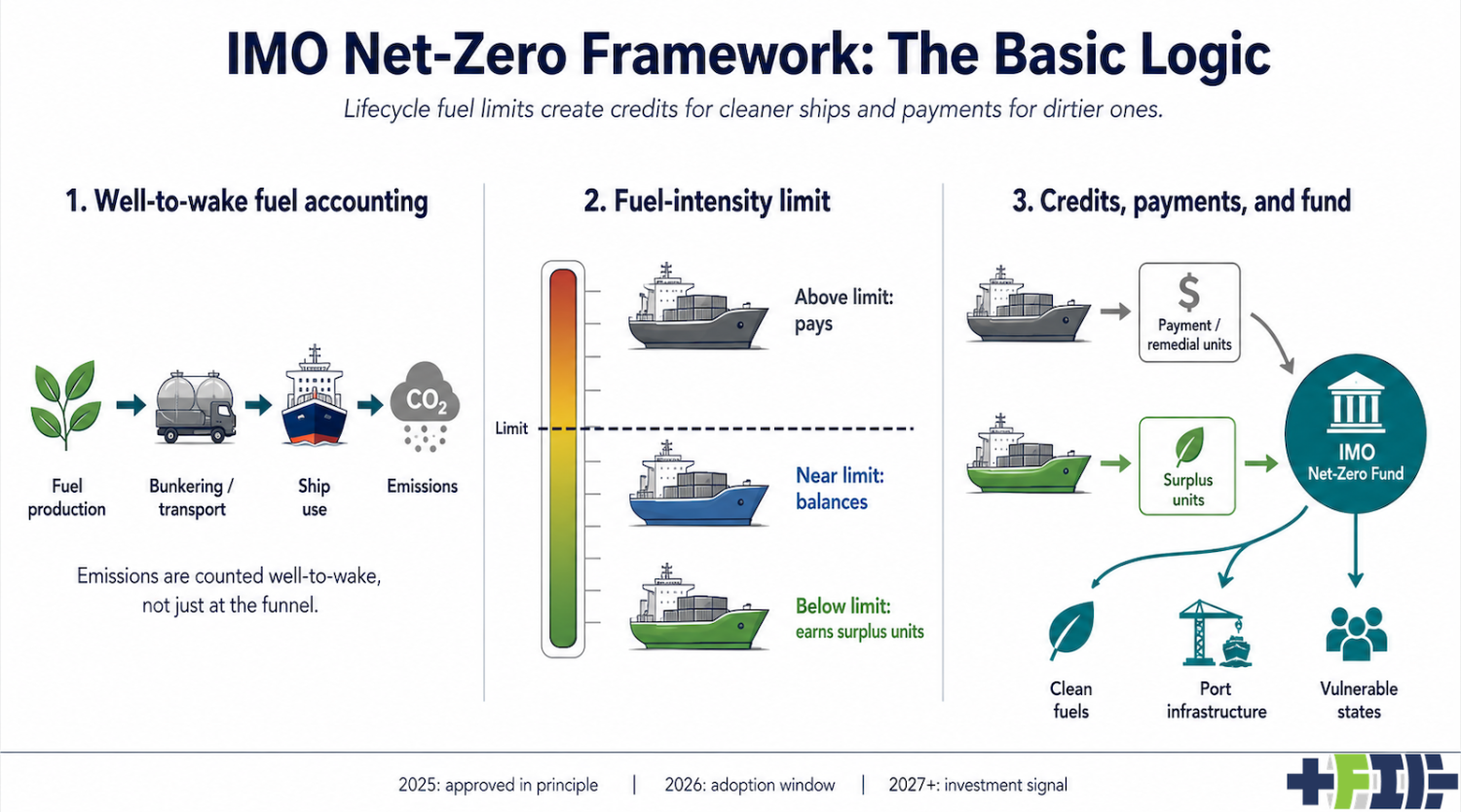

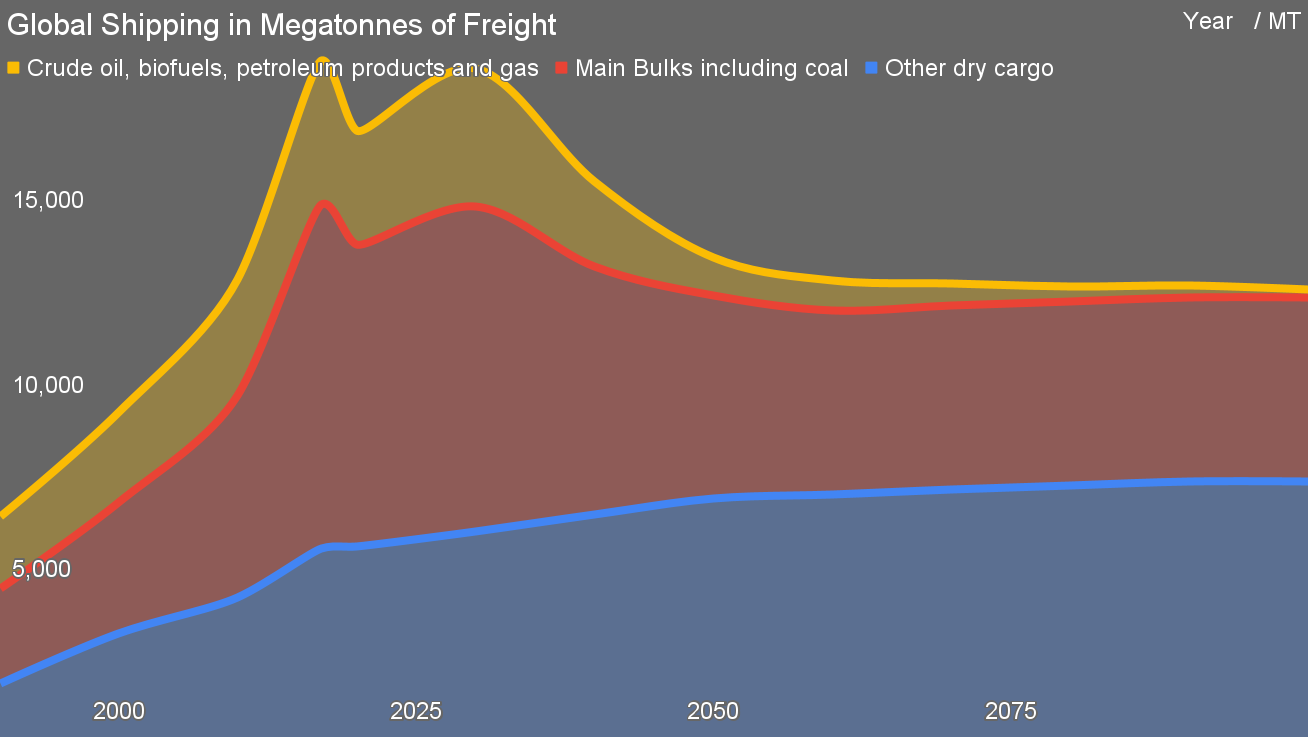

The IMO’s Net-Zero Framework came out of the latest Marine Environment Protection Committee meeting bruised, delayed, and still alive. For maritime climate policy, that matters. The International Maritime Organization has spent decades moving at the pace of the most cautious flag states, the most exposed bulk exporters, and the most defensive fossil fuel governments in the room. Yet after MEPC 84, held from April 27 to May 1, 2026, the core architecture remains on the table: a global fuel standard, lifecycle emissions accounting, and an economic mechanism that starts to put a price on greenhouse gas emissions from ships. That is not victory. Formal adoption did not happen. The next decisive window is now MEPC 85, scheduled for November 30 to December 3, 2026, followed by a resumed extraordinary session on December 4 if the committee confirms the path forward. That places the IMO’s next decision after the United States midterm elections on November 3, 2026. The timing matters because the United States has become the largest near-term political risk to adoption. The United States has not been a passive skeptic. Under the Trump administration, it has been an active spoiler. In October 2025, the framework was expected to move to formal adoption. Instead, a Saudi-led delay motion passed 57 to 49, with 21 abstentions, after strong opposition from the United States and Saudi Arabia. Reuters and Associated Press both reported the US pressure campaign, including threats of trade retaliation against countries supporting the framework. That is not a technical disagreement about emissions factors. It is great-power coercion applied to a global climate rule. The midterms will not directly decide the US position at the IMO. The executive branch will still run foreign policy and the US delegation until January 2029. But Congress affects the volume, credibility, and political cost of obstruction. A Republican hold would make US opposition look more durable and coordinated. A Democratic House, or a Democratic Congress, would not force the administration to support the framework, but it would create oversight, hearings, budget fights, and a public signal that Washington’s position is contested. In an IMO process where many countries are deciding whether to stand firm or fold under US pressure, that