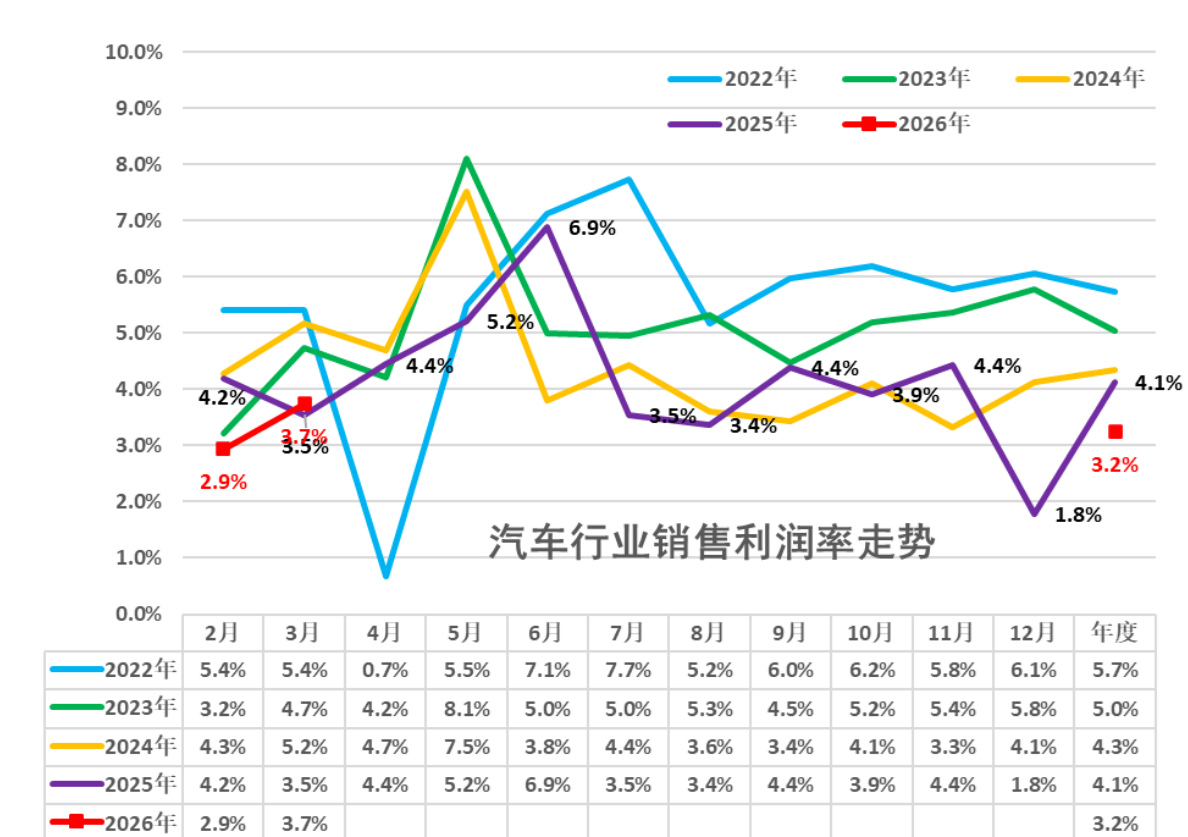

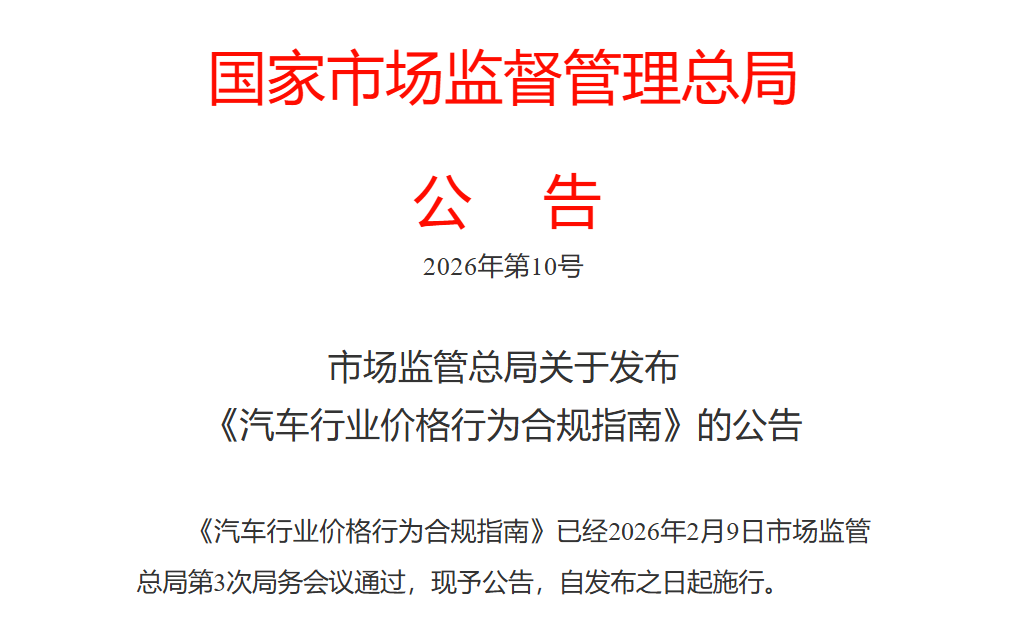

Gasgoo Munich- In the first quarter of 2026, China's auto industry released a striking set of figures. Citing statistics from Cui Dongshu's official account, industry profit fell 18% year-on-year, with the sales profit margin sinking to a low of 3.2%. Viewed through the lenses of cost and supply chain profit distribution, this phenomenon reflects deep structural pressures facing the auto sector.High Upstream Costs Squeeze Auto Industry Profit MarginsAccording to data cited by Cui Dongshu, China's auto output from January to March 2026 stood at 7.15 million units, a 6% drop from the previous year. Total industry revenue came in at approximately 2.41 trillion yuan, a slight dip of 0.2%, while total costs climbed 0.7% to 2.14 trillion yuan.Image Source: Cui DongshuSqueezed by falling revenue and rising costs, total auto industry profit for the quarter was just 78.4 billion yuan—an 18% plunge that pushed the sales profit margin down to 3.2%. Although margins improved to 3.7% in March from 2.9% in the first two months, they still lag significantly behind the 6% average seen in downstream industrial sectors.From a broader industry perspective, this profit decline is closely tied to persistently high upstream raw material prices.Lithium carbonate prices have more than doubled, climbing from a low of around 75,000 yuan per ton in 2025 to breach 180,000 yuan in the first quarter of 2026. Data from Shanghai Metals Network shows the average price for the quarter stabilized between 150,000 and 160,000 yuan per ton, a sharp increase from a year earlier. Estimates suggest the lithium price hike alone added roughly 3,000 to 5,000 yuan to the battery cost of a single electric vehicle. Prices for commodities like copper and aluminum also remain near historical highs, with six key non-ferrous metals posting annual gains ranging from 11.8% to 30.4%.Against this backdrop, the non-ferrous metals industry saw profits surge in the first quarter of 2026, while high volatility in lithium prices unlocked profit potential for lithium miners.Data from the National Bureau of Statistics reveals that profits for industrial enterprises above a designated size jumped 15.5% year-on-year to top 1.69 trillion yuan. Within that, equipment manufacturing profits rose 21%, and high-tech manufacturing surged 47.4%. The raw materials sector saw a 77.9% increase, with non-ferrous metal industry profits soaring 116.7%.Image Source: Huaban.comIn the upstream sector, lithium battery companies posted particularly standout results. As of April 27, 2026, 29 listed firms in the lithium battery chain had released quarterly reports; 15 reported year-on-year net profit growth, and three swung to profitability. CATL logged a net profit of 20.74 billion yuan, up 48.52%, outpacing the full-year 2025 earnings of every major Chinese automaker except BYD in just a single quarter.Upstream lithium miners saw their profits multiply several times over. By contrast, automakers that do not