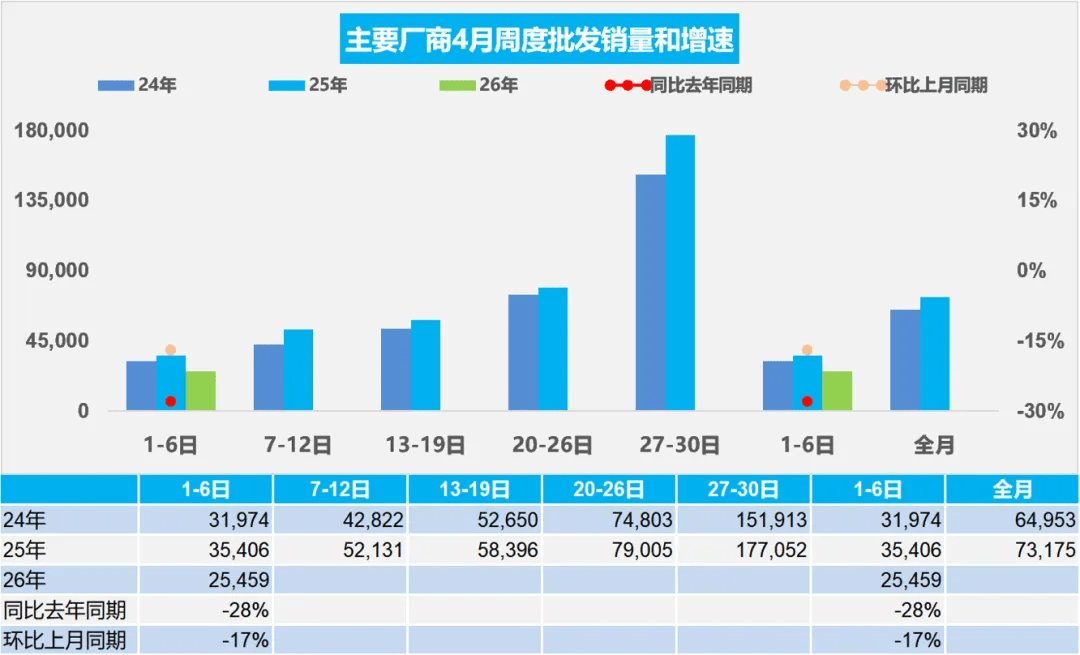

Latest data from the CPCA shows that from April 1 to 6, China’s passenger vehicle retail sales reached 149,000 units, down 29% year-on-year and 20% lower than the same period last month, with daily average retail sales of 25,000 units. Wholesale volumes also came under pressure. During the same period, passenger vehicle wholesale totaled 153,000 units, down 28% year-on-year and 17% lower month-on-month, with daily average wholesale of 25,000 units. The first week of April was affected by China’s Qingming holiday, which reduced effective selling and registration days. In addition, a late-March sales push pulled forward part of demand, leading to a noticeable slowdown in early April transactions. Monthly sales volume and growth rates for the years 2024, 2025, and 2026 Despite the overall market weakness, new energy vehicles remained the core support for the passenger car market. From April 1 to 6, NEV retail sales reached 86,000 units, down 24% year-on-year but up 3% compared with the same period in March, with penetration reaching 57.7%. On the wholesale side, sentiment was more cautious. NEV wholesale totaled 73,000 units, down 39% year-on-year and 14% lower than the same period last month, with penetration at 47.5%, below the retail level. This gap indicates that automakers are actively controlling shipments to reduce inventory rather than pushing stock into dealer channels. Monthly wholesales volume and growth rates for the years 2024, 2025, and 2026 The simultaneous contraction in supply and demand is also linked to external factors. Persistently high global oil prices are raising vehicle usage costs, while a decline in domestic equity markets is affecting household asset income, leading to more conservative consumer sentiment and a stronger wait-and-see attitude. From a production perspective, structural divergence has become more evident. In the first week of April, output of conventional fuel-powered light vehicles reached 176,000 units, down 6% year-on-year but up 7% compared with the same period last month. Meanwhile, production of hybrid and plug-in hybrid models reached 85,000 units, up 16% year-on-year and 60% higher than the same period last month, indicating that automakers continue to shift toward electrification. Overall, the retail market remains in a phase of demand consolidation. With the upcoming Beijing Auto Show and a wave of new model launches later in the month, retail performance is expected to gradually stabilize and recover, with market momentum likely to improve in the second half of April.