distinction matters. The clock is ticking for another reason. Ships last a long time. A vessel ordered in 2026 can still be operating in the 2040s. Port power systems, bunkering networks, fuel contracts, and shipyard production lines also have long lives. Every year of delay increases the risk that owners order another generation of ships designed around cheap fossil fuels, then complain when those assets collide with climate rules. Maritime decarbonization is not waiting for magic. It is waiting for owners, ports, fuel suppliers, financiers, and governments to stop treating a manageable transition as if it were an unsolved engineering mystery. The short history is enough to explain the delay. Kyoto left international shipping to the IMO. The IMO then spent years doing what was politically easiest: efficiency rules such as EEDI, SEEMP, EEXI, and CII. Those measures improved ship design and operations, and they reduced fuel waste, but they did not force a fuel transition. Market-based measures, including levies and trading systems, were discussed in the early 2010s and then parked. The 2018 Initial GHG Strategy moved the institution toward absolute emissions reductions, but the 2023 Revised GHG Strategy was the real break. Once the IMO accepted net-zero greenhouse gas emissions by or around 2050, efficiency rules alone no longer matched the goal. The second 2023 break was lifecycle accounting. At MEPC 80, the IMO adopted lifecycle greenhouse gas guidelines for marine fuels. That moved the argument from the convenient narrowness of tank-to-wake toward the honesty of well-to-wake. Tank-to-wake counts what comes out of the ship. Well-to-wake counts the whole chain, from feedstock extraction, cultivation, capture, or electricity generation, through production, transport, bunkering, and use onboard the vessel. It includes carbon dioxide, methane, and nitrous oxide. That is the difference between regulating the funnel and regulating the fuel system. This is why the shift took so long. Tank-to-wake was convenient for incumbents. LNG looked cleaner when methane leakage was ignored. Hydrogen and ammonia looked cleaner when the fossil gas or electricity used to make them was ignored. Biofuels looked cleaner when feedstocks and land-use pressures were waved away. Methanol looked simpler when fossil, biomass, waste-based, and synthetic pathways were treated as if