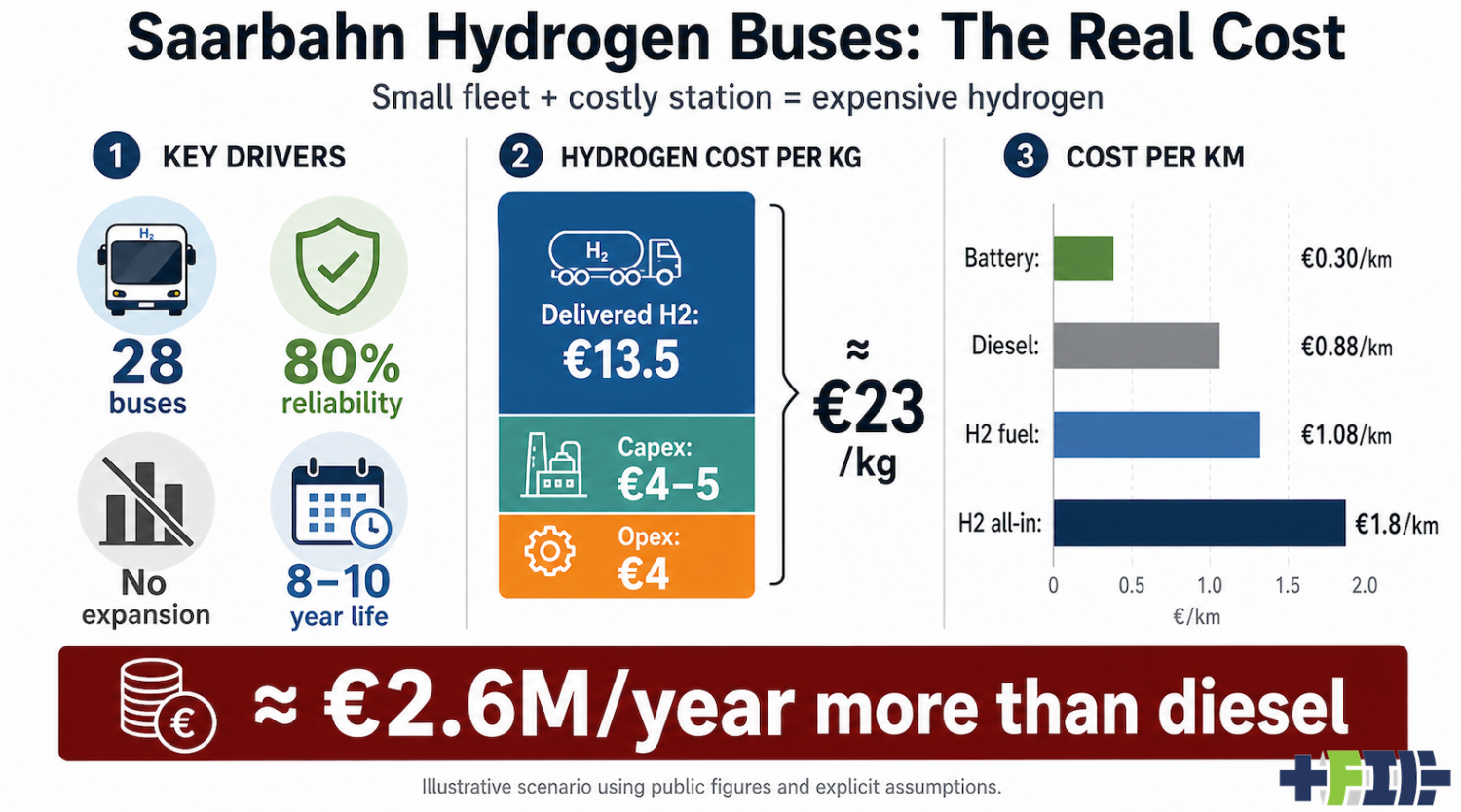

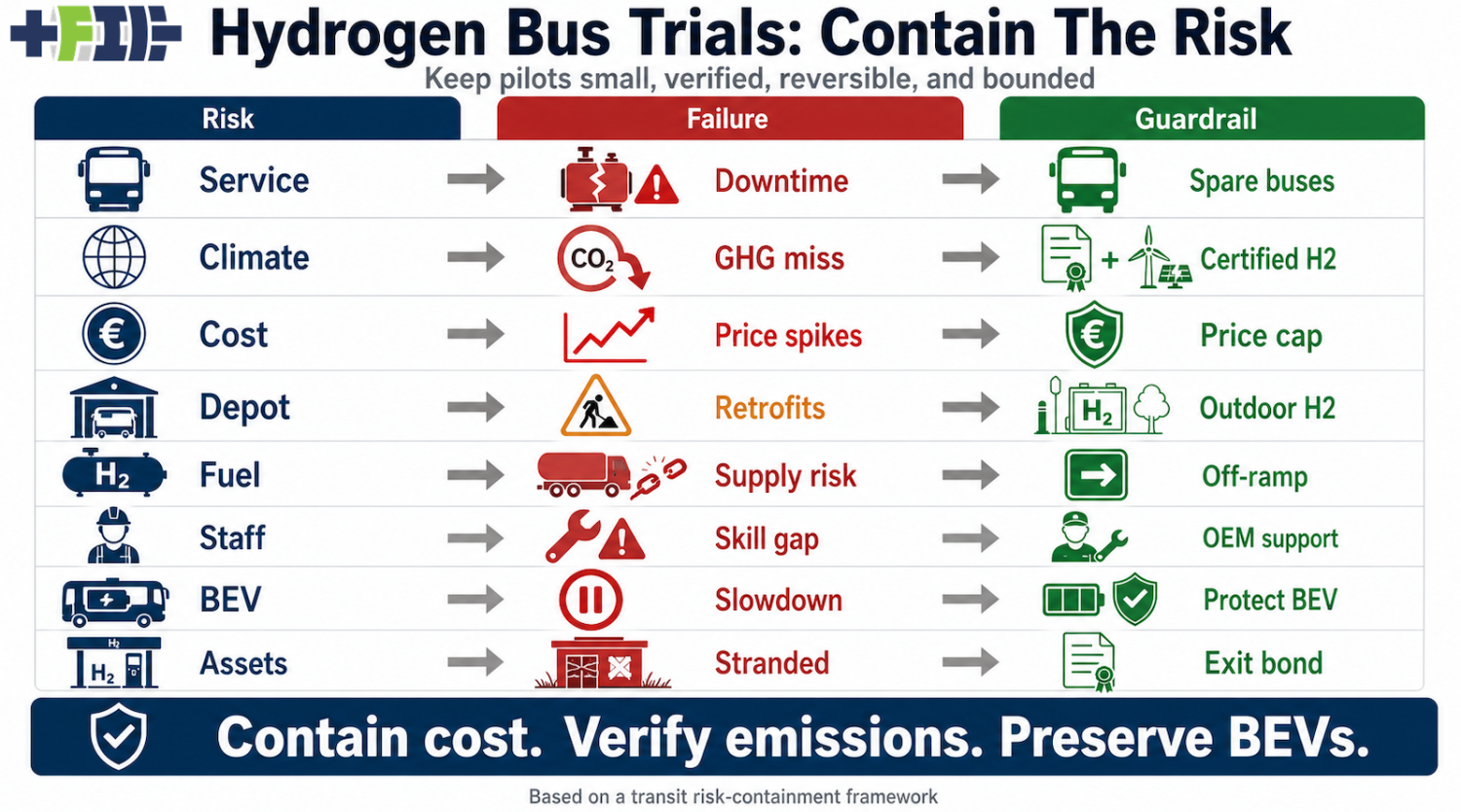

Saarbahn’s newly opened hydrogen refueling station in Saarbrücken is the moment its hydrogen bus program stops being a procurement story and becomes an operating system. The 28 Wrightbus Kite Hydroliner fuel-cell buses now have a depot station, three 350 bar dispensers, storage capacity, delivery logistics, trained staff, safety systems, and daily operating expectations. Hydrogen transit is often discussed as if the bus is the decision. It is not. The station is where the system cost becomes visible. That is why Saarbahn is a useful case study. Saarbrücken is not an obviously poor setting for hydrogen buses. The city has hilly terrain. Some bus duties reportedly exceed 300 km per day. Layovers can be short. A bus that can run 350 km to 400 km between fills and refuel in about ten minutes has real operational appeal. Add federal support, a municipal depot, and a future plan for green hydrogen from Freisen, and the project looks like one of the better versions of the hydrogen bus argument. But good framing is not the same thing as good economics. Once a €7.6 million refueling station is built, the important question is whether enough hydrogen will move through it, at high enough reliability, for enough years, to make the refueling infrastructure cost per kg reasonable. That is the denominator problem. Saarbahn’s public project numbers are clear enough to test. The agency has about 138 buses in total, so the 28 hydrogen buses represent roughly one-fifth of the bus fleet. The Wrightbus buses reportedly carry 36.5 kg of hydrogen in roof tanks. Saarbahn’s new station cost about €7.6 million, with about €3.06 million in public support for the station or infrastructure. The wider bus and infrastructure program received about €11.1 million to €11.17 million in federal support through Germany’s alternative bus drivetrain funding program, according to reporting from NOW GmbH, Electrive, and Urban Transport Magazine. A ten-year horizon and no expansion beyond 28 buses is a defensible and likely downside case, not an invented worst case. Hydrogen stations are not passive civil assets. Compressors, storage systems, dispensers, chillers, valves, sensors, controls, and safety systems all face refurbishment and life-extension decisions. Aberdeen is the cautionary reference class: after hydrogen supply and refueling problems, its 25 hydrogen double-deckers were parked, and the city moved toward disposal rather than another round of spending on the pathway. Saarbahn has also not publicly committed to full hydrogen conversion. It has described hydrogen as an initial pathway while keeping future procurement technology-open. If the first tranche shows the reliability, fuel-price, maintenance, or staffing problems seen elsewhere—likely—, stopping at 28 buses and reassessing before major station reinvestment will be the rational decision, not the pessimistic one. For now, the hydrogen is delivered by truck trailers. As best as I can tell, it is at least somewhat green hydrogen. The longer-term plan is to produce green hydrogen in Freisen