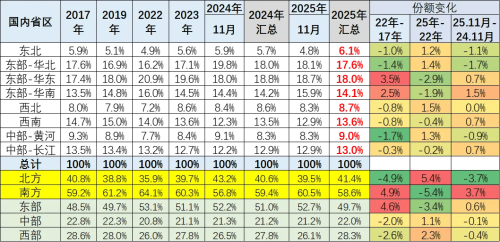

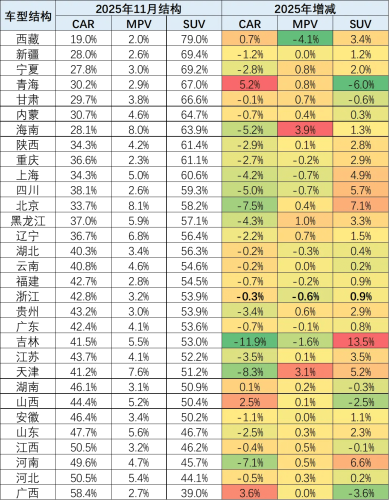

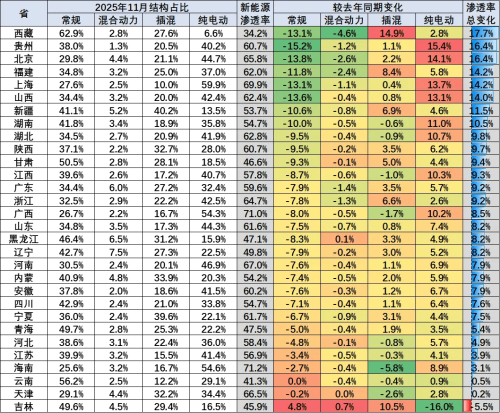

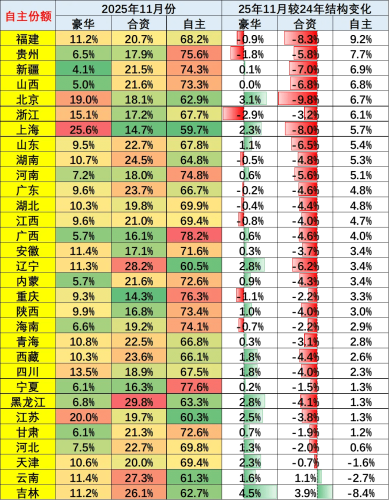

NEVs are gaining traction across regions, with battery electric vehicles driving faster growth in northern China. Based on the China Passenger Car Association’s latest regional market flow analysis for November 2025, China’s passenger vehicle market remained relatively strong from February through September before entering an adjustment phase in October and November, with regional disparities widening further. On a month-on-month basis versus October, changes in subsidy policies emerged as a key driver of regional market performance. The impact of policy support was particularly evident in the mid- to lower-end segments, where demand for economy models rebounded first, underscoring the cushioning role of subsidies on the demand side. In recent years, China’s auto market growth has exhibited a pattern of stronger performance in the north and weaker momentum in the south. Since the start of 2025, northern markets have generally outperformed, particularly in Northeast China and parts of the central regions along the Yangtze River corridor. However, on a year-on-year basis, the northern region’s market share in November 2025 declined by 3.7 percentage points compared with the same period last year. Looking at a longer horizon from 2022 to the present, the region’s cumulative share has still risen by 5.4 percentage points, indicating a structurally positive medium- to long-term trend. Overall, the central and western regions outperformed eastern markets. In 2025, the central region’s market share increased by 1.2 percentage points year on year, with several previously pressured areas along the middle reaches of the Yangtze River showing signs of recovery. At the provincial level, some northern regions such as Liaoning, Tianjin and Shanxi posted weaker results in November, while growth was more pronounced in Chongqing, Guizhou and Fujian. This divergence has made the northern region the most elastic contributor to growth on a full-year basis. From a vehicle mix perspective, A00-segment electric vehicles performed strongly in North China and Northeast China, while A0-segment battery electric vehicles also recorded rapid growth across many regions. Micro and mini EVs emerged as the most direct beneficiaries among all segments. SUVs continued to deliver solid growth, with demand concentrated mainly in central and western China as well as the northwest and southwest. Coastal eastern markets remained relatively stable. In November, C-segment models performed well, and large three-row SUVs continued to see steady demand in tier-one cities and core consumer markets. New energy vehicles maintained relatively strong momentum in 2025, with both battery electric and hybrid models posting solid performance, though regional differences remained pronounced. In the central, western and northern regions, internal combustion engine vehicles still accounted for close to 60% of sales, while NEV penetration exceeded 50% in eastern and southern plain regions. In November, NEV growth in northern China accelerated, driven mainly by BEVs. NEV penetration has surpassed 60% in Hainan and Guangxi, while provinces such as Sichuan and the Yangtze River Delta are approaching 50%, with battery electric vehicles accounting for a rising share of total NEV sales. From a brand structure perspective, luxury vehicles continued to command relatively high shares in tier-one cities such as Beijing and Shanghai. However, in 2025, domestic brands made notable gains, while the market shares of both luxury and joint-venture brands declined. The report noted that joint-venture brands are facing increasing pressure in major cities, as substitution by domestic brands continues to accelerate.