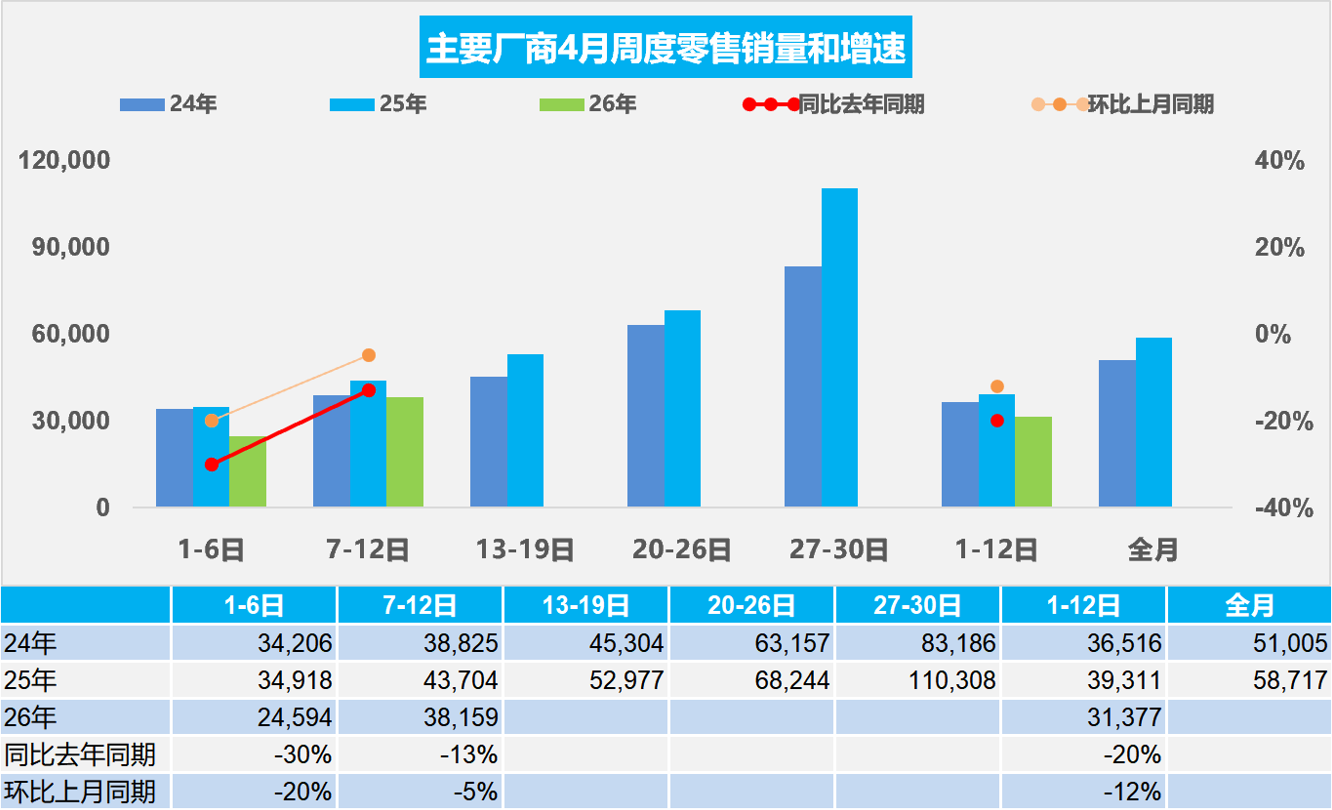

Gasgoo Munich- The China Passenger Car Association (CPCA) released market data covering the first two weeks of April (April 1-12), 2026. The figures show a synchronized decline in both retail and wholesale passenger car sales. New energy vehicles (NEVs) outperformed internal combustion engine (ICE) models, pushing retail penetration past 59%. However, the broader market remains sluggish. Mounting pressure on dealer channels is a critical industry challenge.Image Source: CPCAFrom April 1 to 12, nationwide retail sales reached 377,000 units, a 20% year-on-year drop and a 12% sequential decline. Year-to-date retail sales totaled 4.598 million units, down 18%. Wholesale sales reached 374,000 units during the same period, marking a 29% annual plunge and a 21% sequential slip. Cumulative wholesale volumes for the year stood at 6.241 million, an 8% decrease. Both supply and demand are losing steam, marking a tough start to the period.The NEV sector demonstrated structural resilience. NEV retail sales hit 224,000 units in the first two weeks of April. This represents an 11% year-on-year drop but a 7% increase from March. The retail penetration rate rose to 59.5%. Wholesale volumes reached 199,000 units, a 29% annual drop and a 15% monthly decline. The wholesale penetration rate was 53.2%. Production trends underscored the deepening divide. Pure ICE production slumped 31% year-on-year, while hybrids and plug-in hybrids edged down just 1%.Weekly trends followed a pattern of "slow start, gradual recovery." Daily retail sales averaged 25,000 units in the first week of April. This represents a 30% year-on-year slump and a 20% week-on-week drop. The Qingming holiday and post-quarter cooldown hampered demand. By the second week, daily retail averages recovered to 38,000 units. This is a 13% annual drop and a 5% sequential decline, signaling a modest rebound. The wholesale side remained weak for two consecutive weeks. Daily averages were 25,000 and 37,000 units respectively. Both weeks saw annual declines near 30% as manufacturers tightened supply schedules.Several factors weighed on market performance. Rising international oil prices drove up ownership costs. Fragile consumer confidence cooled demand at the showroom level. Intense anticipation for new models and the approaching Beijing Auto Show encouraged consumers to hold off on purchases. Stable pricing also contributed to this wait-and-see approach. After two consecutive quarters of year-on-year declines, dealers face a dilemma. Selling cars yields no profit, yet not selling results in greater losses. With manufacturers offering limited subsidies, channel pressure is the central issue facing the retail sector.The weakness in wholesale volumes reflects a passive adjustment to sluggish terminal demand. It is also a rational move by automakers to manage inventory and alleviate channel pressure. As the market adapts to high oil prices and inventory burdens ease, the industry expects a gradual recovery. The Beijing Auto Show in late April will drive this trend. The growth gap between wholesale and retail sales is projected to narrow accordingly.Overall, the market remains in an adjustment phase. The persistently high NEV penetration rate acts as a stabilizer. However, it has not fully offset the sharp decline in ICE vehicle sales. The industry urgently needs to improve market conditions and ease channel pressure. This will steer the market back toward a trajectory of steady growth.