from 2028, using an electrolyzer associated with a local wind farm. The Saarland environment ministry is supporting that electrolyzer project with about €2.7 million. It will not change the economics of the station that has already been built, just provide more subsidies to try to make hydrogen less expensive for transit agencies. The delivered hydrogen price is the first uncertainty. A low number can be inferred if a public procurement framework ceiling is divided by an assumed annual volume, but that is not the same thing as a disclosed €/kg contract price. A back-calculated figure around €7.3/kg does not line up well with ordinary trailer-delivered green hydrogen cost reality. At that price, the fuel is likely fossil-based, subsidized, quota-supported, loss-leading, or not representative of full annual fleet consumption. A more realistic central case is €13.50/kg for delivered hydrogen, with €12/kg to €15/kg as a useful sensitivity range. At Saarbahn’s stated or assumed consumption of about 8 kg per 100 km, €13.50/kg hydrogen becomes €108 per 100 km, or €1.08/km, before station costs are counted. By comparison, a diesel bus using 40 L per 100 km at €2.19/L costs about €87.60 per 100 km, or €0.88/km. A battery-electric bus using 1.2 kWh/km at €0.25/kWh costs about €0.30/km. So even before the station appears, hydrogen is not cheap. In this central case, delivered hydrogen fuel alone is about 23% more expensive per km than diesel and about 3.6 times the battery-electric energy cost. But the refueling station is the point of the case study, and the station makes the gap much larger. The station arithmetic is straightforward. Assume 28 buses, 350 km per day, 280 service days per year, and 8 kg of hydrogen per 100 km. That produces planned hydrogen use of 28 times 350 times 280 times 8 divided by 100, or 219,520 kg per year. Rounded, that is about 220 tons per year. If the system delivered perfect useful throughput, that would be the denominator. Hydrogen bus and refueling systems often do not perform at that level, especially in early years. Using an 80% useful system reliability assumption reduces useful throughput to about 176,000 kg per year. The station capital cost and operating cost do not fall in proportion to that lower throughput. Fewer useful kilograms means higher infrastructure cost per kg. Assume annual station operating cost at 10% of capex. For a €7.6 million station, that is €760,000 per year. Spread across 176,000 kg per year, station opex alone adds about €4.32/kg. That is not hydrogen production cost. It is not the fuel supplier’s bill. It is the cost of keeping the refueling system available, serviced, inspected, and usable. The capex burden is about the same size. If the station operates for ten years at 176,000 kg per year, total useful throughput is 1.76 million kg. The €7.6 million capex divided by 1.76 million kg gives €4.32/kg. If the station lasts eight years before a major refurbishment or shutdown decision, total useful throughput is 1.408 million kg, and the capex burden rises to about €5.40/kg. That means the refueling infrastructure adds about €8.6/kg to €9.7/kg