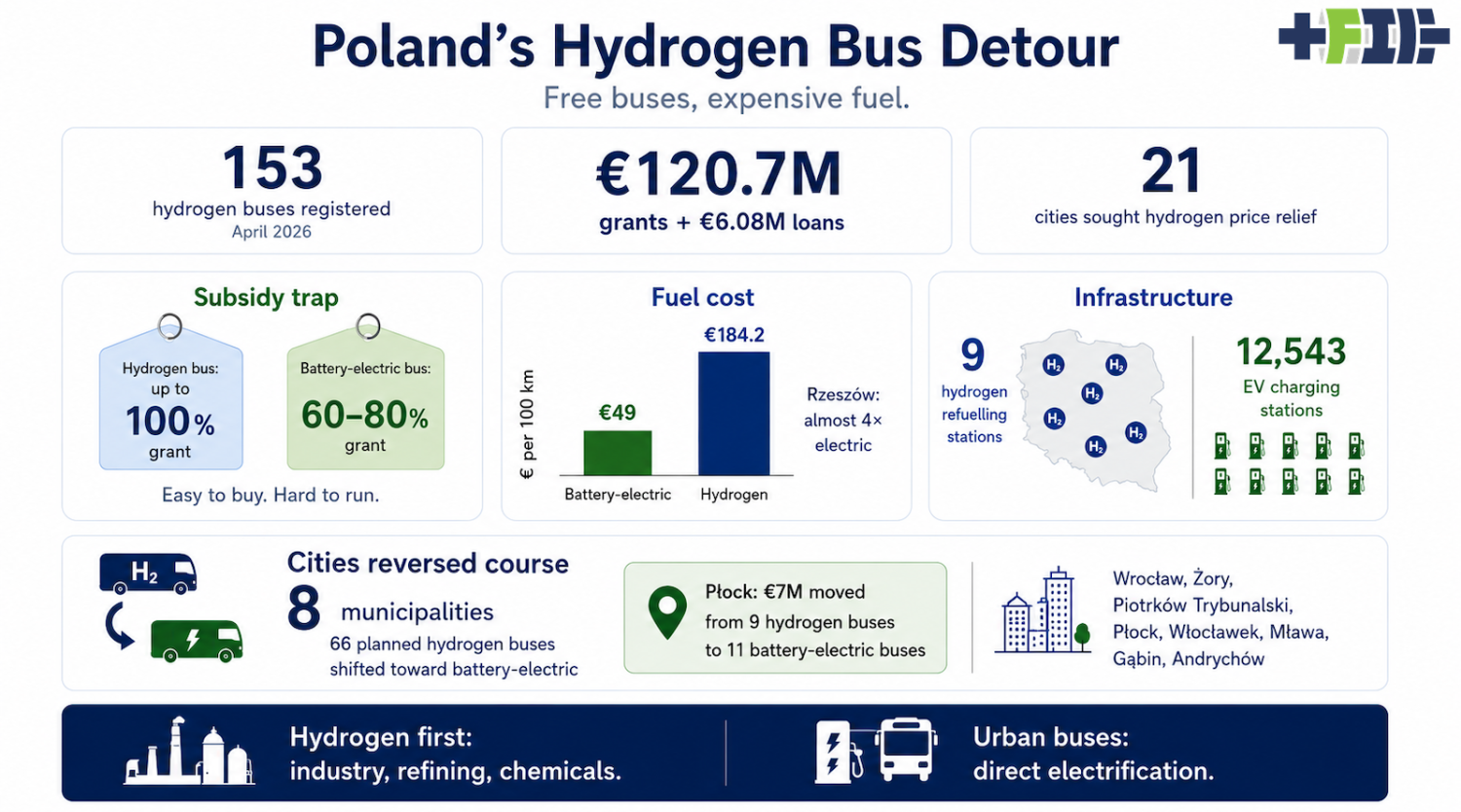

CEE Bankwatch’s May 2026 report, Hydrogen buses in Poland: Where did it all go wrong?, is useful because it moves the hydrogen bus debate out of the brochure and into the depot. It is not another model of what hydrogen might cost in 2035. It is a record of what happened when cities bought buses, signed contracts, waited for fuel, paid invoices, dealt with failed tenders, and tried to run public transport with a fuel system that had not caught up with the promise. By April 2026, Poland had 153 hydrogen buses registered, 140 in service across 12 cities, and another 107 contracted. That is enough deployment to stop pretending this is only about pilots. That matters because Poland is not a trivial case. It is a serious European transit market, a serious bus manufacturing country, and a coal-heavy economy trying to move. In 1990, coal provided about 98% of Poland’s electricity generation. By 2023, that had fallen to about 60.5%, while renewables had risen to about 27% of electricity production. That is still far too coal-heavy for a climate-stable grid, but it is also a large shift in a country with deep coal dependence, industrial inertia, mining politics, and a legacy power system built around lignite and hard coal. That context makes the hydrogen bus detour more interesting. Poland chose hydrogen buses while battery-electric buses were scaling across Europe, charging infrastructure was spreading, and electricity was getting cleaner. The question is not whether Poland should decarbonize buses. The question is why scarce public money and municipal attention were directed toward a fuel-cell pathway that added cost, infrastructure risk, supply-chain risk, and weaker climate accounting when a direct electrification pathway was already available. The answer starts with policy design. Poland’s hydrogen strategy treated public transport as a low-hanging fruit for creating a national hydrogen economy. The strategy set targets of 100 to 250 hydrogen buses by 2025 and 800 to 1,000 by 2030. It also set targets for fuelling stations and low-emission hydrogen production capacity. On paper, this created a tidy industrial story. Buses would create demand. Demand would justify refuelling stations. Refuelling stations would justify hydrogen production. Hydrogen production would help create a national industry. The problem is that buses are not an industrial-policy prop. They are public service machines. They exist to move people reliably, affordably, and with low emissions. Hydrogen became an object of policy in itself, instead of one possible tool to compare against alternatives. The first question should have been simple. What reduces emissions at the lowest cost with the least operational risk for urban buses? For most cities, most routes, and most depots, the answer has been battery-electric buses for years. They are not magic. They require depot planning, grid connections, chargers, maintenance training, route scheduling, and some operational changes. But they use electricity directly, and that matters. Every conversion step avoided is a cost avoided. The subsidy structure made the error worse. According to the Bankwatch report, Polish support schemes could cover up to 100% of hydrogen bus purchase costs, while grants for battery-electric buses often covered 60% to 80%. That turned hydrogen buses into a municipal bargain at the point of purchase, even though their actual market cost was higher than battery-electric alternatives. The capital cost was socialized. The operating cost was municipalized. The physics stayed on the invoice. A city could buy the bus cheaply, or close to free, but it still had to find hydrogen, pay for hydrogen, deal with hydrogen infrastructure, and absorb the service risk when the fuel system failed. The public funding numbers are not small. Bankwatch reports more than €120.7 million in non-repayable grants and just under €6.08 million in loans for hydrogen buses and refuelling stations, financing 163 buses and 2 stations directly. That is about €117.7 million in direct bus grants for 163 buses, or