manufacture batteries themselves face even tighter margins, squeezed by falling export prices and rising domestic battery costs.Persistently high raw material costs are transmitting pressure from the cost side deep into operations for the auto industry. Power batteries—the most expensive component in an EV—have risen in tandem with lithium carbonate, driving up manufacturing costs. Yet fierce price competition prevents automakers from passing these costs entirely to consumers, significantly compressing gross margins.On a per-vehicle basis, average costs climbed 6.3% to 299,000 yuan in the first quarter, outpacing the 5.4% growth in revenue per vehicle. As a result, gross profit per vehicle slumped 13.2% to just 11,000 yuan.Automakers lacking their own battery capacity find themselves at a bargaining disadvantage, while those with vertical integration enjoy more buffer room. Furthermore, the structural imbalance—surging upstream profits versus plunging downstream gains—means that if resource prices stay high, some smaller players will face sustained losses, potentially accelerating industry consolidation.Policy Guidance and Market Regulation: External Variables to Ease Profit PressureAs profit margins continue to slide, regulators are stepping in.In the latter half of the first quarter, the Ministry of Industry and Information Technology, the National Development and Reform Commission, and the State Administration for Market Regulation jointly held a symposium with new energy vehicle companies. They pledged to strengthen price monitoring and cost investigations, cracking down on malicious competition such as selling below cost.Image Source: State Administration for Market RegulationThe market regulator previously released the "Compliance Guidelines for Price Behavior in the Auto Industry," drawing red lines around price-fixing and predatory dumping. Further measures to enforce the Anti-Unfair Competition Law have also taken effect. As the state continues its push to curb cutthroat competition, upstream industry profits are expected to improve.Looking at the internal logic of profit distribution along the supply chain, the lack of in-house battery production is a structural reason automakers are losing the cost battle. Cui Dongshu put it bluntly: "The problem of automakers not making batteries is severe; industry profits will continue to slide."With upstream resource prices high and battery costs rising, automakers without vertical integration face intense pressure. In the medium to long term, extending upstream to control core component capacity may be a crucial path for improving profit structures.ConclusionOverall, the profit pressure from high upstream raw material costs in the first quarter is likely to see some marginal relief in subsequent quarters as the three government departments continue to regulate market order. Moving forward, the trajectory of upstream resource prices and automakers' ability to control costs for core components like batteries will be the two key factors determining the extent of that relief.