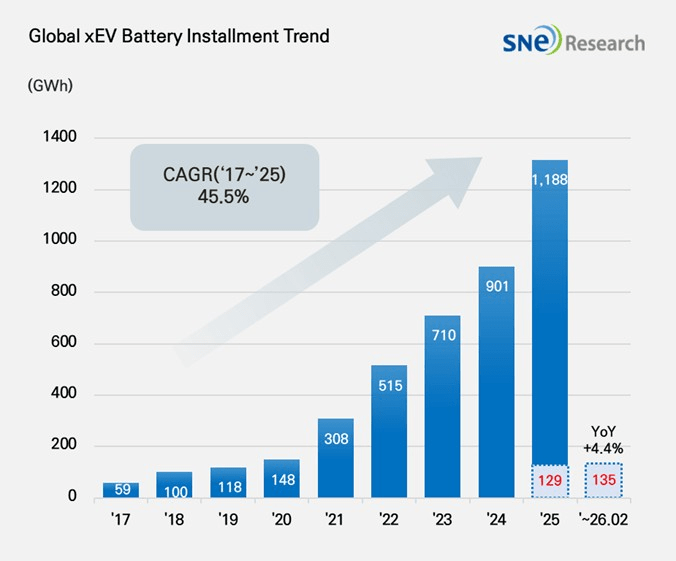

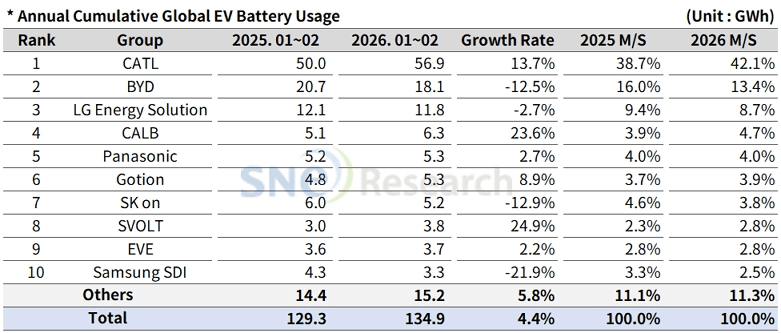

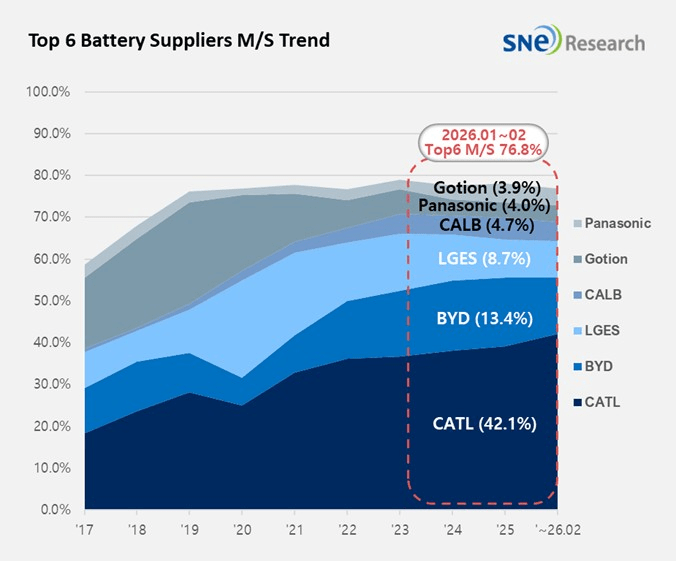

A recent report released by South Korean market research firm SNE Research shows that global electric vehicle (EV, PHEV, HEV) battery installations reached approximately 135 GWh in January–February 2026, up 4.4% year-on-year. In February alone, installations totaled 63 GWh, down 12.5% from 72 GWh in January. Global EV battery installment trend From a competitive landscape perspective, Chinese battery manufacturers continue to dominate. Among the global top 10 battery suppliers, six are Chinese companies, with a combined installation volume of 94.1 GWh, up 8% year-on-year, accounting for 69.7% of total market share. Among them, CATL and BYD remain firmly ranked as the world’s top two battery suppliers, with a combined installation volume of 75 GWh, representing 55.5% of the global market. Specifically, CATL maintained its leading position with 56.9 GWh of installed capacity in the first two months, up 13.7% from 50 GWh in the same period last year. Gloval top 10 battery suppliers by installations in Jan-Feb from 2025 to 2026 Its market share reached 42.2%, further widening the gap with the second-place player. During the same period, BYD recorded 18.1 GWh of battery installations, down 12.5% year-on-year, but still retained its No.2 global ranking. Its market share declined from 16% to 13.4%. The report noted that the decline in BYD’s battery usage was mainly driven by weaker domestic vehicle sales. Data shows that BYD’s total vehicle sales in January–February were around 400,000 units, down 35.8% year-on-year, weighing on battery installation volumes. However, overseas performance provided partial offset. BYD’s exports exceeded 200,000 units during the same period, up 50.78% year-on-year. In February alone, overseas sales surpassed 100,000 units, accounting for 52.6% of total monthly sales, exceeding domestic sales for the first time. Top 6 battery suppliers from 2017 to Feb 2026 Other Chinese battery makers are also expanding their presence. CALB ranked fourth globally with 6.3 GWh of installations, up 23.6% year-on-year. Gotion High-Tech, EVE Energy and SVOLT ranked sixth, eighth and ninth respectively, with installation volumes of 5.3 GWh, 3.8 GWh and 3.7 GWh, representing year-on-year growth of 8.9%, 24.9% and 2.2%. In contrast, South Korea’s three major battery manufacturers saw their combined market share decline. LG Energy Solution, SK On and Samsung SDI together accounted for 15% of the market, down from 17.3% in the same period last year.