roughly €722,000 per bus in non-repayable subsidy before the smaller loan component is added. When a technology needs that level of capital support and then still generates fuel-price relief requests, the problem is not a lack of ambition. The problem is that the economic case has not landed. I wrote about this problem in January 2025, when Poland’s hydrogen bus plans were already running into high hydrogen prices. At the time, 21 Polish municipalities had asked the national government for help with hydrogen operating costs. The mayors of Chełm and Wałbrzych wrote to the Minister for Climate and Environment seeking a support program to cover the price gap between hydrogen and traditional fuels. They estimated €35 million to €70 million would be required from 2025 to 2027 for several hundred buses, with annual costs rising to €46.7 million to €116.6 million afterward. This was the moment the subsidy shell game became obvious. Public money bought the buses. Then cities asked for public money to fuel them. Chełm made the problem concrete. The city’s hydrogen buses were refuelling at about €16.1 per kilogram, creating roughly €639,000 in extra annual operating costs compared with diesel. That was the comparison the cities used when asking for help. The more relevant comparison is with battery-electric buses, because those are the main zero-emission alternative. Bankwatch reports that in Konin, hydrogen buses cost four times as much per 100 kilometres as electric buses. In Rybnik, hydrogen operation was more than three times diesel and four times hybrid. In Rzeszów, hydrogen at €19.9 per kilogram was projected to cost €184.2 per 100 kilometres, almost four times the electric bus operating cost. Over 15 years, those numbers stop being annoying and become structural. Rzeszów’s projected fuel bill for 20 hydrogen buses was €28.1 million, which was €4.7 million more than the purchase price of the buses themselves. That is the point too many hydrogen bus studies obscure. A bus is not a procurement object. It is a 12 to 15-year operating commitment. If the fuel is expensive, volatile, and hard to secure, the purchase grant merely delays the reckoning. The climate accounting problem is just as important. Hydrogen buses are called zero-emission because nothing carbon-based comes out of the tailpipe. That is a regulatory label, not a lifecycle finding. Bankwatch notes that Poland’s legal definition of a zero-emission bus considers only direct vehicle emissions and ignores emissions from fuel production and the wider supply chain. That matters in a country that produces about 1.1 million tons of hydrogen per year, with more than 97% coming from fossil gas through steam methane reforming. Poland’s hydrogen system is not green by default. It is fossil hydrogen with a small and constrained green edge. The report also notes that Polish transport hydrogen marketed as green does not necessarily qualify as renewable fuel of non-biological origin under EU rules. The Konin electrolyser, for example, was described as using 40% solar and wind electricity and 60% electricity from woody biomass combustion. Biomass may receive renewable treatment in some policy systems, but it is not RFNBO-compliant for this purpose. That is enough to make the climate claims much weaker than the marketing. My own assessment of hydrogen buses has usually added another problem that the Bankwatch report does not lean into enough. Hydrogen leakage matters. Hydrogen is an indirect greenhouse gas because it affects atmospheric chemistry in ways that extend the lifetime of methane and influence ozone and stratospheric water vapour. Bankwatch’s case is already strong before leakage. Adding production, compression, trucking, dispensing, and leakage makes the climate case for hydrogen buses thinner still. The infrastructure problem is not a footnote. Battery-electric buses need infrastructure too, but electricity is everywhere and charging infrastructure is scaling across the economy. Hydrogen buses need a dedicated fuel chain. They need production or supply contracts, purification, compression, transport, storage, dispensing, safety