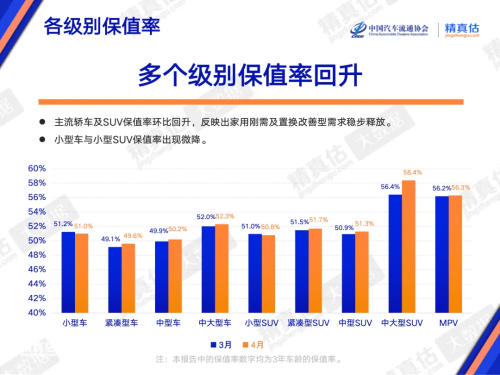

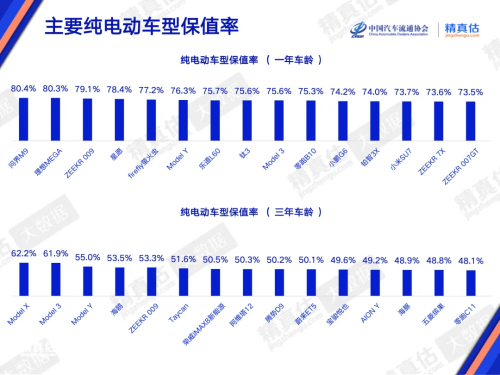

The China Automobile Dealers Association (CADA) released its China Auto Value Retention Rate Research Report for April 2026. According to the report, online used car volume reached 743,448 units in April, up slightly from the previous month, continuing the recovery trend seen in March. However, due to the dense launch of new models at the Beijing Auto Show and anticipated promotional campaigns around the May Day holiday, some consumers adopted a wait-and-see attitude. As a result, the figure was slightly lower than the 780,512 units recorded in the same period last year. Online used car listing volume trends Looking at value retention rates by vehicle segment, mainstream sedans and various SUV categories all posted modest month-on-month increases, reflecting the steady release of household demand and upgrade-oriented replacement demand driven by the “trade-in” policy. Specifically, mid-to-large SUVs led the segments with a 58.4% retention rate, followed by MPVs (56.3%) and large sedans (52.3%). Notably, the retention rate for small cars fell to 51.0%, primarily due to the direct impact of continued price cuts for small electric vehicles in the new car market. Value retention rates by vehicle segment Among premium brands, retention rates generally rebounded, highlighting the resilience of top-tier brands against market risks. Porsche retained the top spot with a three-year retention rate of 62.4%, followed by Lexus at 58.7% – both posting small month-on-month gains. Among the traditional German premium brands (BBA), Mercedes-Benz (56.7%) and BMW (51.4%) saw improved retention rates, while Audi (49.8%) experienced a slight decline. Worth noting is that Tesla, as an EV brand, achieved a retention rate of 57.0%, up from the previous month and ranking third. Performance changes of joint-venture brands The value retention landscape for joint-venture brands showed clear divergence. Japanese brands continued to dominate the leaderboard, with Honda (57.7%) and Toyota (57.0%) taking the top two spots. However, Toyota and Mazda (54.6%) both saw slight declines in their retention rates. In sharp contrast, American and Korean brands posted notable rebounds. Volkswagen (52.1%), Kia (50.7%), Buick (50.7%), and Ford (50.6%) all recorded month-on-month increases in retention rates. Changes among domestic (Chinese) brands On the domestic brand side, most Chinese NEV brands – including Li Auto, BYD, NIO, Zeekr, and Leapmotor – saw rising retention rates, suggesting that consumer “range anxiety” over the residual value of used Chinese-brand NEVs is gradually easing. Looking at the sub‑ranking for domestic battery‑electric midsize SUVs, the Onvo L60 topped the list with a 75.7% retention rate, followed by the Xpeng G6 (74.2%) and the Zeekr 7X (73.6%). Among domestic plug‑in hybrid midsize sedans, the top three were the Seal 06 (69.7%), Avatr 06 (67.8%), and Deepal SL03 (63.7%). For domestic plug‑in hybrid MPVs, the Trumpchi E8 PHEV ranked first with a 54.7% retention rate, followed by the Denza D9 (51.3%) and the Trumpchi E9 (49.1%) in second and third place, respectively. Value retention rates of major battery-electric models In the main battery-electric vehicle ranking for April 2026, the top three models by one‑year retention rate were the AITO M9, Li MEGA, and Zeekr 009. For the three‑year ranking, the top three spots were all captured by Tesla – the Model X, Model 3, and Model Y, in that order. In the main plug‑in hybrid vehicle ranking, for one‑year retention rates, the top three were the AITO M8, AITO M9, and Tank 400 PHEV – showing continued strong momentum for Chinese domestic brands. For the three‑year ranking, the Tank 500 PHEV led with a dominant 66.8%, followed by the Haval Raptor PHEV (60.5%) and the Tank 400 PHEV (58.8%).

