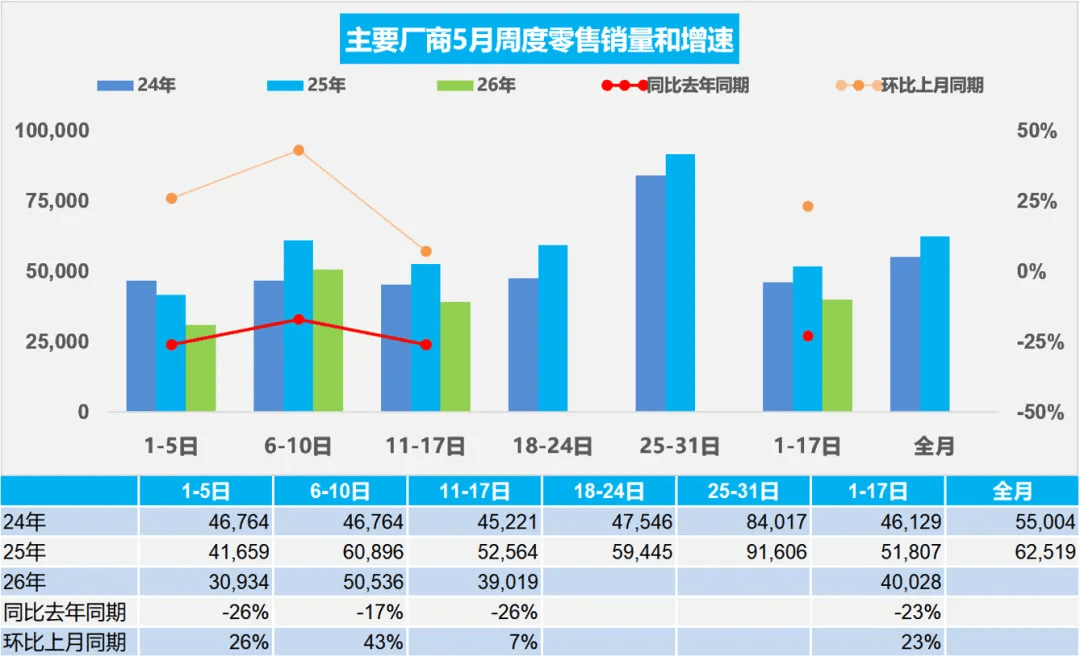

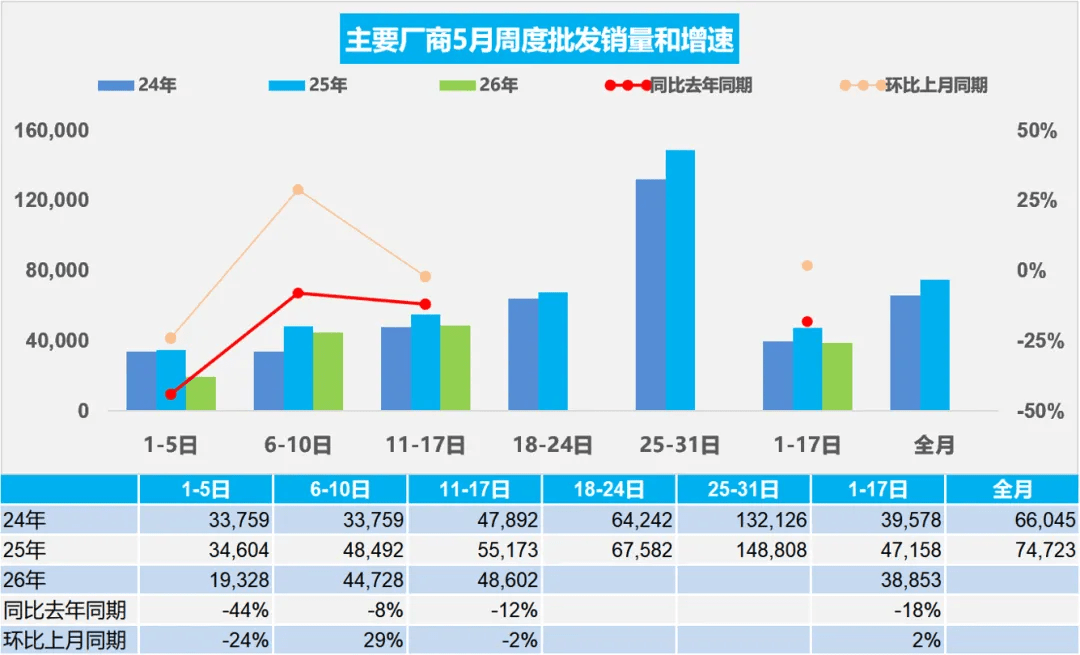

Latest data from CPCA showed that China’s passenger vehicle retail sales totaled 680,000 units during May 1–17, down 23% year-on-year, though up 23% compared with the same period in April. Cumulative retail sales this year reached 6.285 million units, down 19% year-on-year. From a weekly perspective, the May market followed a typical “post-holiday rebound followed by renewed slowdown” pattern. During the Labor Day holiday period, showroom traffic remained relatively weak, with average daily retail sales in the first week reaching only 31,000 units. In the second week, backlogged holiday orders were released, lifting average daily retail sales to 51,000 units, before falling back to 39,000 units in the third week. Weekly sales volume and growth rates for the years 2024, 2025, and 2026 Wholesale performance was also relatively soft. From May 1–17, passenger vehicle wholesale volumes nationwide totaled 660,000 units, down 18% year-on-year and up only 2% from the previous month. Cumulative wholesale volume this year reached 8.637 million units, down 7% year-on-year. Many automakers have recently begun proactively adjusting production schedules to reduce inventory pressure across dealer channels. In comparison, new energy vehicles (NEVs) remained the market’s primary growth driver. Between May 1 and 17, NEV passenger vehicle retail sales reached 400,000 units, down 12% year-on-year but up 18% month-on-month. NEV penetration climbed to 58.9%. Over the same period, NEV passenger vehicle wholesale volume reached 396,000 units, down 9% year-on-year but up 12% month-on-month, with penetration further increasing to 59.9%, even higher than the retail level. Weekly wholesales volume and growth rates for the years 2024, 2025, and 2026 On a cumulative basis, NEV retail sales this year reached 3.158 million units, down 17% year-on-year, while cumulative NEV wholesale volume totaled 4.349 million units, down 2%. From the production side, internal combustion engine vehicle capacity continued to contract, while hybrid and plug-in hybrid models increasingly became a key buffer supporting sales stability for many automakers. During the first three weeks of May, production of gasoline-powered light vehicles totaled 284,000 units, down 41% year-on-year and down 31% from the previous month’s comparable period. Meanwhile, hybrid and plug-in hybrid vehicle production reached 197,000 units, down 14% year-on-year but up 3% month-on-month. Looking ahead, the CPCA expects the market to enter another sales push phase over the coming weeks. Based on historical trends, late May typically sees a new round of retail incentives, while automakers begin building momentum toward mid-year sales targets. In the near term, NEVs and low-cost entry-level models are expected to remain the most resilient segments of the market, while traditional gasoline vehicles — particularly mid- to high-end joint-venture brands — are likely to face mounting pressure.