systems, specialized maintenance, and enough throughput to keep stations from losing money. This is not just “refuelling is faster.” It is an entire parallel fuel system for a small number of vehicles. The numbers show the imbalance. By the end of 2025, Poland had only nine hydrogen refuelling stations. By March 2026, electric vehicles could use 12,543 charging stations across the country. Those are not equivalent networks, and pretending they are equivalent because both involve infrastructure is category confusion. One is an extension of the electricity system. The other is a new fuel system trying to exist before it has customers, scale, low-cost supply, or a clear climate advantage. ZE PAK’s experience shows what happens when station economics meet reality. The company originally planned 30 commercial hydrogen refuelling stations and assumed an 85% utilization rate by 2032. Instead, its public hydrogen stations were unprofitable for a second year. The net loss for its hydrogen infrastructure subsidiary grew from €600,000 in 2023 to €3.3 million in 2024. It then shelved expansion plans and returned €14.9 million in subsidies rather than carry the remaining capital burden. That left cities with commissioned buses facing uncertain local fuel access. This is not an operator failing to believe hard enough. It is a utilization problem. The operational failures are instructive as well. In Poznań, fuel contamination grounded 23 of 25 hydrogen buses for two weeks. A similar problem affected Wałbrzych. Orlen later paid €116,595 in compensation after the contamination was traced to a fire at its hydrogen production line in Włocławek. The issue is that hydrogen buses create specialized dependencies. Fuel purity is not optional. Station uptime is not optional. Supplier reliability is not optional. A single point of failure can ground a fleet. The winter resilience story also took a hit. Hydrogen buses are often marketed as better in cold weather because fuel cells produce waste heat. That can be true in some operating conditions, but it is not a free pass through winter. Bankwatch reports that Chełm’s hydrogen fleet stopped operating below -20°C after heating and hydrogen fuel system failures. Tychy kept new buses in the depot until March 2026 after test runs ended in breakdowns. This does not prove battery-electric buses are perfect in winter. It proves that hydrogen buses are not exempt from cold-weather engineering, and that a marketing claim is not the same thing as fleet resilience. The cities are now learning. At least eight Polish municipalities that had applied for funding for a combined 66 hydrogen buses amended their plans toward battery-electric alternatives, including Wrocław, Żory, Piotrków Trybunalski and Płock. Płock is especially telling because it is Orlen’s home city. It reallocated about €7 million originally intended for 9 hydrogen buses to buy 11 battery-electric buses instead. When the home city of the national oil and hydrogen champion shifts money from hydrogen buses to battery-electric buses, the market signal is not subtle. That is not anti-innovation. It is evidence of learning after operating data arrived. Lublin adds the manufacturer-risk dimension. It selected Arthur Bus, a Polish-German startup, to deliver 20 hydrogen buses. The company later declared bankruptcy. Lublin could not run a new tender or source alternative vehicles in time to meet project deadlines and lost €15 million in funding. That is not just one failed supplier. It is a symptom of a niche market where demand is driven by subsidies, volumes are thin, and manufacturers can be exposed when public programs do not create durable demand. That brings us to Solaris. Solaris is not Arthur Bus. It is a serious manufacturer with real products, real engineering depth, and a major position in European transit. That is why its hydrogen strategy matters. In November 2025, I wrote that Solaris was winning the wrong race in Europe’s zero-emission bus market. It had become Europe’s leading hydrogen bus supplier, but the hydrogen segment was