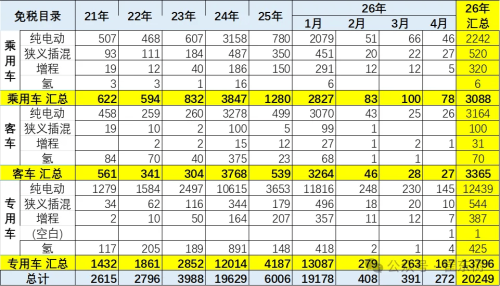

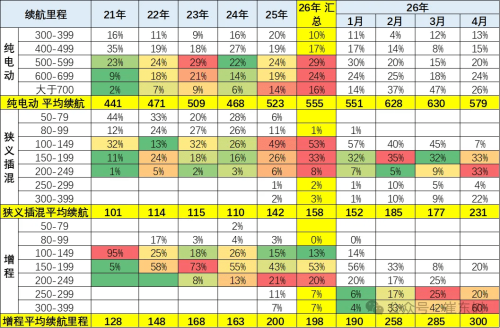

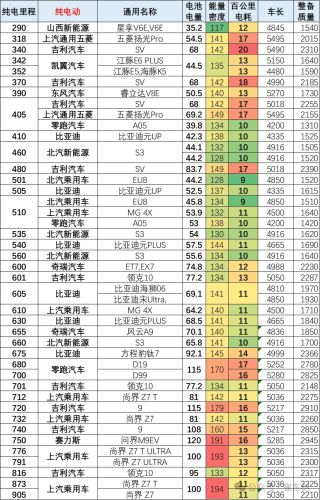

On April 21, Cui Dongshu, secretary general of the China Passenger Car Association, released a report tracking new energy vehicle (NEV) product launches and technology pathways for April. According to catalog data, a total of 20,249 NEV models were included in China’s tax exemption catalog in the first four months of 2026, with 272 new entries added in April. While the overall volume remains relatively low compared with previous years, the product pipeline from February to April is richer than in 2025. NEV product launches in China from 2021 to April 2026 From a structural perspective, battery electric vehicles (BEVs) continue to dominate. In April, BEVs accounted for nearly 80% of new entries, with a notable increase in electric commercial and special-purpose vehicles, which added 145 models. By contrast, plug-in hybrid electric vehicles (PHEVs) and extended-range electric vehicles (EREVs) remain less prominent in catalog share. However, from a product trend perspective, both segments are entering a phase of rapid expansion. Battery swapping models saw a slight increase in 2026, mainly concentrated in commercial BEVs, while growth in the passenger vehicle segment has slowed. NEV product launches in China across different powertrains from 2021 to April 2026 Driving range continues to improve across NEVs. The average range of BEVs has risen from 468 km in 2021 and 523 km in 2025 to 579 km as of April 2026, with a growing number of models exceeding 700 km. Although battery energy density has increased only marginally—from 138 Wh/kg in 2025 to around 143 Wh/kg in April 2026—vehicle-level efficiency optimization continues to drive range improvements. For PHEVs and EREVs, average electric ranges have increased to 231 km and 300 km respectively, with energy densities reaching 132 Wh/kg and 156 Wh/kg. Energy consumption trends show divergence. BEVs maintain an average consumption of around 13 kWh/100 km, while PHEVs and EREVs are higher at approximately 21 kWh/100 km and 24 kWh/100 km, leaving room for further optimization. Electrical range of NEVs across different powertrains from 2021 to April 2026 In terms of product positioning, BEV passenger vehicles are increasingly shifting toward mid-to-large segments. Models exceeding 4.8 meters in length are becoming more common, with 5-meter-class vehicles gradually emerging as the mainstream, reinforcing the premiumization trend. Products such as AITO demonstrate balanced performance across key metrics, while brands like Geely and BAIC stand out in energy efficiency, placing greater emphasis on real-world usability. BEV models in April Within the PHEV segment, domestic brands including Great Wall Motor, Chery and Geely maintain stable competitiveness, with technology pathways becoming increasingly mature. In the EREV segment, recent market performance has been relatively subdued. However, a new wave of long-range models—including AITO M9 and Leapmotor D series—is being introduced, aiming to revive demand through extended electric range and improved efficiency.