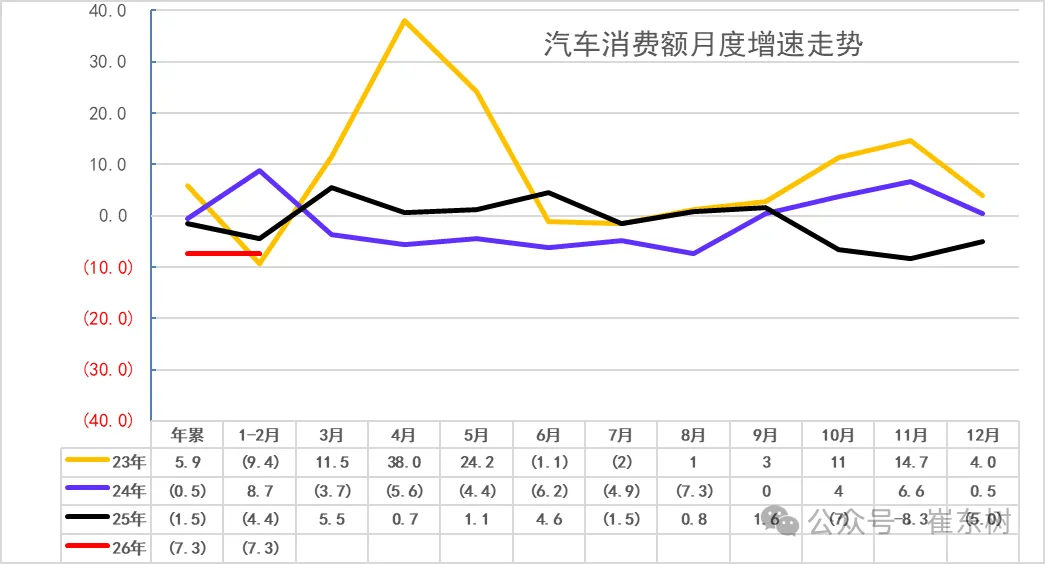

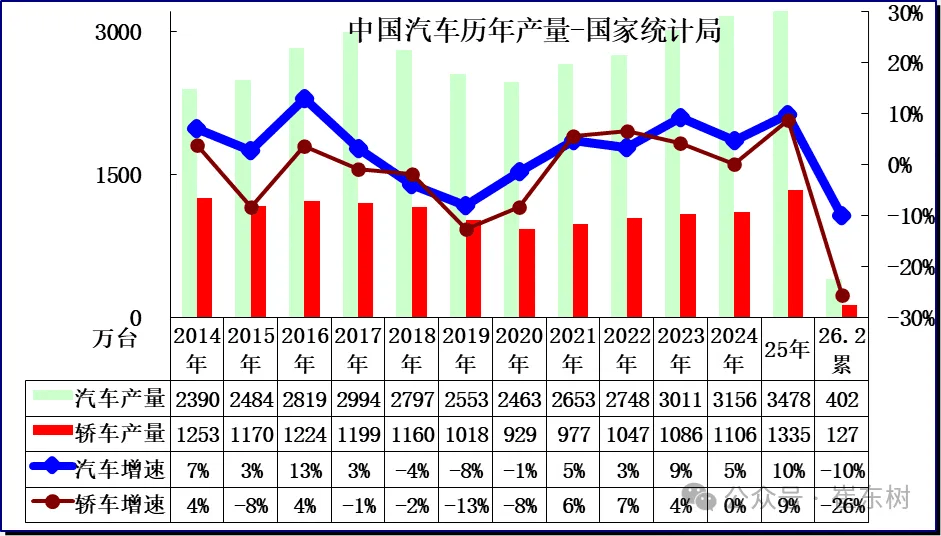

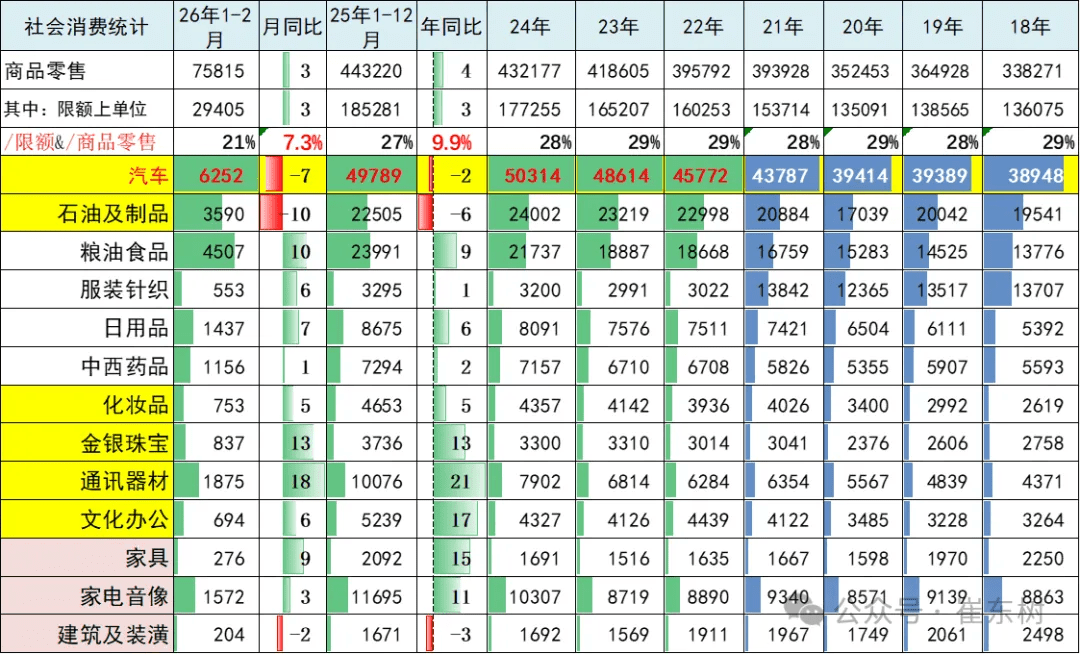

China’s industrial output rose 6.3% YoY in Jan-Feb 2026, while auto sector growth trailed at 3.4%. Cui Dongshu, Secretary-General of the China Passenger Car Association (CPCA), released a research report on the automotive market for January-February 2026. The data shows that in the first two months of 2026, the market clearly exhibited structural characteristics of “stable investment growth alongside production and sales pressure”. First, let’s look at a set of core data (for the period of January-February 2026): Automotive Investment: Increased by 2.6% year-on-year, higher than the national average of 1.8% for fixed asset investment (excluding rural households). Automotive Production: Total output reached 4.02 million units, a decrease of 10% year-on-year. New Energy Vehicles (NEVs): Production stood at 1.60 million units, a decrease of 14% year-on-year, with a penetration rate of 40%. Fuel Vehicles: Production reached 2.42 million units, a decrease of 7% year-on-year. Automotive Consumption: Total retail sales amounted to 625.2 billion yuan, a decrease of 7% year-on-year, while retail sales of consumer goods excluding automobiles grew by 3.7%. Growth trend of monthly auto consumption value From the production perspective, in January-February 2026, the added value of industrial enterprises above the designated size increased by 6.3% year-on-year. However, the added value of the automotive industry only grew by 3.4%, a significant slowdown compared to the 11.5% growth for the full year of 2025. In terms of output, total vehicle production was 4.024 million units, a decrease of 9.9%. Among this, NEV production was 1.604 million units, down 13.7%, with the penetration rate dropping to 40% from 48% for the full year of 2025. Cui Dongshu’s analysis points out that the decline in production is