![BYD, BYD reveals new flagship EV has a range of 1,008 km [Video]](https://cdn.topcarnews.net/thumb/id/aHR0cHM6Ly9pMC53cC5jb20vZWxlY3Ry-ZWsuY28vd3AtY29udGVudC91cGxvYWRz-L3NpdGVzLzMvMjAyNi8wNy9CWUQtR3Jl-YXQtSGFuLWZsYWdzaGlwLUVWLWltYWdl-cy5qcGVnP3c9MTUwMCZhbXA7cXVhbGl0-eT04MiZhbXA7c3RyaXA9YWxsJmFtcDtz-c2w9MQ/4049f882a47c576215dc589324539d9e.jpeg?t=20260802&post_id=49032)

![BYD, BYD reveals new flagship EV has a range of 1,008 km [Video]](https://cdn.topcarnews.net/thumb/id/aHR0cHM6Ly9pMC53cC5jb20vZWxlY3Ry-ZWsuY28vd3AtY29udGVudC91cGxvYWRz-L3NpdGVzLzMvMjAyNi8wNy9CWUQtR3Jl-YXQtSGFuLUZsYWdzaGlwLUVWLXJhbmdl-LmpwZz9zdHJpcD1pbmZvJmFtcDt3PTE0-NDAmYW1wO3NzbD0x/920438ef47ea4b64276e2d118cbc44a4.jpg?t=20260802&post_id=49032)

![BYD, BYD reveals new flagship EV has a range of 1,008 km [Video]](https://cdn.topcarnews.net/thumb/id/aHR0cHM6Ly9pMC53cC5jb20vZWxlY3Ry-ZWsuY28vd3AtY29udGVudC91cGxvYWRz-L3NpdGVzLzMvMjAyNi8wNy9CWUQtR3Jl-YXQtSGFuLWZsYWdzaGlwLUVWLWltYWdl-cy0xLmpwZz9zdHJpcD1pbmZvJmFtcDt3-PTIwMDAmYW1wO3NzbD0x/7e67fdf6aa71ab43cf8921346e319c49.jpg?t=20260802&post_id=49032)

![BYD, BYD reveals new flagship EV has a range of 1,008 km [Video]](https://cdn.topcarnews.net/thumb/id/aHR0cHM6Ly9pMC53cC5jb20vZWxlY3Ry-ZWsuY28vd3AtY29udGVudC91cGxvYWRz-L3NpdGVzLzMvMjAyNi8wNy9CWUQtR3Jl-YXQtSGFuLWZsYWdzaGlwLUVWLWltYWdl-cy00LmpwZz9zdHJpcD1pbmZvJmFtcDt3-PTIwMDAmYW1wO3NzbD0x/009ae9f6be1ef39cd2130fe4c294219a.jpg?t=20260802&post_id=49032)

![BYD, BYD reveals new flagship EV has a range of 1,008 km [Video]](https://cdn.topcarnews.net/thumb/id/aHR0cHM6Ly9pMC53cC5jb20vZWxlY3Ry-ZWsuY28vd3AtY29udGVudC91cGxvYWRz-L3NpdGVzLzMvMjAyNi8wNy9CWUQtR3Jl-YXQtSGFuLWZsYWdzaGlwLUVWLWltYWdl-cy0yLmpwZz9zdHJpcD1pbmZvJmFtcDt3-PTIwMDAmYW1wO3NzbD0x/c3d1447bac110db6de426e7e7f691a8b.jpg?t=20260802&post_id=49032)

![BYD, BYD reveals new flagship EV has a range of 1,008 km [Video]](https://cdn.topcarnews.net/thumb/id/aHR0cHM6Ly9pMC53cC5jb20vZWxlY3Ry-ZWsuY28vd3AtY29udGVudC91cGxvYWRz-L3NpdGVzLzMvMjAyNi8wNy9CWUQtR3Jl-YXQtSGFuLWZsYWdzaGlwLUVWLWltYWdl-cy01LmpwZz9zdHJpcD1pbmZvJmFtcDt3-PTIwMDAmYW1wO3NzbD0x/4048ff9aec9ba2b011563ef8cb066b9f.jpg?t=20260802&post_id=49032)