before the fuel itself. Delivered hydrogen at €13.50/kg becomes about €22.1/kg to €23.2/kg at the bus nozzle. Rounded, Saarbahn’s real hydrogen cost under these assumptions is about €23/kg. The newly opened station does not just dispense hydrogen. It adds almost another hydrogen price to the hydrogen price. Convert that back into bus-km and the result is hard to ignore. At €22.65/kg and 8 kg per 100 km, hydrogen costs about €181 per 100 km, or €1.81/km, for delivered fuel plus refueling infrastructure. Diesel is about €0.88/km. Battery-electric energy is about €0.30/km. Hydrogen fuel-only is about €1.08/km, but hydrogen all-in with station capex and opex is about €1.8/km. For Saarbahn’s 28 buses, the annual distance assumption is 28 buses times 350 km per day times 280 days, or 2.744 million bus-km per year. Hydrogen all-in at €1.81/km costs about €4.97 million per year for energy and refueling infrastructure. Diesel at €0.88/km costs about €2.42 million per year. Battery-electric at €0.30/km costs about €823,000 per year. The hydrogen premium is about €2.55 million per year compared with diesel and about €4.14 million per year compared with battery-electric. These are not full total cost of ownership figures. They do not include vehicle purchase price, driver labour, maintenance differences, insurance, financing, depot works beyond the fuel systems, taxes, or residual value. They are energy system comparisons. That limited scope is why they matter. If the energy system alone creates a €2.6 million annual premium over diesel for 28 buses, before counting fuel-cell bus maintenance premiums, spare fleet effects, or diesel fallback during outages, the project is not sitting in the rounding-error column. Fuel is not the largest transit cost. Labour is. But that does not make the hydrogen premium small. Labour often represents around 50% to 60% of bus operating cost. Fuel may be around 10% to 15%. Maintenance and depreciation can each be in a similar range. The station-inclusive hydrogen premium over diesel is about €0.93/km. Against an €8/km bus operating cost reference, that is around 11% to 12% of total operating cost, roughly the size of an entire major cost category. The compressors, storage, trailers, dispensers, inspections, and maintenance contracts do not vanish because they sit behind the depot fence. Expansion could improve the arithmetic. The station may not have been built only for 28 buses. It has 2.4 tons of capacity and modular station technology. Public reporting has suggested Saarbahn may have contemplated a hydrogen fleet closer to 60 vehicles. If the station eventually serves 60 buses, operates at high reliability, and remains in service for 15 years, the infrastructure burden per kg falls. Hydrogen infrastructure economics look better when high fixed costs are spread across more fuel. But public evidence does not show a formal plan to convert the whole bus fleet to hydrogen. Saarbahn’s language has been cautious. It has described hydrogen as an initial pathway and has said it remains technology-open. Battery-electric buses remain part of the public discussion. Near-term