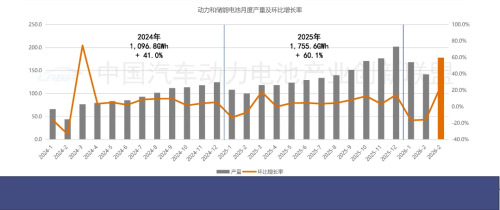

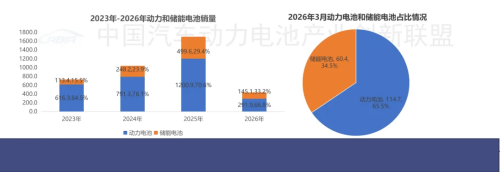

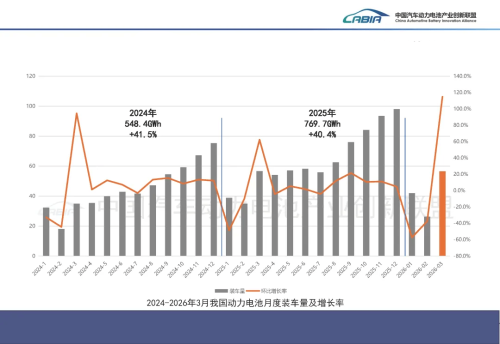

On April 10, the China Automotive Battery Innovation Alliance released its monthly data on power battery development for March 2026. Data showed that total output of power and energy storage batteries in China reached 177.7 GWh in March, up 25.5% month-on-month and 50.2% year-on-year. Cumulative output in the first quarter reached 487.4 GWh, marking a 49.3% year-on-year increase. Output and growth rates of China’s EV batteries from 2014 to Mar 2026 In terms of sales, total battery sales reached 175.1 GWh in March, up 54.7% month-on-month and 51.6% year-on-year. Following adjustments earlier in the year, the industry is returning to an upward trajectory. Power battery sales accounted for 114.7 GWh, representing 65.5% of total sales, while energy storage batteries contributed 60.4 GWh. Cumulative sales for January–March reached 437.1 GWh, up 52.9% year-on-year. Sales volume of China’s power and energy storage batteries from 2023 to Mar 2026 Exports continued to grow. In March, total battery exports reached 36.1 GWh, up 57.1% year-on-year, accounting for 20.6% of total monthly sales. Of this, power battery exports stood at 22.3 GWh, while energy storage battery exports reached 13.8 GWh. Total exports for the first quarter amounted to 84.1 GWh, up 36.7% year-on-year. Driven by demand for new energy vehicles, power battery installations remain the key industry indicator. In March, domestic installations reached 56.5 GWh, up 114.9% month-on-month and down marginally by 0.1% year-on-year. China’s battery installations from 2024 to Mar 2026 By chemistry, lithium iron phosphate batteries continued to dominate due to cost and safety advantages, with installations of 45.8 GWh, accounting for 81% of the total. Ternary batteries recorded installations of 10.7 GWh. In the first quarter, cumulative domestic power battery installations reached 124.9 GWh, down 4.1% year-on-year. LFP batteries accounted for 99 GWh, while ternary batteries totaled 25.8 GWh. By vehicle type, battery electric vehicles remained the primary source of demand, accounting for 82.7% of installations in March. Plug-in hybrid vehicles accounted for 17.3%, while fuel cell vehicles represented just 0.015%. Top 15 battery manufacturers in battery installation volume for Mar 2026 in China Industry concentration remained high. A total of 31 battery manufacturers achieved installation volumes in March, down by 10 compared with a year earlier. The top 10 companies accounted for 52.9 GWh, representing 93.6% of total installations, indicating further consolidation toward leading players. At the company level, CATL ranked first with 25.71 GWh of installations, holding a 45.54% market share. BYD followed with 10.06 GWh, accounting for 17.83%. Together, the two companies captured a combined market share of 63.37%, maintaining a dominant position in China’s battery market. They were followed by CALB, Gotion High-Tech, EVE Energy, and LG Energy Solution, with installation volumes of 3.52 GWh, 3.37 GWh, 2.74 GWh, and 1.92 GWh, respectively.