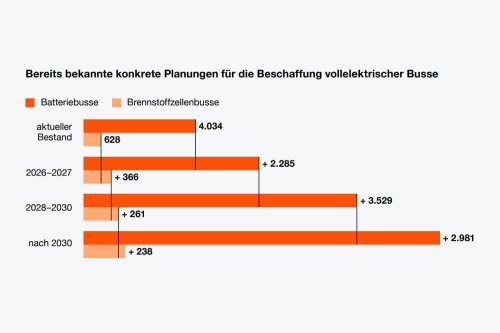

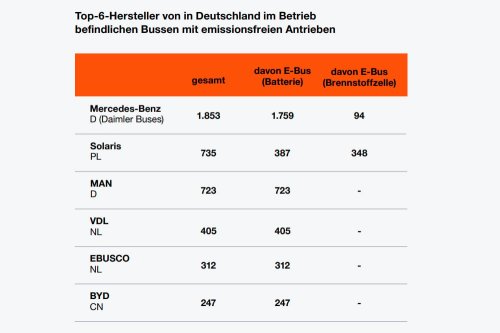

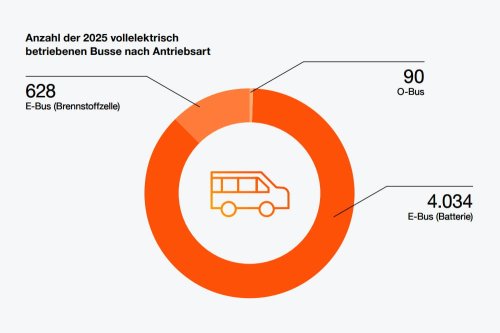

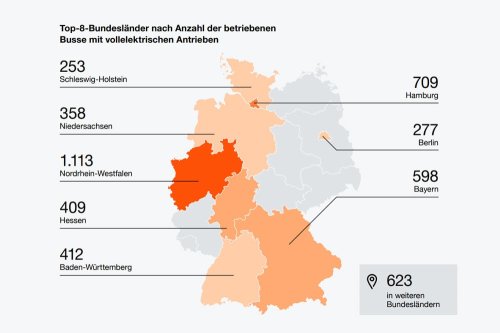

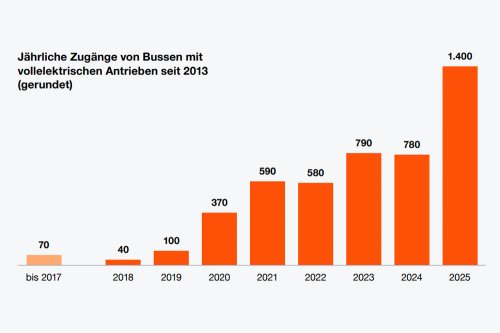

The number of new electric buses in Germany has surged sharply, as highlighted by the latest annual statistics from the German Motor Transport Authority. Depending on the methodology, the authority reports 1,458 newly registered units, while PwC counts 1,397. We explain the discrepancy below.What is clear is that registrations have roughly doubled compared to 2024. PwC’s E-Bus Radar also provides detailed insights into the distribution of battery-electric and fuel cell buses across Germany’s regions and cities, along with data on brands, costs and planned procurements.The subtitle of the eighth PwC E-Bus Radar reads: “The e-bus is gaining ground – despite challenging framework conditions.” In the seventh Radar, published a year ago, the consultancy warned: “The e-bus market at a crossroads?” In the sixth E-Bus Radar three years ago, it proclaimed: “The decade of the e-bus is picking up speed!” A lot has changed since then.Before diving into the details, a brief definition: the current analysis considers buses with more than eight passenger seats (vehicle class M3), fully electric drivetrains (BEV and FCEV), and external energy supply, which are classified as ‘clean’ or ‘zero-emission’ under the EU’s ‘Clean Vehicles Directive.’In other words, it focuses solely on electric city buses (M3, Class I). Additionally, only ‘actual operational use in public transport, not merely vehicle registration’ has been recorded. This definition is narrower than that of the KBA, which explains the aforementioned difference in recorded new registrations. PwC’s data cutoff was 31 December 2025.More than 4,000 battery-electric buses in serviceWith that in mind, let’s examine the findings: according to PwC, exactly 1,397 electric city buses were added in 2025 under the above definition. That represents a 79% increase compared to 2024 and 2023 (780 and 785 units, respectively) and marks the first time the figure has exceeded 1,000.Including these new registrations, there were 4,752 zero-emission buses in operation in Germany at the turn of the year. Of these, 4,034 were predominantly battery-electric buses, 13% were fuel cell buses (628 units), and just under 2% were trolleybuses (90 units). PwC had already included these 90 trolleybuses in last year’s statistics, and no additional trolleybuses have been added in the past twelve months. Image: PwC Image: PwC Image: PwC Image: PwC Image: PwCHowever, there has been significant movement in the other two drivetrain categories: the number of battery-electric buses increased from 2,946 to 4,034 units—a 37% rise. Fuel cell buses jumped from 339 to 628 units, an 85% increase. This makes FCEVs the fastest-growing zero-emission drivetrain in percentage terms.“A large proportion of the newly commissioned vehicles result from investment decisions made one to two years ago,” the analysts note.At the same time, a strategic shift is observable at some locations: “Planned hydrogen projects are being reviewed, adjusted, or realigned in favour of battery-electric solutions. The economic viability of fuel cell buses remains highly dependent on local conditions—particularly the guaranteed availability of sufficient hydrogen volumes at competitive prices, as well as long-term contractually secured supply structures or economically viable on-site production.”“Electrification is gaining noticeable momentum and is no longer an exception made by individual pioneers,” the study’s authors state. “Transport companies are driving the transformation with a high willingness to invest—with battery-electric technology as the clearly dominant solution, but also a growing number of fuel cell buses.”North Rhine-Westphalia, Hamburg, and Bavaria remain in the leadThe federal state ranking in the PwC report shows that nearly half of all electric buses in Germany operate in the federal states of North Rhine-Westphalia, Hamburg, and Bavaria—just as they did a year ago. North Rhine-Westphalia has now