hydrogen ambition appears to be a subset of the fleet, not a full 138 bus conversion. The project might grow, but the economics depend on that future arriving. The battery-electric alternative has to be treated with the same seriousness. Saarbahn’s routes may be demanding. Long daily blocks, hills, passenger loads, winter conditions, air conditioning, driver schedules, depot constraints, and layover times all affect battery-electric feasibility. A simple comparison between hydrogen buses and depot-only battery buses would not settle the question. The fair comparison is hydrogen buses plus a dedicated hydrogen station versus battery-electric buses plus the charging architecture needed for the network. That could include depot charging with larger battery packs, terminal opportunity charging, route and block optimization, depot grid upgrades, charging at interchanges, and selective in-motion charging on the hardest corridors. Saarbahn may have had a plausible case against simple depot-only battery substitution. That is not the same as proving that battery-electric transit with a proper charging strategy could not meet the service requirements. In-motion charging is relevant because it addresses the strongest hydrogen arguments: steep routes, long duties, and limited layover time. Modern in-motion charging trolleybuses use overhead wires on parts of a route and batteries off-wire. They do not require every kilometre to be wired. They recharge while moving, which reduces dependence on terminal charging and can reduce battery size. The technology has costs and constraints, but it is a known transit option, not a lab concept. Public material I have seen does not show a full comparison by Saarbahn of hydrogen against battery-electric buses with opportunity charging and selective in-motion charging. There are references to a feasibility study and to regional hydrogen planning. There are public explanations based on topography, long distances, refueling time, and range. Those are legitimate inputs. They are not, by themselves, proof that battery-electric alternatives were inferior. As with most hydrogen fleet decisions, regional assertions of a hydrogen economy and cheap hydrogen led to transit agencies settling on hydrogen with poor due diligence. This matters because hydrogen decisions often harden around assumptions that were somewhat plausible several years earlier. Battery-electric buses have improved. Charging strategies have improved. Depot energy management has improved. Operating experience has improved. Green hydrogen costs have remained stubbornly high. Higher ecosystems have not materialized, and hydrogen use cases have collapsed. A conclusion that made sense in a 2020-style range framing is weaker in a 2026 infrastructure context. Infographic of common hydrogen transit fleet failures and related derisking A prudent hydrogen procurement should also protect the agency from known hydrogen risks. Saarbahn appears to have done some things that reduce exposure. It did not convert the whole fleet at once. It has kept technology-open language. It has a depot station rather than depending on public