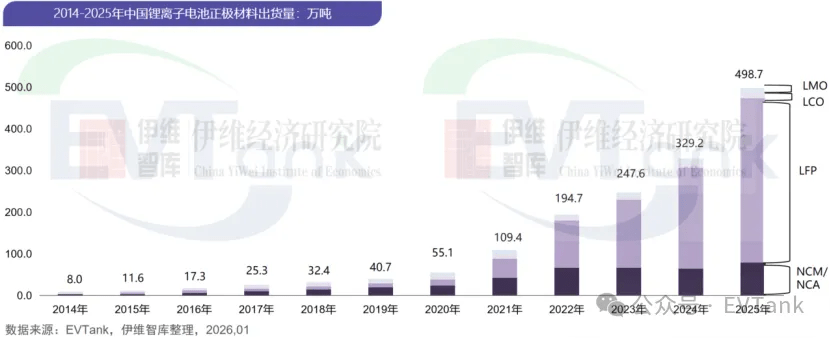

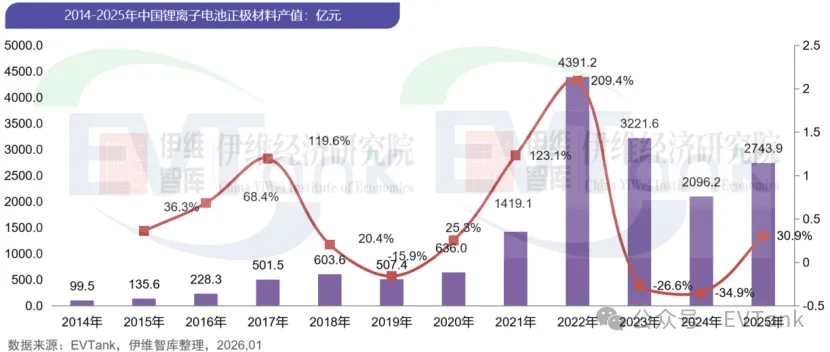

China’s demand for LFP materials is expected to reach 6 million tonnes in 2026, with overall industry growth expected to remain in the 40%–50% range. On January 27, research firm EVTank, together with China Yiwei Institute of Economics, released the China Lithium-ion Battery Cathode Materials Industry Development White Paper (2026). According to the report, China’s total cathode material shipments reached 4.987 million tonnes in 2025, up 51.5% year on year. From a structural perspective, lithium iron phosphate (LFP) remained the dominant growth driver. China’s total cathode material shipments from 2014 to 2025 China’s LFP cathode material shipments totaled 3.944 million tonnes in 2025, representing a year-on-year increase of 62.5% and accounting for 79.1% of total cathode shipments, further lifting its market share. By comparison, ternary cathode materials recorded annual shipments of 786,000 tonnes, up 22.2% year on year. Lithium cobalt oxide and lithium manganese oxide shipments reached 119,000 tonnes and 138,000 tonnes, respectively, rising 20.2% and 12.2% from a year earlier. As China’s NEV and energy storage markets continue to expand, application scenarios that place higher emphasis on safety, cycle life and cost efficiency are growing rapidly, further strengthening the suitability of LFP chemistry in both power and stationary storage batteries. On the pricing and value side, average market prices for LFP and ternary materials declined in 2025 compared with 2024, while prices for lithium cobalt oxide and lithium manganese oxide rose noticeably. Supported by strong shipment growth, the total output value of China’s cathode material industry climbed 30.9% year on year to RMB 274.39 billion ($38.1 billion), ending two consecutive years of decline, though still below the 2022 peak of RMB 439.12 billion ($61.0 billion). China’s cathode material output value from 2014 to 2025 At the company level, concentration in the LFP segment continued to increase. Hunan Yuneng shipped more than 1 million tonnes in 2025, ranking top for several consecutive years, followed by Wanrun Energy and Defang Nano. Demand for LFP materials continued to rise over the past year, with leading battery makers including CATL, BYD, EVE Energy, Sunwoda and CALB steadily increasing procurement volumes. CATL’s LFP battery According to Battery China, purchases by these companies alone approached 6 million tonnes, with total order value exceeding RMB 24 million ($3.33 million). Meanwhile, driven by a rebound in lithium carbonate prices and environmentally driven production curbs, domestic LFP prices have rebounded notably, with mainstream power-grade products now exceeding RMB 60,000 per tonne (approximately $8,330 per tonne). Looking ahead, industry forecasts suggest domestic demand for LFP materials could reach 6 million tonnes in 2026, with overall industry growth expected to remain in the 40%–50% range.