surpassed the 1,000 mark for the first time. In total, eight federal states each have more than 200 electric buses.North Rhine-Westphalia leads with 1,113 electric buses, having added a substantial 415 electric buses over the past twelve months. It is followed by Hamburg (709 vehicles), Bavaria (598), Baden-Württemberg (412), Hesse (409), Lower Saxony (358), Schleswig-Holstein (253), and Berlin (277).The remaining federal states collectively operate 623 electric buses. According to the PwC data, a clear east-west divide persists: of the six states in eastern Germany, only Berlin has more than 200 electric buses. This trend was already evident in previous e-Bus Radars. Nevertheless, more electric buses were integrated in the past year, even beyond the top eight federal states: the 623 electrically powered vehicles in the ‘remaining’ states represent a significant jump from the 340 units in 2024.At city level, Hamburg leads with 706 battery-electric buses, followed by Berlin (277), Cologne (129), Nuremberg (123) and Wiesbaden (121). Cologne also dominates hydrogen deployment with 127 fuel cell buses, ahead of Rostock (71) and Wuppertal (52). Of Germany’s 90 trolleybuses, 66 operate in Solingen.A clear trend identified by PwC is that zero-emission buses are increasingly being used in everyday operations in smaller cities and rural regions: “In 2025, zero-emission buses are in service in 222 cities and regions—up from 180 in 2024 and 90 in 2020. Within just a few years, their spatial distribution across Germany has expanded significantly.”90% of all electric buses come from six manufacturersThe PwC study also allows for filtering by manufacturer. According to the data, around 90% of the electric buses currently in operation in Germany come from six manufacturers: Daimler Buses (1,853 vehicles), Solaris (735), MAN (723), VDL (405), Ebusco (312), and BYD (247). The ranking has remained consistent compared to 2024, though sales for all manufacturers have exceeded last year’s figures.What about pricing? A 12-metre solo bus with a battery-electric drivetrain still costs significantly more than a conventional diesel bus, according to PwC. The discrepancy is similar for articulated buses. Specifically, the analysts cite €580,000 and €780,000 for the procurement of battery-electric solo and articulated buses, respectively, compared to €310,000 and €410,000 for comparable diesel models.What stands out is that the price tag for battery-electric buses has remained unchanged compared to last year’s E-Bus Radar, while those for diesel buses have increased by €50,000 each. That means the price gap is narrowing—not because battery-electric buses are becoming more affordable, but because diesel vehicles are becoming more expensive.However, the authors assume that bus manufacturers ‘will achieve economies of scale as zero-emission buses become more widespread and production volumes increase.’The key question is whether these savings will be passed on to consumers in the form of lower prices.One thing remains clear: the price premium for electric buses is still substantial. As the report states: “Operating electric buses requires significant investment in charging infrastructure, grid connections, and depot upgrades. In many cases, additional space is also needed for e-bus infrastructure. This poses an additional economic challenge, particularly in urban areas.”The authors conclude that funding programmes remain crucial for the transformation of public transport. In this context, the follow-up funding announced by the federal government for spring 2026 is timely.According to the E-Bus Radar, the currently known plans of fleet operators aim to procure around 6,400 additional zero-emission buses by 2030. Based on the current fleet, this could increase the number of electric buses to over 11,000.“Overall, the currently known procurement plans across all drivetrain types amount to around 9,660 additional vehicles. The federal government’s target—half of all city buses in Germany to run electrically by 2030—is thus achievable,” the study’s authors conclude.pwc.de, pwc.de (PDF), pwc.de (press release; all links in German)