fueling. It has contracted for hydrogen supply. It has a future local green hydrogen story. Those are real safeguards. But the public record does not show the deeper protections that would make the project look like a tightly bounded experiment. I have not found public evidence of a 95% station uptime guarantee, fuel delivery damages, a published hydrogen price cap, a hydrogen-specific spare fleet plan, diesel fallback cost disclosure, a public monthly reliability dashboard, a decommissioning bond, or a station exit strategy. Those provisions may exist in non-public contracts. If they do, publishing performance outcomes would help taxpayers understand whether the project is working. Subsidies are central to the story. Large public support reduces Saarbahn’s capital pain, but it does not eliminate the economic cost. Subsidies move costs. They do not erase them. They do not make compressors cheaper, hydrogen denser, trailer logistics simpler, or small fleet utilization better. A 40% subsidy can make a project easier to approve while leaving the operating system exposed to high fuel cost, station maintenance, downtime, and refurbishment risk. This is not unique to Saarbahn. Capital grants often reward visible procurement events. A hydrogen station has a ribbon-cutting. It signals innovation. It fits regional industrial policy. Grid upgrades, charger redundancy, block redesign, and boring depot electrical work are less photogenic. They may also be lower-risk paths to the same service outcome. Public funding can help agencies adopt new technology, but it can also blur the line between a transit decarbonization strategy and an industrial-policy demonstration. The Freisen green hydrogen plan should be viewed through the same lens. If it arrives, it may improve emissions accounting. Local renewable hydrogen is a better carbon story than gray hydrogen delivered by truck. But green hydrogen can improve the carbon story without fixing the station denominator. The questions remain practical: how much hydrogen will the electrolyzer produce, at what utilization, with what storage, at what delivered cost, and with what backup supply when wind output is low? That is the broader lesson. Saarbahn is interesting because it is not a silly case. It has hilly service, long bus blocks, public funding, a depot station, and a future green hydrogen plan. If the arithmetic is difficult in a reasonably favourable hydrogen bus case, transit agencies with weaker cases should be cautious. Hydrogen bus projects often begin with edge-case arguments. Long routes. Cold weather. Hills. Short layovers. Fast refueling. Existing depot fuel culture. Local hydrogen economy goals. Those conditions can make hydrogen worth studying. But the recurring problems are usually not just inside the bus. They are in fuel supply, station utilization, delivered hydrogen price, refueling reliability, maintenance complexity, and fleet availability. Before approving a hydrogen station, a transit agency should publish route-level modeling of duty cycles, loads, gradients, weather, layovers, depot constraints, and schedule recovery margins. It should