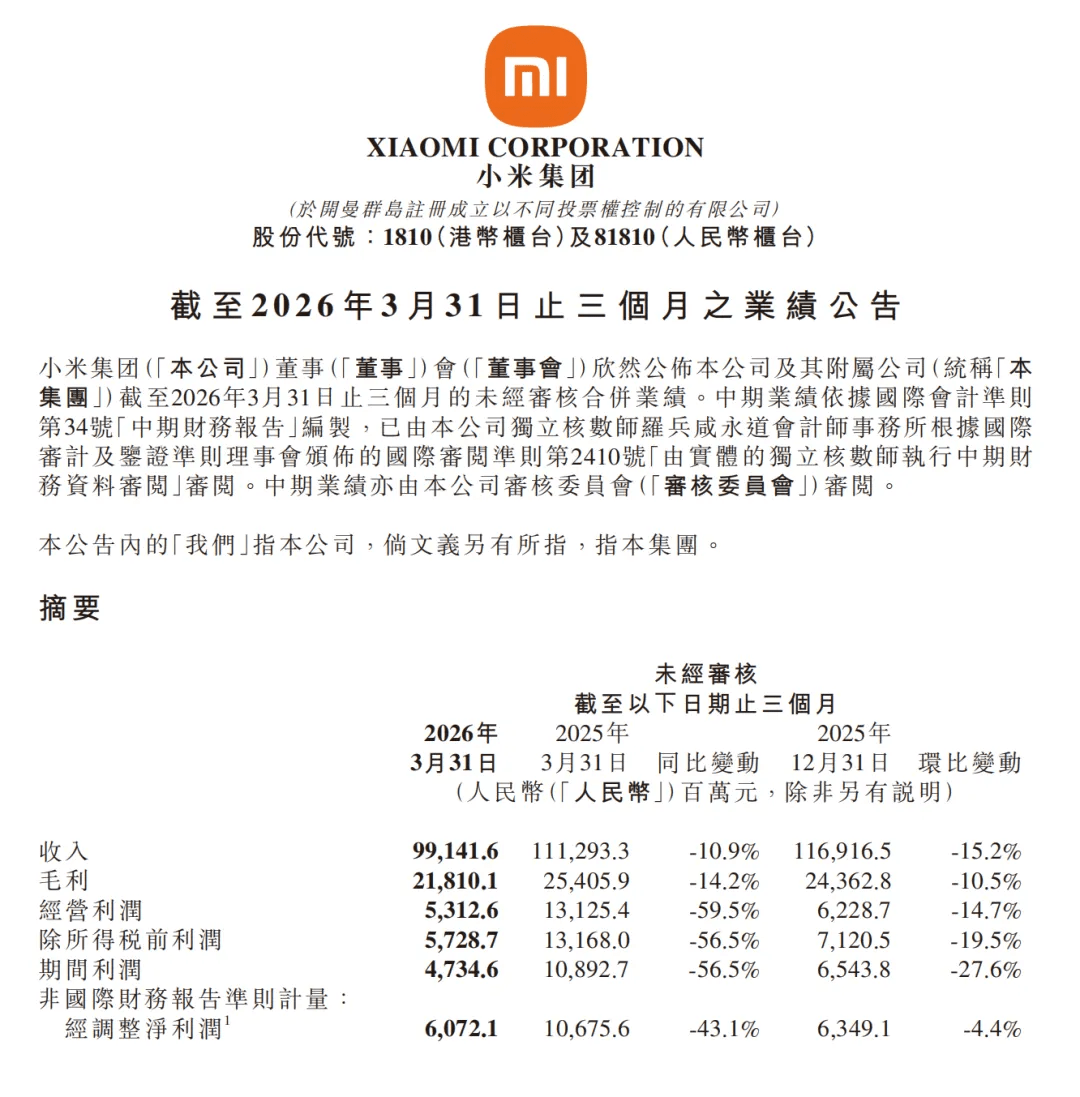

On May 26, Xiaomi released a quarterly automotive earnings report that is difficult to summarize in just a few sentences. First, the numbers: Q1 deliveries reached 80,856 units, up 6.6% year-on-year but down sharply from Q4’s 145,000 units to just above 80,000 units sequentially. Automotive revenue fell to RMB 19 billion ($2.8 billion), while ASP dropped to RMB 235,100 ($34,600). Viewed in isolation, the report suggests slowing growth and mounting pricing pressure. Xiaomi EV’s financial data in Q1 But the figures need to be understood in context. Q1 coincided with a highly unusual product transition period. The first-generation SU7 lineup was discontinued at the beginning of the quarter, while the new-generation SU7 was only unveiled in March and began scaling deliveries in April. Throughout the entire first quarter, Xiaomi EV’s delivery backbone was effectively limited to the YU7 alone. Under those conditions, achieving quarterly sales of 80,000 units was not necessarily weak. As for the new-generation SU7, Xiaomi said locked orders surpassed 80,000 units during the launch phase, while deliveries exceeded 26,000 units within one month of launch — roughly triple the ramp-up pace of the first-generation SU7. Looking ahead to Q2, vehicle sales are highly likely to post a meaningful sequential rebound, suggesting Xiaomi EV’s core business fundamentals remain stable. Gross margin became another focal point of debate. The earnings report showed a segment gross margin of 20.1%, down 3.1 percentage points year-on-year. Xiaomi attributed the decline to a lower mix of SU7 Ultra deliveries, purchase-tax subsidies, and rising core component costs. In absolute terms, however, a gross margin above 20% still exceeds most Chinese EV startups. NIO Inc., for example, recently reported a vehicle gross margin of 18.8%. In other words, a “20.1% gross margin” is still a relatively strong figure. The controversy lies in the fact that the number combines automotive, AI and other businesses together, while Xiaomi did not separately disclose vehicle-only gross margin. A decline in sales of higher-margin products such as the SU7 Ultra inevitably weighs on profitability across the division. At the same time, the upcoming new-generation Xiaomi SU7 is unlikely to be a high-margin product either. Given rising costs, margin pressure could even exceed that of the YU7. Xiaomi President Lu Weibing has already confirmed that the YU7 standard version will deliver lower margins than previous variants. As for the YU7 GT, while margins may improve somewhat, demand remains uncertain. Xiaomi YU7 GT During the earnings call, CFO Alain Lam said that in Q2, rising sales volumes and higher ASP could improve cost allocation efficiency, “which may have some impact on gross margin.” The implication was clearly positive. But whether that translates into actual financial improvement will depend on future data. At the same time, Lu Weibing previewed a new large vehicle based on an entirely new platform set to debut in the second half of the year, while previously denying rumors that it would be named “YU9.” Market speculation suggests the vehicle could launch under a new “Xuntian” product series and target the large SUV market with an extended-range powertrain. Returning to the earnings report, the clearest signal came from changes in capital expenditure. Xiaomi SU7 Automotive-related CapEx plunged from RMB 3.88 billion ($570 million) in Q4 to RMB 1.49 billion ($220 million) in Q1, a decline of 61.5%. One of the market’s biggest concerns about Xiaomi’s EV business had been the fear of endless cash burn. At minimum, this sharp decline indicates