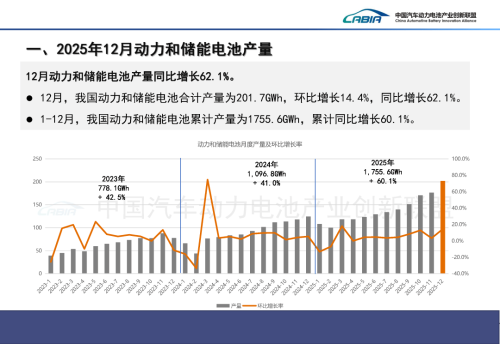

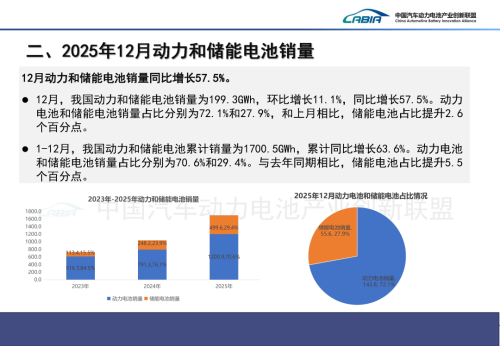

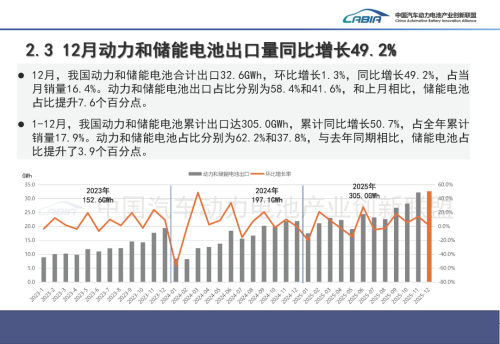

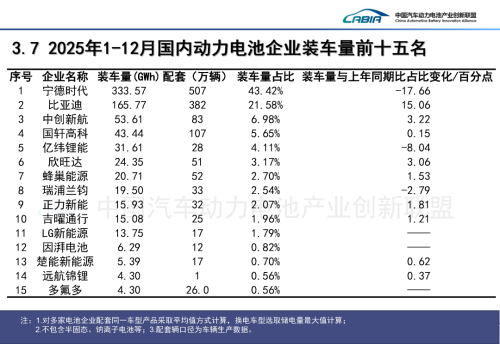

In 2025, ternary battery installation accounted for 144.1 GWh, while LFP batteries reached 625.3 GWh. On January 16, the China Automotive Battery Innovation Alliance released its monthly power battery report for December 2025. Data showed that China’s combined output of power and energy storage batteries totaled 201.7 GWh in December, up 14.4% month on month and 62.1% year on year. Full-year output reached 1,755.6 GWh, marking a year-on-year increase of 60.1%. Production volume of power and energy storage batteries in December 2025 and 2025 In terms of sales, combined power and energy storage battery sales reached 199.3 GWh in December, up 11.1% from November and 57.5% from a year earlier. Power battery sales accounted for 143.8 GWh, or 72.1% of the total, while energy storage battery sales stood at 55.6 GWh. For the full year 2025, cumulative sales of power and energy storage batteries reached 1,700.5 GWh, up 63.6% year on year. Power batteries accounted for 1,200.9 GWh, or 70.6% of total sales, while energy storage batteries totaled 499.6 GWh. Sales volume of power and energy storage batteries in December 2025 and 2025 On the export front, China exported a combined 32.6 GWh of power and energy storage batteries in December, up 1.3% month on month and 49.2% year on year, accounting for 16.4% of monthly sales. Power battery exports stood at 19.0 GWh, while energy storage battery exports reached 13.6 GWh. The cumulative exports of power and energy storage batteries reached 305.0 GWh in 2025, up 50.7% year on year. Power battery exports totaled 189.7 GWh, while energy storage battery exports reached 115.3 GWh. Export volume of power and energy storage batteries in December 2025 and 2025 In terms of installation mix, lithium iron phosphate (LFP) batteries continued to dominate. China’s power battery installations totaled 98.1 GWh in December, including 18.2 GWh of ternary batteries and 79.8 GWh of LFP batteries, which accounted for 81.3% of the total. For the full year, the cumulative power battery installations reached 769.7 GWh, up 40.4% year on year. Ternary batteries accounted for 144.1 GWh, while LFP batteries reached 625.3 GWh. By company, CATL ranked first in 2025 with power battery installations of 333.57 GWh, holding a market share of 43.42%, though down 17.66% year on year. Top 15 companies involved in battery vehicle installations in China for January to December 2025 BYD ranked second with 165.77 GWh and a market share of 21.58%. Together, the two companies accounted for about 65% of the market, indicating a largely stable industry structure. Overall, China’s power battery industry maintained relatively fast growth in 2025 despite a high base, with energy storage and exports emerging as key growth drivers, while LFP batteries remained dominant due to cost and safety advantages.