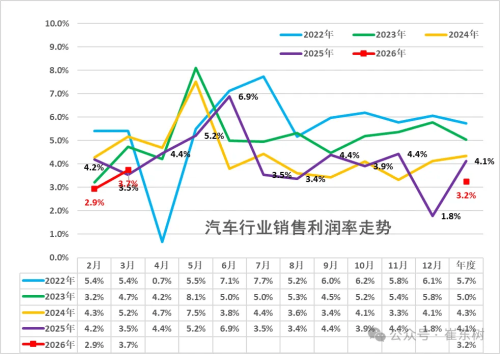

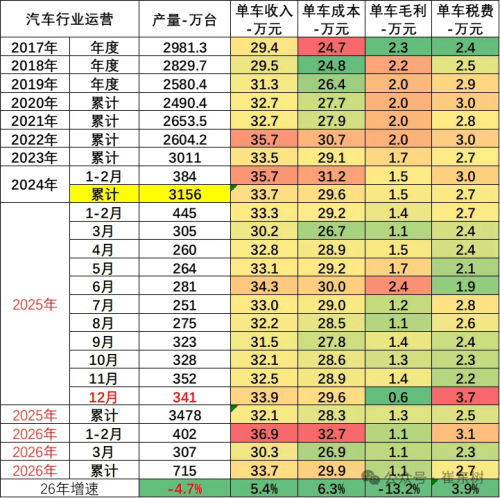

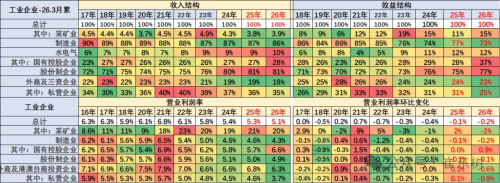

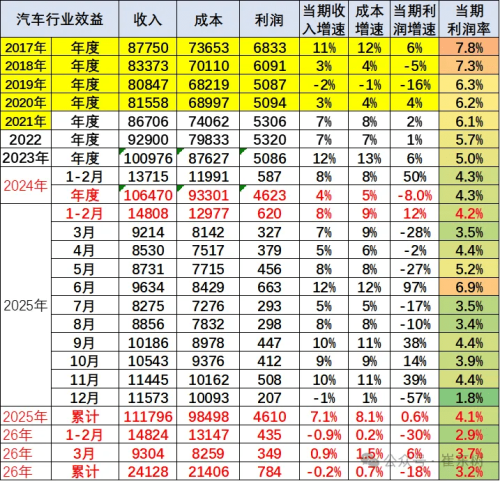

Cui Dongshu, Secretary-General of the China Passenger Car Association (CPCA), released the China automotive industry profit report for January-March. Data shows that in the first quarter, automobile production reached 7.15 million units, down 6% year-on-year; industry revenue totaled 2,412.8 billion yuan, down slightly by 0.2% year-on-year; costs stood at 2,140.6 billion yuan, up 0.7% year-on-year; while profit was only 78.4 billion yuan, plunging 18% year-on-year. More notably, the automotive industry’s sales profit margin further dropped to 3.2%, hitting a historic low. Although the single-month profit margin in March rebounded to 3.7%, outperforming the 2.9% recorded in January-February, the overall situation remains at an industry trough. Compared with the average 6% profit margin of downstream industrial enterprises, the profitability of the automotive industry is significantly weaker, and even far below the 9% profit margin level seen in 2014. Trend of sales profit margin in the automotive industry From the perspective of per-vehicle economic indicators, the automotive industry’s per-vehicle revenue in the first quarter was 337,000 yuan, up 5.4% year-on-year; per-vehicle cost was 299,000 yuan, up 6.3% year-on-year; per-vehicle taxes and fees were 27K RMB(~$ 3954), up 3.9%; while per-vehicle gross profit was only 11K RMB(~$ 1610), down 13.2% year-on-year. These figures reveal a stark reality: the cost increase (6.3%) significantly outpaced the revenue growth (5.4%), and coupled with rising taxes and fees, the per-vehicle profit margin has been continuously squeezed. Operating cost data of the automotive industry Specifically, in the first quarter of 2026, profit differentiation across industrial sectors was extremely pronounced. Mining industry profits grew 16% year-on-year, with the profit margin maintained at a high of 19.9%. Among them, the non-ferrous metal mining and dressing industry saw a profit margin as high as 39.1%, while the oil and natural gas extraction industry reached 32.9%. The surge in upstream raw material prices has directly created massive cost shocks for downstream manufacturing industries. In the first quarter, overall downstream industrial profits grew by 15%, yet automotive manufacturing profits declined by 18%, making it an “outlier” among downstream industries. In contrast, other downstream sectors such as tobacco, alcohol, and pharmaceuticals maintained profit margins at high levels of 12%-17%, while the computer, communication, and electronic equipment industry saw an abnormal profit growth of 125%. The automotive industry’s 3.2% profit margin not only falls below the downstream average of 6%, but also lags significantly behind comparable consumer goods industries. Changes in the revenue and profit structure of industrial enterprises Looking at the automotive industry’s production structure in the first quarter. The overall automobile market showed a contraction trend, with total production in the first quarter at 7.15 million units, down 6% year-on-year. Among them, sedan production was 2.27 million units, plummeting 22% year-on-year; SUVs bucked the trend with growth, reaching 3.4 million units, up 6% year-on-year; new energy vehicle (NEV) penetration remained stable, with production at 3.02 million units, down slightly by 6% year-on-year; in contrast, fuel-powered vehicles continued to shrink, with production at 4.13 million units, down 5% year-on-year. Worth mentioning is that NEV penetration maintained a high level of 42%, but the growth rate has clearly slowed (compared to 25% growth in the same period last year), indicating that the new energy vehicle market has shifted from high-speed growth to a stage of stock competition. Profit structure of the automotive industry