small while battery-electric buses were dominating new zero-emission city bus sales. The strategic concern was not that Solaris could not build hydrogen buses. The concern was that it could. A company can succeed at the wrong product. Solaris has won hydrogen bus tenders in Poland and elsewhere, but those wins bind engineering attention, supply chains, maintenance systems, sales focus, and management narrative to a market that public policy created but operational reality is shrinking. A home market inflated by grants can look like validation, when it is actually a distorted signal. Every engineering hour spent integrating fuel cells, high-pressure hydrogen systems, fuel-cell thermal management, hydrogen safety, and specialized diagnostics is an hour not spent advancing battery-electric platforms, charging interfaces, depot integration, software, cost reduction, and manufacturing scale. That strategic misalignment is painful because Solaris has strengths that should matter in the winning market. Europe needs reliable, affordable, standardized battery-electric buses. It needs manufacturers that can scale production, improve range without overbuilding batteries, integrate depot and opportunity charging, reduce maintenance costs, and help operators electrify fleets route by route. Solaris can do that work. But hydrogen leadership risks making it a champion in a category that depends on grant design, fuel subsidies, and municipal optimism. The European lesson is broader than Poland and broader than Solaris. Parallel pathways are not free. Supporting hydrogen buses alongside battery-electric buses did not simply preserve optionality. It split procurement, policy attention, manufacturing learning, maintenance training, infrastructure planning, and public funding. A city that spends two years on hydrogen fuel tenders is not spending those two years optimizing depot charging. A ministry that funds hydrogen refuelling stations is not putting that money into grid connections, chargers, and depot upgrades. The right policy correction is not complicated. Renewable hydrogen should first replace existing fossil hydrogen in industry, chemicals, refineries, and other sectors where hydrogen is already used and where direct electrification is difficult or uneconomic. Poland already consumes large volumes of fossil hydrogen. That is the no-regrets decarbonization target. Creating new hydrogen demand in urban buses before cleaning up existing hydrogen demand is poor sequencing. It increases competition for scarce renewable hydrogen while avoiding the bus technology that uses electricity most efficiently. For urban buses, direct electrification should be the default. Not because batteries are perfect. Because they are good enough, improving, cheaper to operate, easier to fuel, and tied to an electricity system that is decarbonizing anyway. The policy task is to make the default easier. That means depot grid upgrades, predictable charging support, better route planning, procurement standardization, operator training, and electricity tariffs that reward managed charging. It also means forcing cost-benefit analyses to compare modern battery-electric buses against hydrogen buses using current data, real fuel prices, maintenance costs, infrastructure costs, and lifecycle emissions. Poland’s hydrogen bus experience is useful because it produced evidence. The lesson is not that Poland should slow its transport transition. The lesson is that Poland can move faster by narrowing focus. The Bankwatch report should end the claim that the only problem is lack of scale. Poland tried creating scale through grants. The result was high fuel costs, fragile supply, station losses, fuel-quality failures, city reversals, and requests for operating subsidies. It should also end the idea that winning hydrogen tenders is proof of strategic strength. For Solaris and other manufacturers, the better prize is the large, boring, battery-electric market that is actually decarbonizing city buses. For Poland, the better prize is simpler. Use public money to buy emissions reductions, not hydrogen demand.