that the peak phase of production capacity investment has likely passed following completion of the company’s Phase I and Phase II factories. Depreciation pressure has begun stabilizing, cash consumption has slowed, and the automotive division’s operating loss narrowed to RMB 3.1 billion ($460 million) from Q4. But the risks remain real. Operating expenses for the automotive segment still rose 45.8% year-on-year, with both R&D and sales spending continuing to expand. Meanwhile, ASP declined 5.9% quarter-on-quarter, as product mix and subsidy pressure simultaneously squeezed profit margins. More importantly, the health of the broader Xiaomi Group deserves attention. Smartphone shipments fell 19.2% year-on-year, IoT revenue plunged 23.7%, and operating cash flow turned negative. Automotive revenue now accounts for roughly 20% of Xiaomi Group’s total revenue, meaning the EV business is increasingly expected to independently support the company’s growth narrative — even though it remains far from profitability. That also means Xiaomi Group may become increasingly dependent on its EV business, while the division’s operational performance will have a growing impact on the broader company. Xiaomi EV’s market momentum remains strong, but margins are shrinking and the business is still operating at a loss — arguably the most controversial aspect of the current results. Q2 will therefore become an important stress test, as deliveries of the new SU7 ramp up and YU7 GT deliveries begin. If losses fail to narrow meaningfully despite a sharp increase in deliveries, investor confidence in Xiaomi EV’s profitability model could weaken. At the same time, YU7 sales have started to cool after peaking last year. Responding to questions from reporters, Lu Weibing attributed the decline largely to delivery lead times that at one point stretched to 10 months, resulting in customer attrition. He also noted that feedback for the YU7 standard version has been positive since vehicles began arriving at dealerships. As production capacity constraints gradually ease, the YU7 may be able to maintain its current delivery performance more steadily. Looking at the full year, Xiaomi EV is still maintaining its 500,000-unit sales target. But after intentionally transitioning its product lineup in Q1 and delivering only 80,000 vehicles, the pressure on the remaining three quarters has become extremely high. As for the question of when Xiaomi EV can turn profitable, CFO Alain Lam did not provide a specific answer. However, based on the formula he outlined — “operating profit/loss = deliveries × gross margin – AI investment” — a significant increase in delivery volume clearly remains a key factor. Xiaomi is not without a “second option” to drive incremental growth. During the earnings call, reporters also asked about overseas expansion plans, which could potentially become an entirely new growth engine for Xiaomi EV. But Lu Weibing’s response was notably measured. He emphasized that Xiaomi EV still intends to “follow the original plan,” with a strategy focused on “developed markets before developing markets,” “premium models before mass-market models,” and “right-hand-drive models before left-hand-drive models.” The issue lies in the timeline. Xiaomi Group currently plans to begin overseas expansion only in the third or fourth quarter of 2027, meaning the initiative will have virtually no impact on sales in the near term. In the upcoming second quarter, the YU7, YU7 GT and SU7 will shoulder essentially all delivery pressure. Whether Xiaomi EV’s financial metrics can rebound as hoped remains an open question. That answer will likely have to wait until the next earnings report.