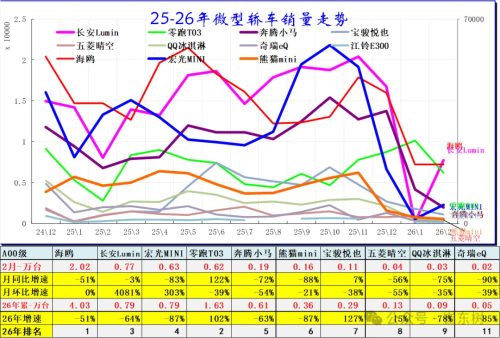

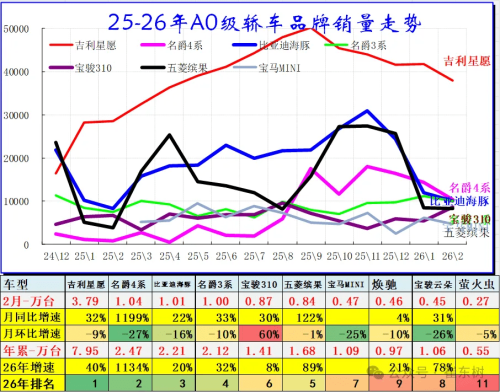

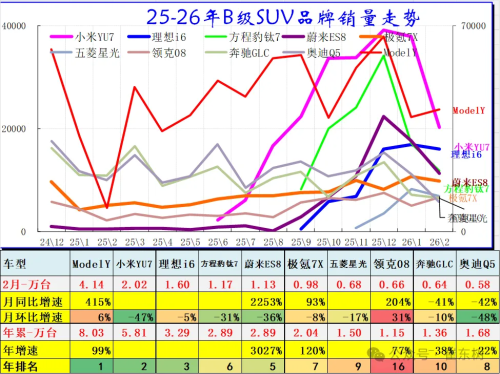

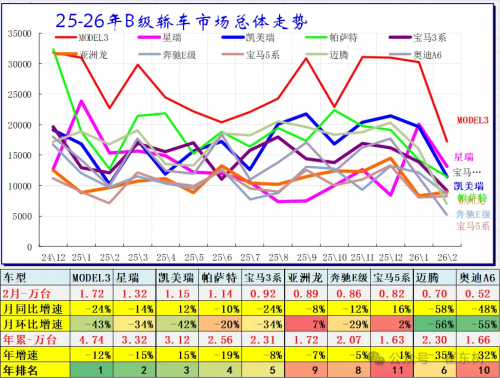

On March 23, Cui Dongshu, secretary-general of the China Passenger Car Association (CPCA), released February 2026 segment-level data for the domestic passenger vehicle market. Overall retail sales fell 25% year-on-year in February, significantly steeper than the 14% decline at the wholesale level. The primary driver was the phased withdrawal of early-year vehicle replacement subsidies, which directly disrupted end-market demand. Structurally, the entry-level segment was hit the hardest. A00-class sedans saw retail sales plunge 80% year-on-year, while wholesale volumes dropped 61%. Sales trends of A00-class sedans for the years 2025-2026 Despite the downturn, leading models maintained some scale. BYD Seagull ranked first with 20,200 units, followed by Changan Lumin and Wuling Hongguang MINI with 7,700 units and 6,300 units, respectively. In contrast, the A0-class sedan segment showed resilience. Wholesale volumes rose 16% year-on-year, making it one of the few growing segments. Electrification in this price band is largely complete, with internal combustion vehicles rapidly losing relevance. Geely Xingyuan led the segment with 37,900 units, followed by SAIC MG4 series at 10,400 units and BYD Dolphin at 10,100 units, indicating a high level of sales concentration. Sales trends of A0-class sedans for the years 2025-2026 SUVs remained the core of the market. A-class SUVs reached 487,100 units in wholesale volume, accounting for more than half of total sales. Although down 38% year-on-year, they continued to dominate overall demand. Within this category, A0-class SUVs declined 10% in wholesale and 50% in retail. MG ZS, Geely Binyue, and Chery Omoda 5 ranked among the top sellers. At the higher end, the B-class SUV segment reversed the broader trend. Wholesale volumes increased 31% year-on-year, while retail sales rose 17%. Sales trends of B-class SUVs for the years 2025-2026 Among leading models, Tesla Model Y recorded 41,400 units, followed by Xiaomi YU7 at 20,200 units and Li Auto i6 at 16,000 units. With sales reaching 11,200 units in February, the NIO ES8 ranked fifth, representing a massive year-on-year surge of 2,253% and becoming the fastest-growing B-segment SUV that month. Premium new energy vehicles are increasingly achieving scale advantages in this segment. The sedan market showed divergence. A-class sedans declined sharply overall, though the share of new energy vehicles continued to rise. In the B-class sedan segment, Tesla Model 3 led with 17,200 units, followed by Geely Xingrui at 13,200 units and Toyota Camry at 11,500 units. Sales trends of B-class sedans for the years 2025-2026 ICE models still retain a base level of demand, though their share continues to shrink. The A0-class SUV and MPV segments remained relatively weak. A0 SUVs saw retail sales fall 50% year-on-year, with domestic brands becoming dominant after Japanese and Korean automakers largely exited. The MPV market entered a low-growth phase, with B-class MPV retail sales up 45% year-on-year but still limited in scale. Wuling Xingguang ranked first with 7,100 units. Overall, subsidy adjustments have had a more direct impact on the lower-priced segments, while mid- to high-end new energy vehicles have demonstrated stronger resilience. Notably, B-class SUVs have emerged as the fastest-growing segment in the current market.