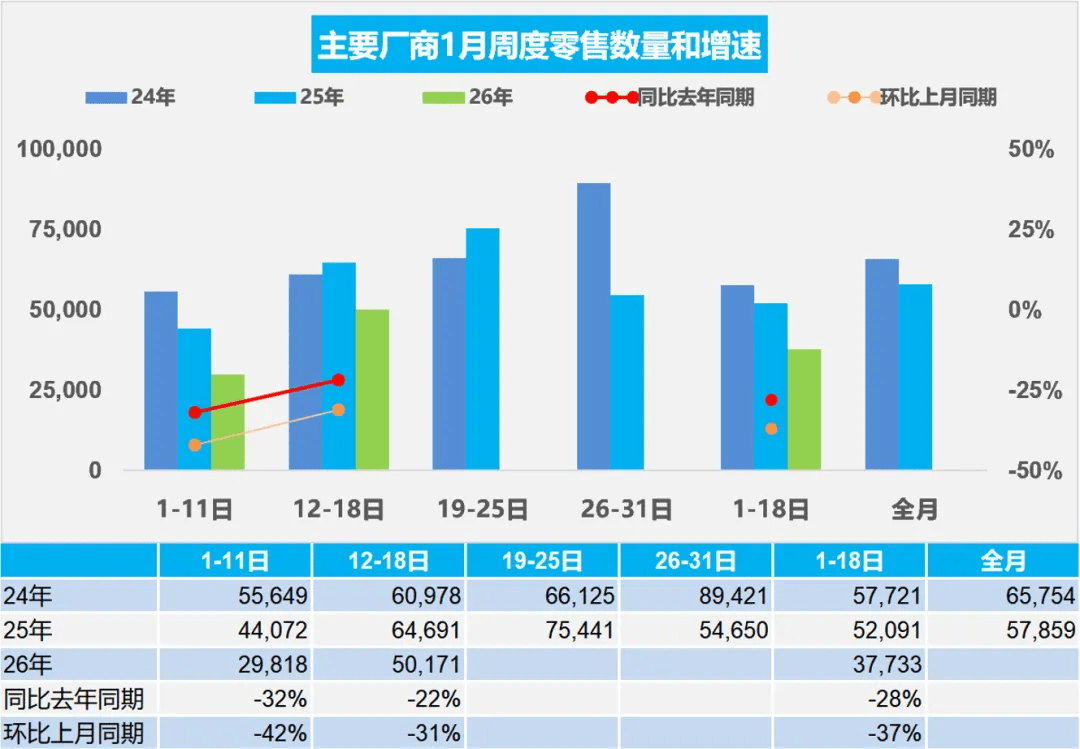

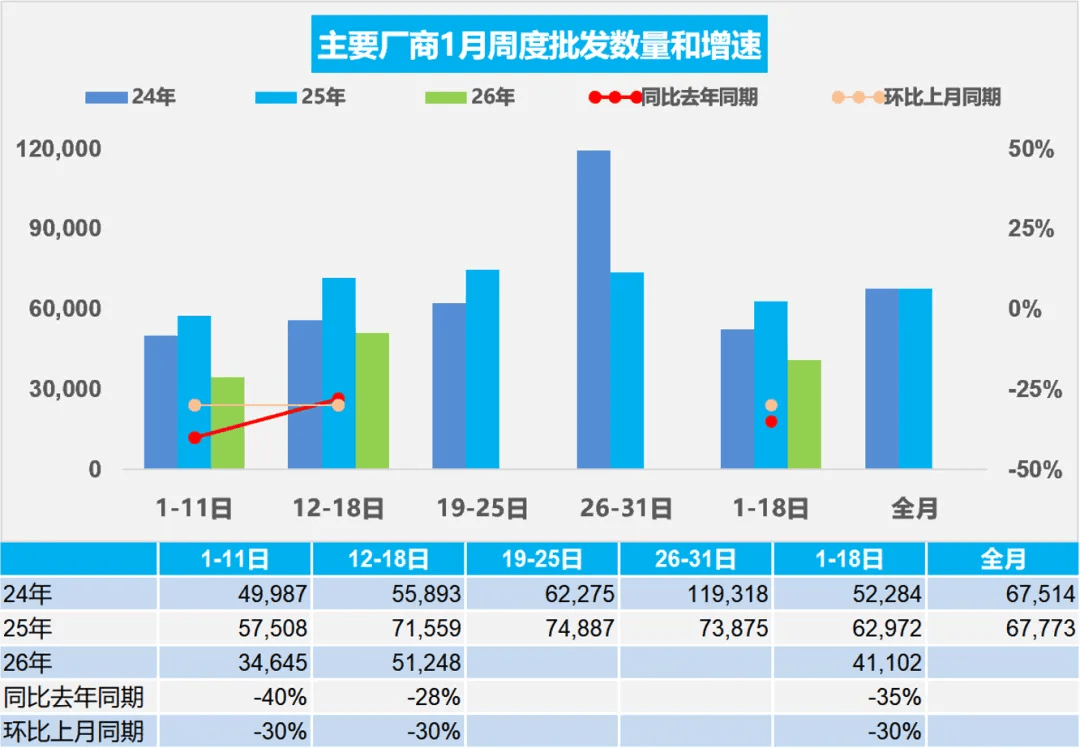

China’s retail sales of NEV passenger cars reached 312,000 units in Jan 1-18, down 16% YoY and 52% MoM, with NEV penetration slipping to 46%. Latest data from the China Passenger Car Association show that China’s retail sales of passenger vehicles totaled 679,000 units in Jan 1–18, down 28% year on year (YoY) and 37% month on month (MoM). Wholesale volumes weakened in tandem. Passenger car manufacturers recorded cumulative wholesale sales of 740,000 units over the same period, representing a YoY decline of 35% and a MoM drop of 30%, indicating a clear early-year downturn in the overall auto market. The new energy vehicle segment also came under pressure. From Jan. 1 to Jan. 18, China’s retail sales of NEV passenger cars reached 312,000 units, down 16% YoY and 52% MoM, with NEV penetration slipping to 46%. On the wholesale side, cumulative NEV passenger car volumes stood at 348,000 units, down 23% YoY and 46% MoM, with wholesale penetration falling to 47%. Both retail and wholesale NEV sales contracted more sharply than the broader passenger car market. Monthly sales volumes and growth rates for the years 2024, 2025, and 2026 From a production perspective, the decline in conventional internal combustion vehicles was even more pronounced. In the first two weeks of January, nationwide production of pure fuel-powered light vehicles totaled 91,000 units, plunging 85% YoYr and 77% MoM. Combined production of hybrid and plug-in hybrid models reached 139,000 units, down 65% YoY and 75% MoM. Automakers clearly slowed production early in the year, reflecting a strong focus on inventory control. Weekly data point to tentative