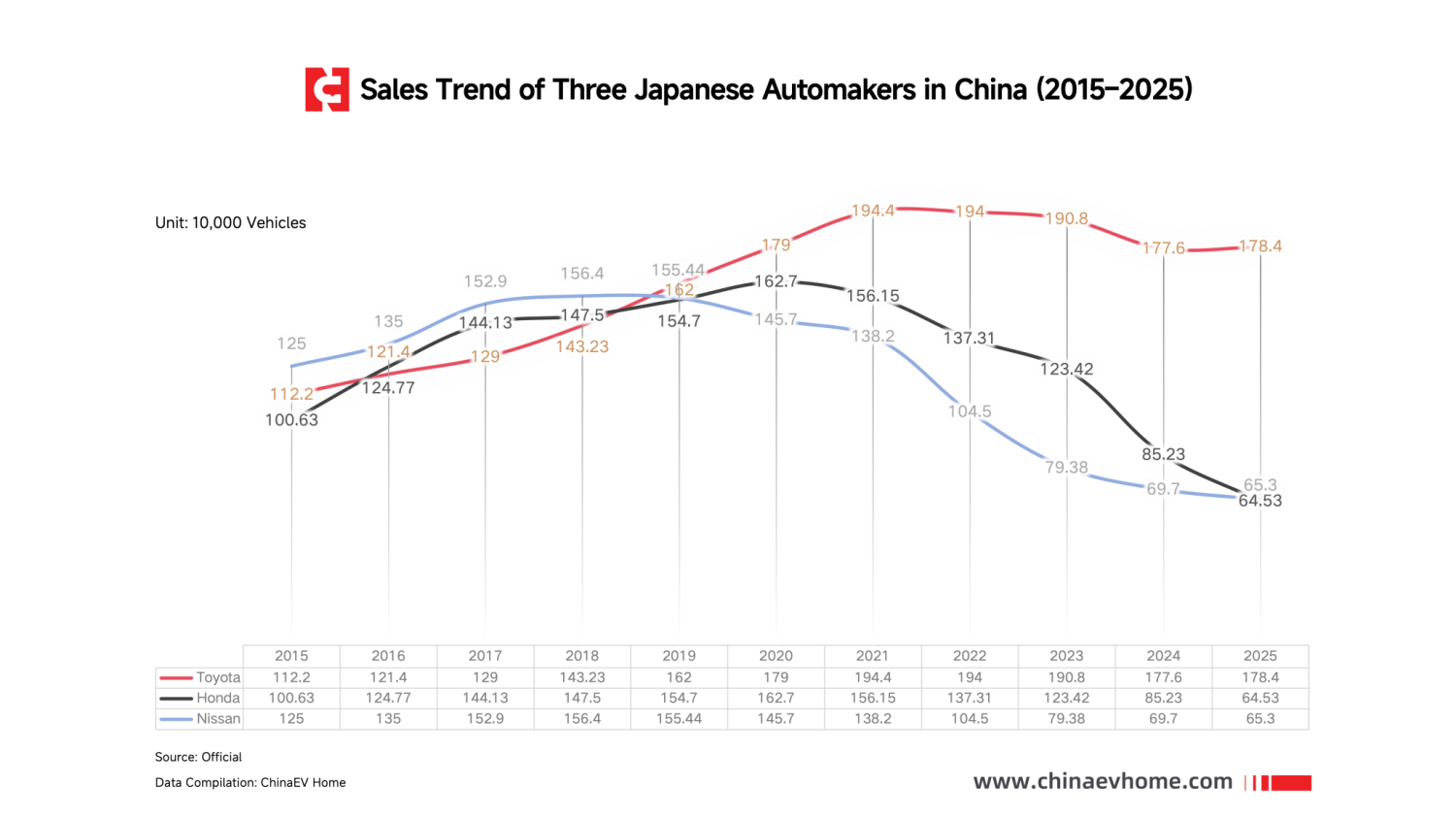

The top three Japanese automakers sold approximately 3.08 million vehicles in China in 2025, accounting for less than 9% of the market share. According to data released by the China Association of Automobile Manufacturers, China’s total automobile sales reached 34.4 million units in 2025. Considering that the combined sales of the three major Japanese brands in China were approximately 3.08 million units, their market share has fallen to less than 9%. Against the backdrop of new energy vehicle penetration approaching 60% and strong competition from domestic brands, Japanese brands are facing vastly different realities in the Chinese market. Recently, Toyota Motor officially announced that its total sales in the Chinese market in 2025 exceeded 1.78 million vehicles, showing a slight increase from 1.776 million vehicles in 2024. This makes Toyota the only Japanese brand to achieve positive growth in the Chinese market in 2025. In contrast, Nissan China sold 653,000 vehicles for the full year, a year-on-year decline of 6.26%. This marks the seventh consecutive year of sales decline for Nissan in the Chinese market. Compared to its sales peak in 2018, Nissan’s sales have nearly halved, dropping by close to 60%. Meanwhile, Honda China’s sales fell to 645,300 vehicles, a decrease of 24.28% year-on-year, representing the fifth consecutive year of decline. Its annual sales have shrunk by nearly one million vehicles compared to the 1.627 million units sold in 2020. HONDA S7 Specifically, Toyota’s counter-trend growth benefits from its more proactive localization strategy. In terms of organizational structure, Toyota introduced the RCE (Regional-Chief Engineer) system, with its core being “full-process localization.” This system hands over the development decision-making power for future China-specific models to its Chinese team. Reflecting this in specific models, the bZ3X, launched in March 2025, has seen steady sales growth, surpassing 10,000 units per month for two consecutive months in October and November 2025. In addition to the already launched bZ3X and bZ5, Toyota also plans to introduce the bZ7 as its all-electric flagship model. This vehicle will also be Toyota’s first D-segment sedan equipped with the HarmonyOS cockpit, representing the “Phase 2.0” of Toyota’s intelligent and electrification transformation. Regarding product and technology roadmap choices, Toyota’s CEO believes pure electric vehicles are not the company’s only option. Instead, Toyota has adopted a “multi-pathway” strategy centered on hybrids and plug-in hybrids, without placing all its bets on pure electric vehicles. According to its plan, Toyota aims to increase the share of HEVs to 50% by 2027. It is also accelerating its electrification transformation, planning to launch more than 5 exclusive pure electric models between 2026 and 2027, and increasing investment in localized battery production in China to reduce costs and improve efficiency. TOYOTA bZ7 Despite increasing challenges, Nissan Motor achieved new breakthroughs in the Chinese market in 2025. For example, Dongfeng Nissan successively launched the N7 and N6 NEVs in 2025, attempting to address market competition through a dual-line layout of “plug-in hybrid + pure electric.” Among them, the Nissan N7 launched in April has achieved cumulative sales of 45,000 units to date. The N6 model officially launched on December 1st also completed nearly 7,000 units in sales in its first month, a performance worthy of recognition. Data from the China Passenger Car Association shows that with the strong rise of domestic brands leveraging their advantages in new energy and intelligence, the overall market share of mainstream joint-venture brands has shrunk to 20.2%. Against this backdrop, whether the new models launched by Japanese brands in the coming years can compete with local brands like BYD and XPeng will be key to determining if Japanese brands can achieve a collective breakthrough.