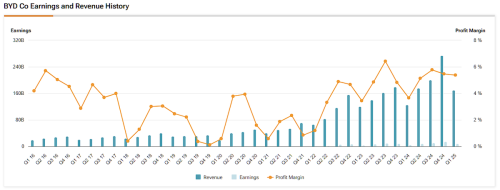

In 2025, BYD became the largest producer of PHEVs, BEVs, and NEVs overall globally. It was the top automotive company in China. It was also the largest exporter of BEV buses. And it was the top producer of Battery Energy Storage Systems (BESS) by installed capacity. However, in its recently released annual report, BYD’s net earnings declined 18.97% YoY. A net margin of 4.1% was down from 5.2% a year ago. Revenue was up 3.5% YoY. Excluding BYD’s electronics manufacturing business (which makes products like the iPad), BYD’s automotive and related business, which makes up 80.7% of revenue, saw gross margin slip 1.8% to 20.5% last year. The company also paid more in domestic taxes than it made in net profit. In context with other automakers, that slightly beat Tesla’s net margin, while Tesla saw declining revenue, leading to BYD pulling ahead in net earnings. Tesla also paid no US federal income tax. BYD’s automotive gross margin was also higher, even when including regulatory credits for Tesla. GM, Ford, Stellantis, and Renault lost money in 2025. Volkswagen saw a 2.1% net margin. Honda, Nissan, and Mazda have fiscal years ending March 31, but they are anticipated to post significant losses. Toyota margins are projected by the company to be higher at 7.1%, but the YoY drop will be larger. Hyundai also had a higher net margin at 5.9%, but that also represented a larger YoY drop. In China, Geely, which gets roughly half of its sales from NEVs, had a higher 4.9% net margin. However, that signifies a larger drop from 6.9% last year. Though, Geely’s revenue increase kept net earnings essentially flat. Compared to other NEV-only makers, BYD is still ahead. However, BYD also increased its R&D last year to 63.4 billion RMB ($9.17 billion USD) and increased its R&D engineering staff. That is almost twice as much in R&D as its net profit. While other automakers lost money scaling back their investments in vehicle electrification, BYD increased its investments. At the same time, BYD’s balance sheet improved, with total shareholder equity (assets minus liabilities) up 30%. Significant construction was underway, and payment cycles shortened. Overall, moderate net margins while putting money back into growth and development is part of BYD’s business model. 9 months ago, I wrote the following referencing the chart above: “While net margins have fluctuated, they have remained positive as their business evolved. It goes farther back than the chart below. Most of their startup competitors fueled growth by attracting capital to fund years of losses. Tesla didn’t turn their first full year of net profitability until 2020, halfway through this chart. BYD has stayed net profitable and grown gross margins to reinvest in R&D and business growth. Typically, when net profits have risen, they reinvest, increase R&D and/or cut prices to increase scale. From a historical perspective, current net margins are relatively high and overall earnings are growing, so I would expect them to make some shifts.” Overall, we have seen that shift. Net margins at ~4% are closer to their historical average. 5%+ was higher than average. However, margins are not constant, especially around new product launches. For reverence, look at the last two quarters of 2019 and 1Q 2020. Those quarters represent a low point in BYD’s net profit margin. Sales were also down during that period. In March 2020, BYD introduced the first-generation Blade Battery. Image credit: BYD, translated with Google Lens In March 2026, BYD introduced the second-generation Blade Battery, along with new Flash Charging stations. The new battery is being rapidly rolled out across the company’s lineup. Even though BYD just started activating its new chargers this month, there were already 4,990 Flash Charging stations online as of March 25th in China, each with multiple charging stalls. For comparison, there are currently 4,195 NACS fast charging stations in total (including Tesla Superchargers) in the US. In addition, BYD seems to be a bit conservative in its charging speed claims, with independent testing by Yiche.com showing new models meeting speed claims in real-world testing, while some competitors struggled. Image Credit: Yiche, translated with Google Lens I expect BYD’s 1Q 2026 sales, revenue, and margins to be down, as seen with the previous launch. The Osborne effect, clearing out old models, ramping up new models, seasonality, and a disruption in scrappage incentives will drive margins down. Perhaps not as low as the period of the first-generation Blade Battery launch, as far more of their sales come from growing export markets now, but the numbers will almost certainly be down. 2Q could be better. Although, many of the models will not launch until the Beijing Auto Show in April, and production may take some time to ramp up. Hungary and Indonesia production should also be starting in 2Q, with Thailand and Brazil ramping up further. 3Q should be a better indication of where the big picture is heading. At the same time, some competitors are also stepping up. Xiaomi and XPENG have improved products and new technology that should also lead to sales growth in 2Q. While Geely benefitted from less product update disruption in 1Q, it also has a few models being introduced. The EV market is very competitive in China. We could also see a global recession that creates margins closer to what we saw during COVID. And trade policy is uncertain. Energy prices could also see some massive shifts, shifting car buying patterns. The world doesn’t seem to be getting more predictable. Image Credit: BYD However, BYD’s 2025 financial performance makes sense in context, even if expectations are not constantly being exceeded. It also may not be exciting to some, and a bit old fashioned from a US perspective, but the annual report included 25 pages of corporate governance reporting and was accompanied by a Sustainability Report (although, the BYD Global website really needs to upgrade its PDF viewer capability). Overall, if BYD’s net margins start creeping up again, I expect that the company will increase R&D spending again. Some investors might not find that tendency attractive. If you are looking for a company that extracts maximum net margins from its operations, BYD might not be for you. This is not a company led by accountants. It is a company led by engineers and scientists. Margins are likely to go back into research and developing new technologies. From the annual report: “The Group is a global technology enterprise driven by core technological innovation, ranking 91st on the 2025 Fortune Global 500 list. Guided by its “Three Green Visions” of solar energy, energy storage, and electric vehicles, the Group adheres to the core development philosophy of “technology-based, innovation-oriented”. Embodying the engineer spirit of “Dare to Think, Dare to Act, Dare to Persevere”, and leveraging a world-class R&D system built with over 120,000 engineers, more than 71,000 patent applications, and over 42,000 granted patents, the Group has achieved disruptive technological breakthroughs in key sectors such as NEVs, batteries, and electronics. In 2025, it secured the dual global championship titles for NEV sales and energy storage system shipments. Facing the macro trends of the global energy system transitioning from fossil fuels to clean energy, and AI-driven intelligence becoming the core engine of future societal development, the Group remains committed to high-level R&D investment. In 2025, R&D expenditure amounted to approximately RMB63.4billion, representing a year-on-year increase of 17%, with cumulative R&D investment exceeding RMB240 billion.” Image Credit: BYD

![BYD confirms new flagship EV has a range of 1,008 km [Video]](https://cdn.topcarnews.net/thumb/id/aHR0cHM6Ly9pMC53cC5jb20vZWxlY3Ry-ZWsuY28vd3AtY29udGVudC91cGxvYWRz-L3NpdGVzLzMvMjAyNi8wNy9CWUQtR3Jl-YXQtSGFuLUZsYWdzaGlwLUVWLmpwZWc_-dz0xNTAwJmFtcDtxdWFsaXR5PTgyJmFt-cDtzdHJpcD1hbGwmYW1wO3NzbD0x/c37374468f3a539ee1e0ce2b627e08d0.jpeg?t=20260731&post_id=48318)