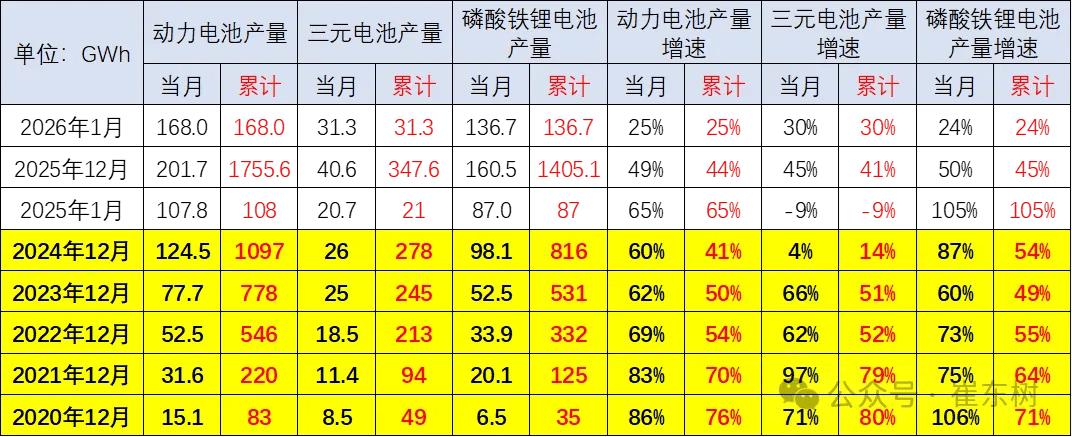

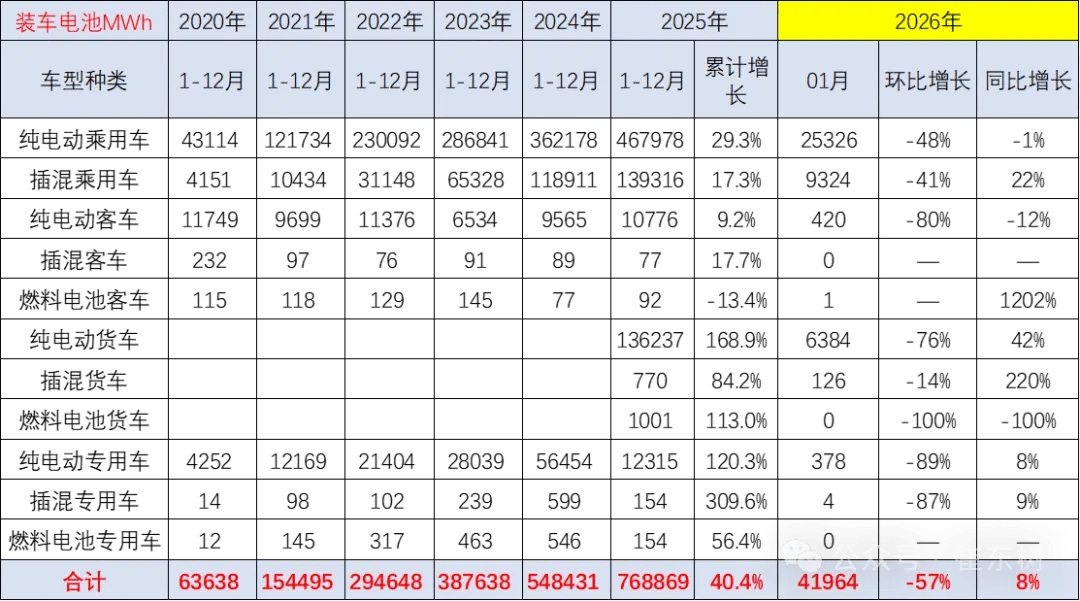

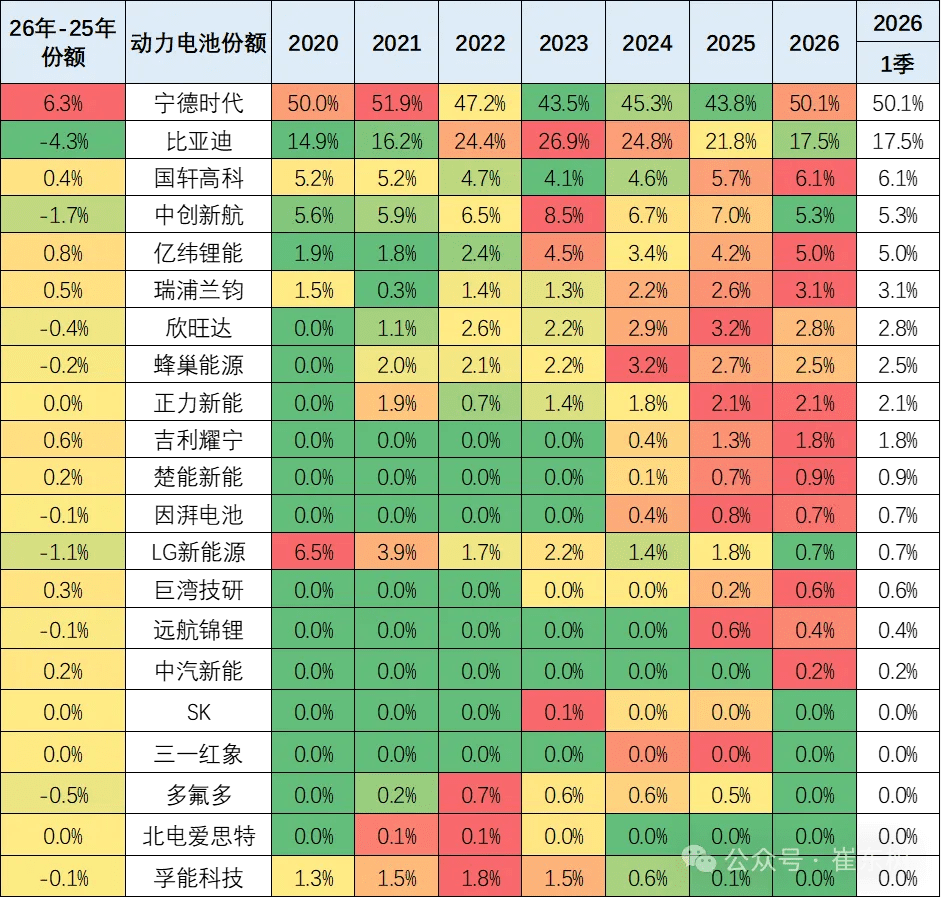

CATL and BYD retained a combined 67% market share, with ternary competition concentrated among leading suppliers. Latest data disclosed by Cui Dongshu, secretary general of the China Passenger Car Association, show that China’s combined output of power and other batteries reached 168 GWh in January 2026, up 25% year on year. However, vehicle installation data point to a weak start to the year. In 2025, about 44% of power battery output was installed in vehicles, but in January 2026 the ratio fell to 25%, marking a cyclical low. Battery production quantities and growth rates for different battery types from December 2020 to January 2026 By chemistry, the installation rate for ternary lithium batteries stood at 30%, compared with 24% for lithium iron phosphate batteries. The year-end surge in new energy vehicle production did not carry into January, leaving battery manufacturers facing inventory destocking pressure at the start of the year. Based on downstream estimates, domestic new energy vehicle installations totaled around 700,000 units in January, down 12% year on year. Battery electric passenger vehicles accounted for 398,000 units, down 17%, while plug-in hybrid passenger vehicles reached 269,000 units, down 6%. Battery electric commercial-purpose vehicles totaled 29,700 units. Overall momentum remained subdued, with clear structural divergence across segments. Battery demand from passenger vehicles remained relatively resilient, with installed capacity reaching 42 GWh, up 8% year on year. Electric vehicle battery installations across various vehicle types from 2020 to 2026 Commercial vehicles showed comparatively strong performance: battery electric trucks rose 42% year on year, while plug-in hybrid trucks surged 220%. In terms of installation share, battery electric passenger vehicles retained the largest proportion, followed by plug-in hybrid passenger vehicles in second place and battery electric trucks in third. On the technology front, vehicles equipped with battery systems exceeding 160 Wh/kg energy density accounted for 13% in the first quarter of 2026, up from 9% in 2025. Ternary chemistry saw a recovery, supported by demand for high-end plug-in hybrids. Products with energy density below 125 Wh/kg accounted for 0%, indicating accelerated phase-out of low-end capacity. Market share of different battery enterprises from 2020 to 2026 The competitive landscape remained dominated by CATL and BYD, whose combined market share held at around 67%, leaving slightly over 30% for other players. As BYD has fully transitioned to lithium iron phosphate batteries, the competitive edge in ternary batteries has become more concentrated among CATL, SVOLT, CALB and LG Energy Solution.