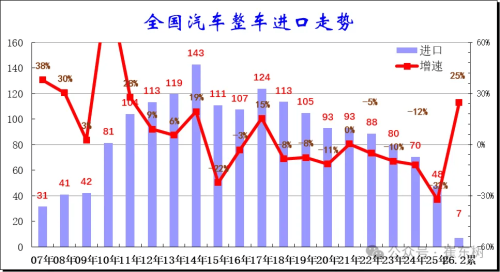

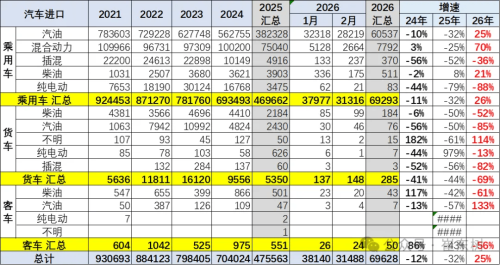

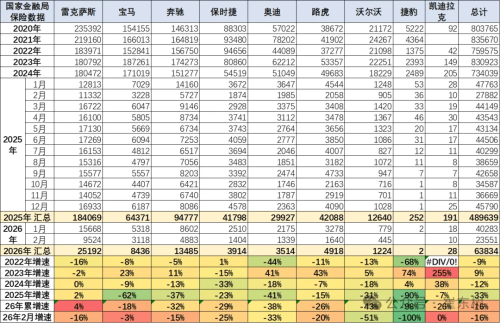

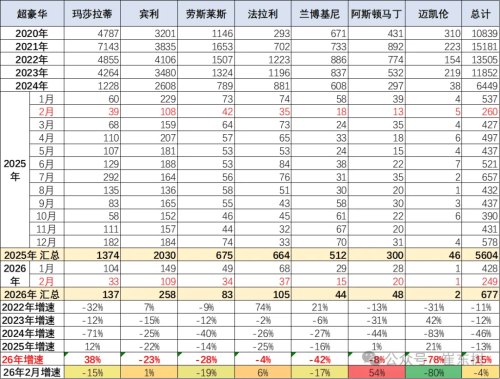

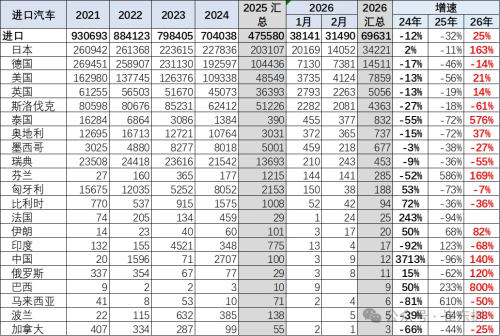

Latest data released by CPCA Secretary General Cui Dongshu show that China imported 70,000 vehicles in January–February 2026, up 25% year-on-year. In February alone, imports reached 32,000 units, down 12% year-on-year and 17% month-on-month, indicating a gradual normalization of market growth. Looking at the longer-term trend, the contraction is more evident. Since 2018, China’s vehicle import volume has been on a sustained downward trajectory. Adjusted for cyclical fluctuations, the market has weakened for eight consecutive years. Trend of China’s vehicle imports and growth rates from 2007 to Feb 2026 Total imports in 2025 fell to 480,000 units, down 32% year-on-year and significantly below the peak of 1.43 million units in 2014. The key drivers behind this decline are the rising competitiveness of domestic vehicles and the accelerated localization of production by multinational automakers. Structural changes are also pronounced. In the first two months of 2026, passenger vehicles accounted for over 99% of total imports, with sedans making up 46% and four-wheel-drive SUVs 25%. In terms of powertrain mix, the import market has effectively reverted to the “fuel era,” with new energy passenger vehicles accounting for just 1%. Battery electric vehicle imports plunged 88% year-on-year, while plug-in hybrids declined 36%, making them the most contracted segment. Auto import data across different types from 2021 to Feb 2026 This trend stands in stark contrast to China’s export market. As domestic NEV penetration continues to rise, imported NEVs are losing competitiveness in the local market. At the brand level, the support base for imports is narrowing, increasingly reliant on demand for luxury vehicles. In January–February 2026, Lexus imported 25,192 units, up 4% year-on-year, maintaining its position as the leading imported luxury brand, with its hybrid lineup continuing to attract stable demand. Import data of luxury auto brands from 2020 to Feb 2026 In contrast, ultra-luxury brands weakened overall, with imports down 15%. Bentley and Rolls-Royce recorded subdued performance, with total imports of 258 and 83 units respectively in the first two months. Ferrari saw a 6% year-on-year increase in February imports, but this was insufficient to reverse the broader downward trend. Notably, non-luxury imported vehicles have nearly disappeared. As domestic brands and localized joint-venture models substitute traditional import segments, the space for imported mainstream vehicles is rapidly shrinking, particularly for European brands. Import data of ultra-luxury auto brands from 2020 to Feb 2026 By country of origin, China’s passenger vehicle imports remain concentrated in Japan, Germany, the United States, Slovakia and the United Kingdom, with U.S. imports notably affected by tariffs. In January–February 2026, Japan ranked first with 34,221 imported vehicles, followed by Germany with 14,511 units, the United States with 7,859 units, the United Kingdom with 5,056 units and Slovakia with 4,363 units. Auto import statistics across various countries from 2021 to Feb 2026 Meanwhile, pressure on imported NEVs continues to intensify, with imports from major source countries declining 64%.