mainly due to the combined impact of a high base in the same period last year, the contraction of policy-driven demand at the end of 2025, and this year’s sharp reduction in subsidies for micro electric vehicles. Looking at a longer cycle, after experiencing rapid growth from 2022 to 2025 (with the penetration rate jumping from 26% to 48%), the 40% NEV penetration rate in January-February this year represents a periodic adjustment, yet it remains at a high level. China’s auto production over the years Automotive consumption value in January-February fell by 7% year-on-year, forming a stark contrast with the 3.7% growth in retail sales of consumer goods excluding automobiles. Cui Dongshu analyzed the connection between the real estate market and the auto market. The report indicates that since the property market entered an adjustment cycle in 2021, total automotive consumption has steadily increased from 3.94 trillion yuan in 2020 to 4.98 trillion yuan in 2025, suggesting that the crowding-out effect of housing investment on consumption has somewhat eased. Data shows that the current ratio of auto sales to real estate sales is approximately 23 square meters of housing sold per vehicle. Although this is a significant improvement compared to 70 square meters per vehicle in 2020, pressure still exists. Despite the pressure on production and sales data, fixed asset investment in the automotive industry increased by 2.6% year-on-year, outperforming the average level across all industries nationwide. Social consumption statistics In his analysis, Cui Dongshu emphasized that challenges such as insufficient effective demand and a lack of market vitality persist in the automotive industry, making the task of stabilizing growth arduous. He pointed out that the relatively weak subsidy intensity for passenger vehicles under the 2025 trade-in policy is one of the reasons for the current high pressure on passenger car consumption.