![BYD, BYD confirms new flagship EV has a range of 1,008 km [Video]](https://cdn.topcarnews.net/thumb/id/aHR0cHM6Ly9pMC53cC5jb20vZWxlY3Ry-ZWsuY28vd3AtY29udGVudC91cGxvYWRz-L3NpdGVzLzMvMjAyNi8wNy9CWUQtR3Jl-YXQtSGFuLUZsYWdzaGlwLUVWLmpwZWc_-dz0xNTAwJmFtcDtxdWFsaXR5PTgyJmFt-cDtzdHJpcD1hbGwmYW1wO3NzbD0x/c37374468f3a539ee1e0ce2b627e08d0.jpeg?t=20260802&post_id=48318)

![BYD, BYD confirms new flagship EV has a range of 1,008 km [Video]](https://cdn.topcarnews.net/thumb/id/aHR0cHM6Ly9pMC53cC5jb20vZWxlY3Ry-ZWsuY28vd3AtY29udGVudC91cGxvYWRz-L3NpdGVzLzMvMjAyNi8wNy9CWUQtR3Jl-YXQtSGFuLUZsYWdzaGlwLUVWLXJhbmdl-LmpwZz9zdHJpcD1pbmZvJmFtcDt3PTE0-NDAmYW1wO3NzbD0x/920438ef47ea4b64276e2d118cbc44a4.jpg?t=20260802&post_id=48318)

![BYD, BYD confirms new flagship EV has a range of 1,008 km [Video]](https://cdn.topcarnews.net/thumb/id/aHR0cHM6Ly9pMC53cC5jb20vZWxlY3Ry-ZWsuY28vd3AtY29udGVudC91cGxvYWRz-L3NpdGVzLzMvMjAyNi8wNy9CWUQtR3Jl-YXQtSGFuLUZsYWdzaGlwLUVWLTEuanBn-P3N0cmlwPWluZm8mYW1wO3c9MjAwMCZh-bXA7c3NsPTE/ec58de9827d67dc3cc45f86d6bcc427c.jpg?t=20260802&post_id=48318)

![BYD, BYD confirms new flagship EV has a range of 1,008 km [Video]](https://cdn.topcarnews.net/thumb/id/aHR0cHM6Ly9pMC53cC5jb20vZWxlY3Ry-ZWsuY28vd3AtY29udGVudC91cGxvYWRz-L3NpdGVzLzMvMjAyNi8wNy9CWUQtR3Jl-YXQtSGFuLUZsYWdzaGlwLUVWLWZyb250-LmpwZz9zdHJpcD1pbmZvJmFtcDt3PTIw-MDAmYW1wO3NzbD0x/819af4faa5c9804a09497b7d33d39bc1.jpg?t=20260802&post_id=48318)

![BYD, BYD confirms new flagship EV has a range of 1,008 km [Video]](https://cdn.topcarnews.net/thumb/id/aHR0cHM6Ly9pMC53cC5jb20vZWxlY3Ry-ZWsuY28vd3AtY29udGVudC91cGxvYWRz-L3NpdGVzLzMvMjAyNi8wNy9CWUQtR3Jl-YXQtSGFuLUZsYWdzaGlwLUVWLXJlYXIu-anBnP3N0cmlwPWluZm8mYW1wO3c9MjAw-MCZhbXA7c3NsPTE/25142d787c42fc350bb7230fb0006a37.jpg?t=20260802&post_id=48318)

![BYD, BYD confirms new flagship EV has a range of 1,008 km [Video]](https://cdn.topcarnews.net/thumb/id/aHR0cHM6Ly9pMC53cC5jb20vZWxlY3Ry-ZWsuY28vd3AtY29udGVudC91cGxvYWRz-L3NpdGVzLzMvMjAyNi8wNy9CWUQtR3Jl-YXQtSGFuLUZsYWdzaGlwLUVWLXNpZGUu-anBnP3N0cmlwPWluZm8mYW1wO3c9MjAw-MCZhbXA7c3NsPTE/cc2fac4025c1ccea61860176a17cec12.jpg?t=20260802&post_id=48318)