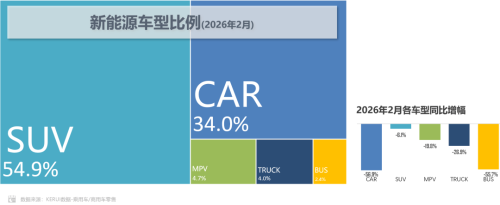

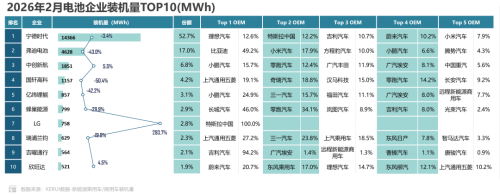

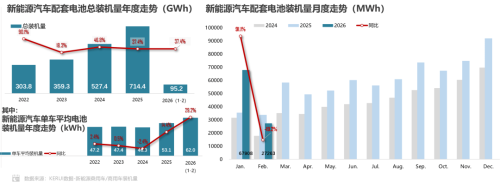

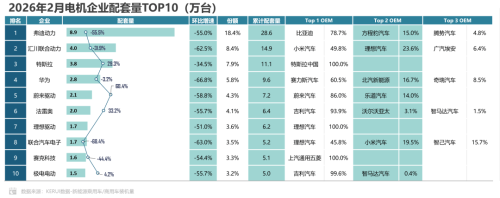

Recently, the China Passenger Car Association (CPCA) released its February New Energy Vehicle Three-Electric System Insight Report. The report noted that overall production and sales fluctuated under the combined influence of the halved purchase tax policy and the Spring Festival holiday. From January to February, China’s new energy vehicle production reached 1.604 million units, a year-on-year decrease of 13.7%, with a cumulative penetration rate of 39.9%. In terms of market structure, all vehicle types posted year-on-year declines. Among them, sedans saw the largest drop of 56.9% and currently hold a 34% market share, while SUVs fell by 6.1% year-on-year with a 54.9% market share. New energy vehicle ratio In February, the power battery installation volume for new energy vehicles reached 27.3 GWh, down 19.2% year-on-year. Data showed that the top 10 battery enterprises in terms of installation volume accounted for a combined 62.4% of the market share. CATL ranked first with a market share of over 50%, and its installation volume was 3.1 times that of BYD, which came in second. CATL supplies mainstream automakers including Li Auto, Tesla, Geely, NIO and Xiaomi. BYD ranked second with a 17% market share. Nearly half (49.2%) of its total battery installation volume went to its own brand, and among external customers, Xiaomi ranked first with a 17.9% share, far higher than BYD’s own brands such as Denza and Fangchengbao. This battery installation performance is also reflected in the market performance of Xiaomi Auto. Official data showed that Xiaomi’s cumulative sales exceeded 59,000 units from January to February, up 47.5% year-on-year. Top 10 battery manufacturers by installed capacity in February 2026 It is worth adding that the all-new SU7 was officially launched on March 19. At the first delivery ceremony, CEO Lei Jun revealed that the number of new car reservations had exceeded 30,000. It is expected that Xiaomi’s share in BYD’s battery supply system will rise further as the new model hits the market. Along with the continuous growth in new energy vehicle sales, the power battery market saw a cumulative year-on-year increase of 37.4% from January to February. During the same period, the average battery capacity per new energy vehicle was 62.0 kWh, an increase of 29.2% year-on-year. Xiaomi, BYD and Tesla became the major contributors to power battery installation volume. Annual trend of total battery installed capacity for new energy vehicles The drive motor and electronic control sectors showed a clear star-model effect. In the drive motor market, the top 10 enterprises held a combined 62.4% share in February, with most experiencing a month-on-month decline. The top five supporting models of BYD accounted for 45.2%, among which the Fangchengbao Tie 7 took up 12.5%, becoming a new growth driver. Inovance Technology’s core supporting model is the Xiaomi YU7, with this single model accounting for as high as 49.6% of its matching volume. Tesla uses self-produced motors exclusively, with the Model Y making up 47.1% of its total motor matching volume. Huawei mainly supplies the AITO series, and the AITO M7 accounted for 32.2% of its motor matching volume. In February 2026, the TOP 10 motor enterprises by support volume. In the electronic control market, the top 10 suppliers held a combined 61.5% share in February. Fudi Power’s matching volume dropped significantly by 61.2% year-on-year. Among Huawei’s supporting automakers, Seres accounted for 63.8%. In terms of specific models, the Xiaomi YU7 made up 48.9% of Inovance Technology’s electronic control matching volume, the AITO M7 35.0% of Huawei’s electronic control matching volume, and the Model Y 47.1% of Tesla’s electronic control matching volume. The report concluded that solid-state batteries are becoming the core direction of next-generation battery technology. Currently, solid-state battery technologies are divided into four categories according to electrolyte types: sulfide, oxide, polymer and composite electrolytes. Their core advantages include effectively solving the problem of thermal runaway in terms of safety, and an expected energy density of over 500 Wh/kg, which will greatly increase the cruising range of vehicles.