signs of stabilization at low levels. In the first week of January, average daily retail sales of passenger cars stood at 30,000 units, rising to 50,000 units in the second week. Monthly wholesales volumes and growth rates for the years 2024, 2025, and 2026 While retail activity showed some recovery, overall market conditions remained subdued. The expiration of purchase tax incentives, combined with China’s later Lunar New Year this year, amplified the YoY decline. As local subsidy details are gradually finalized and incentive channels reopen, there remains potential for pent-up demand to be released ahead of the holiday. Wholesale trends broadly mirrored retail performance. Average daily wholesale volumes were 35,000 units in the first week of January, increasing to 51,000 units in the second week. Under pre-order-based sales models, some automakers continue to hold a backlog of undelivered orders, suggesting that wholesale adjustments are largely temporary. Overall, the early-January weakness in China’s auto market appears to be driven primarily by policy transitions and the timing shift of the Lunar New Year. The National Development and Reform Commission announced a new vehicle trade-in program on Dec. 30 last year, which is expected to provide additional support for auto consumption in January.

![Gasgoo, NIO, [Gasgoo Express] NIO's William Li Discusses ES9 Design, Saying Originality is Difficult but Must Be Done; March Passenger Vehicle Exports Reach 695,000 Units](https://cdn.topcarnews.net/media/id/aHR0cHM6Ly9pbWFnZWNuLmdhc2dvby5j-b20vbW9ibG9nby9OZXdzL1VFZGl0b3Iv-aW1hZ2UvMjAyNTA2MTAvNjM4ODUxNzAw-MTkzODM1OTU2NTQxNDEzNi5qcGc/c06991c2ffe2e05fe81c97062ebd8cf3.jpg?t=20260727&post_id=14615)