![BYD, BYD confirms new flagship EV has a range of 1,008 km [Video]](https://cdn.topcarnews.net/thumb/id/aHR0cHM6Ly9pMC53cC5jb20vZWxlY3Ry-ZWsuY28vd3AtY29udGVudC91cGxvYWRz-L3NpdGVzLzMvMjAyNi8wNy9CWUQtR3Jl-YXQtSGFuLUZsYWdzaGlwLUVWLmpwZWc_-dz0xNTAwJmFtcDtxdWFsaXR5PTgyJmFt-cDtzdHJpcD1hbGwmYW1wO3NzbD0x/c37374468f3a539ee1e0ce2b627e08d0.jpeg?t=20260731&post_id=48318)

![BYD, BYD confirms new flagship EV has a range of 1,008 km [Video]](https://cdn.topcarnews.net/thumb/id/aHR0cHM6Ly9pMC53cC5jb20vZWxlY3Ry-ZWsuY28vd3AtY29udGVudC91cGxvYWRz-L3NpdGVzLzMvMjAyNi8wNy9CWUQtR3Jl-YXQtSGFuLUZsYWdzaGlwLUVWLXJhbmdl-LmpwZz9zdHJpcD1pbmZvJmFtcDt3PTE0-NDAmYW1wO3NzbD0x/920438ef47ea4b64276e2d118cbc44a4.jpg?t=20260731&post_id=48318)

![BYD, BYD confirms new flagship EV has a range of 1,008 km [Video]](https://cdn.topcarnews.net/thumb/id/aHR0cHM6Ly9pMC53cC5jb20vZWxlY3Ry-ZWsuY28vd3AtY29udGVudC91cGxvYWRz-L3NpdGVzLzMvMjAyNi8wNy9CWUQtR3Jl-YXQtSGFuLUZsYWdzaGlwLUVWLTEuanBn-P3N0cmlwPWluZm8mYW1wO3c9MjAwMCZh-bXA7c3NsPTE/ec58de9827d67dc3cc45f86d6bcc427c.jpg?t=20260731&post_id=48318)

![BYD, BYD confirms new flagship EV has a range of 1,008 km [Video]](https://cdn.topcarnews.net/thumb/id/aHR0cHM6Ly9pMC53cC5jb20vZWxlY3Ry-ZWsuY28vd3AtY29udGVudC91cGxvYWRz-L3NpdGVzLzMvMjAyNi8wNy9CWUQtR3Jl-YXQtSGFuLUZsYWdzaGlwLUVWLWZyb250-LmpwZz9zdHJpcD1pbmZvJmFtcDt3PTIw-MDAmYW1wO3NzbD0x/819af4faa5c9804a09497b7d33d39bc1.jpg?t=20260731&post_id=48318)

![BYD, BYD confirms new flagship EV has a range of 1,008 km [Video]](https://cdn.topcarnews.net/thumb/id/aHR0cHM6Ly9pMC53cC5jb20vZWxlY3Ry-ZWsuY28vd3AtY29udGVudC91cGxvYWRz-L3NpdGVzLzMvMjAyNi8wNy9CWUQtR3Jl-YXQtSGFuLUZsYWdzaGlwLUVWLXJlYXIu-anBnP3N0cmlwPWluZm8mYW1wO3c9MjAw-MCZhbXA7c3NsPTE/25142d787c42fc350bb7230fb0006a37.jpg?t=20260731&post_id=48318)

![BYD, BYD confirms new flagship EV has a range of 1,008 km [Video]](https://cdn.topcarnews.net/thumb/id/aHR0cHM6Ly9pMC53cC5jb20vZWxlY3Ry-ZWsuY28vd3AtY29udGVudC91cGxvYWRz-L3NpdGVzLzMvMjAyNi8wNy9CWUQtR3Jl-YXQtSGFuLUZsYWdzaGlwLUVWLXNpZGUu-anBnP3N0cmlwPWluZm8mYW1wO3c9MjAw-MCZhbXA7c3NsPTE/cc2fac4025c1ccea61860176a17cec12.jpg?t=20260731&post_id=48318)