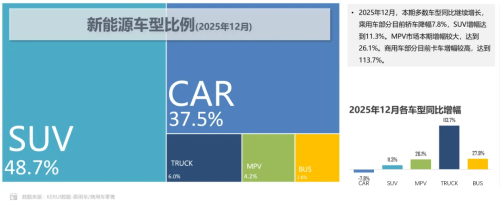

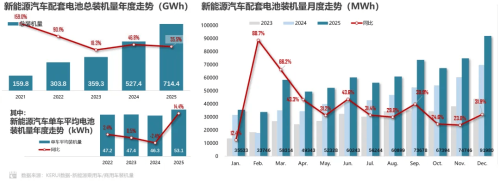

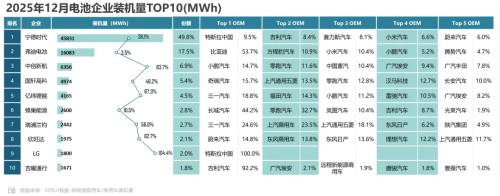

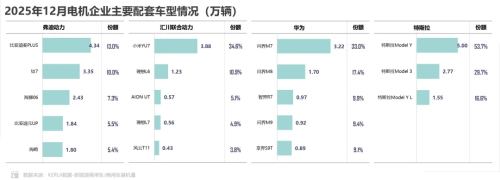

In December 2025, the MPV segment saw significant growth of 26.1%, SUVs grew by 11.3%, while the sedan segment declined by 7.8%. The China Passenger Car Association released the December 2025 New Energy Vehicle Three-Electric Systems Report today. First, let’s review the general trends of the Chinese new energy vehicle market in 2025. Data shows that China’s new energy vehicle production reached 16.524 million units in 2025, a year-on-year increase of 25.1%, with the cumulative penetration rate reaching 47.5%. Looking specifically at December, new energy SUVs held a market share of 48.7%, dominating nearly half the market. This was followed by sedans at 37.5%, with the remaining shares being MPVs at 4.2%, trucks at 6.0%, and buses at 3.6%. It is worth noting that the MPV segment saw significant growth of 26.1%, SUVs grew by 11.3%, while the sedan segment showed a downward trend with a decline of 7.8%. December 2025 NEV Market Share The continuously growing penetration rate of new energy vehicles is driving sustained growth in power battery installation. Data shows that in December 2025, the installed capacity of power batteries for new energy vehicles reached 92.0 GWh, a year-on-year increase of 31.9%. The average battery capacity per vehicle in December was 62.5 kWh, a year-on-year increase of 23.2%. Among the contributors, BYD, Tesla, and Xiaomi were the main enterprises driving the installed capacity. The total installed capacity from January to December was 714.4 GWh, a year-on-year increase of 35.5%. Monthly/Annual NEV Battery Installation Trends Looking at specific cell materials, the proportion of LFP batteries used in the passenger vehicle market continues to rise, increasing from 65.8% in 2024 to 74.6% in 2025. In contrast, the market share of NCM batteries declined from 33.4% to 23.9%. Regarding enterprise supply partnerships, in December 2025, the top three enterprises held a combined market share of 74.2%, while the top ten enterprises accounted for 95.6%. CATL maintained its leading position with a current share of 49.8%; followed by FinDreams Battery with a market share of 17.5%. CALB, benefiting from sales growth at XPeng and Leapmotor, ranked third in current installed capacity with a share of 6.9%. It also became the fastest-growing Chinese battery manufacturer, with a growth rate reaching 83.7%. Top 10 Battery Suppliers by Installation Volume, December 2025 In the electric drive field, in December, the combined share of the top ten drive motor enterprises reached 62.5%, and the supply volume in December increased month-on-month. Specifically, FinDreams’ top five models accounted for 41.2% of its supply, with the BYD Qin PLUS alone contributing 13.0%. It is noteworthy that among these top five models, except for the Fangchengbao Tai7, the other models have relatively low single-vehicle prices. These volume-selling models ensure FinDreams’ monthly supply volume. For Inovance Technology, the Xiaomi YU7 accounted for the highest proportion among its supplied models, reaching 34.6%. Huawei’s main supplied models are the AITO series, with the M7 model accounting for 33.0% of its share. Tesla primarily equips its own brands, with the Model Y alone accounting for 53.7% of its share. Key Vehicle Models by Motor Supplier, December 2025 Additionally, in December, the top ten electronic control suppliers held a combined share of 58.6%. In this period, the supply volumes for FinDreams and UAES saw year-on-year declines. Among Huawei’s current partner enterprises, Seres accounts for 66.6%. BYD’s Fangchengbao Tai7 performed outstandingly in sales, with this single model accounting for 12.2% of its share. Inovance Technology’s main supplied model remains the Xiaomi YU7, with this single model accounting for 34.6% of its share. Tesla’s star model is the Model Y, accounting for 53.7% of its share, and Huawei’s star model is the AITO M7, accounting for 35.5% of its share.