compare hydrogen with depot-only battery-electric, depot plus opportunity charging, and selective in-motion charging. It should show grid connection costs, charger redundancy, battery degradation assumptions, and spare ratio impacts. Hydrogen should be modeled with station capex, station opex, delivered fuel cost, reliability, spare fleet, refurbishment timing, and decommissioning. The sensitivity analysis should be public. Hydrogen price should not be a single optimistic number. It should be shown across €8/kg, €12/kg, €15/kg, and €20/kg delivered cases. Station utilization should be shown for 28 buses, 60 buses, and full-fleet conversion. Reliability should be tested at 80%, 90%, and 95%. Station life should be tested at 8, 10, and 15 years. The result should be shown in €/kg, €/km, and annual fleet cost. A hydrogen bus program should also report monthly kg dispensed, station downtime, bus availability, diesel fallback kilometres, delivered hydrogen price, station maintenance events, and actual consumption in kg per 100 km. If the system performs well, the agency can show it. If it performs poorly, decision-makers can correct course before the next procurement round. Saarbahn’s new hydrogen station moves the debate from aspiration to arithmetic. If the fleet remains small, if useful reliability is around 80%, if the station does not expand, and if a refurbishment decision arrives after 8 to 10 years, the kilograms remain very expensive. A delivered hydrogen assumption of €13.50/kg can become about €23/kg at the nozzle once station capex and opex are included. That can become about €1.8/km for energy and refueling infrastructure, or about €2.6 million per year more than diesel for 28 buses. That does not prove Saarbahn’s project will fail. It shows the burden it has to overcome. The buses have to be reliable. The station has to be reliable. Delivered hydrogen has to be cheaper than many market indicators suggest. The fleet probably has to expand enough to improve station utilization. The future green hydrogen supply has to arrive at a credible cost. Battery-electric alternatives must remain less suitable after current charging options are modeled, not just after old range assumptions are repeated. The lesson for other transit agencies is simple. Before opening a hydrogen refueling station, make sure the denominator is large enough to carry it. Hydrogen does not have to be banned from consideration, although I think the evidence supports that choice. It must be required to compete against battery-electric buses, opportunity charging, and in-motion charging as a full system, with all infrastructure costs, reliability risks, and exit costs included. Otherwise, an agency may think it is buying zero-emission buses, while the refueling station is quietly buying it a very expensive fuel bill.

!['Come get some free [electricity]': Owner offers promotional free refueling at massive EV charging station](https://cdn.topcarnews.net/thumb/id/aHR0cHM6Ly9tZWRpYS56ZW5mcy5jb20v-ZW4vdGhlX2Nvb2xfZG93bl83MzcvYTVm-MDg1ODk2N2ZmOThkYjk5NDZiZmU4ZmFm-MjFmZjk/e1fb34ce63b412c1e70fd7086dfb4bd7.jpg?t=20260810&post_id=26026)