branding mattered more than chemistry. Well-to-wake accounting does not answer every question, but it forces fuel claims to carry their real supply chains into the room. Infographic of IMO Net Zero Framework, by author with ChatGPT. The Net-Zero Framework is imperfect, but it reflects this better framing. It applies to large ocean-going ships, generally those above 5,000 gross tonnage, which the IMO says represent more than 85% of international shipping emissions. It combines a global fuel standard with a greenhouse gas pricing mechanism. Ships that beat the standard can create surplus compliance units. Ships that miss it must cover the gap, including through payments into an IMO Net-Zero Fund. The fund is intended to reward lower-emission ships, support fuel and infrastructure deployment, and assist developing states. That is not the clean universal levy many climate-vulnerable states wanted. It is a negotiated hybrid, and negotiated hybrids are what survive in global shipping. The important question is not whether the framework is elegant. It is whether it creates a durable direction of travel, moves the sector onto lifecycle accounting, and starts shifting investment away from fossil defaults. On those tests, it matters. Megatons of freight shipping through 2100, by author. The largest analytical mistake in much maritime discussion is treating future shipping as today’s shipping with different fuels. That is the wrong baseline. A decarbonized world does not ship the same volumes of coal, crude oil, refined petroleum products, and LNG. It does not move the same mass of fossil molecules across oceans. It does not replace every ton of coal and oil with a ton of hydrogen, ammonia, or synthetic fuel unless policymakers make strange choices that fight the economics of electrification. Shipping is measured in tons and ton-miles, and fossil fuels are heavy. Coal, oil, and gas are not rounding errors in seaborne trade. UNCTAD’s Review of Maritime Transport has shown for years that dry bulk and tanker trades dominate global seaborne tonnage, and a large share of that is energy commodities or industrial bulk tied to the fossil system. As coal power declines, coal shipping declines. As oil demand falls with electric vehicles, heat pumps, rail electrification, and industrial electrification, tanker demand declines. As gas is displaced in power and buildings, LNG growth weakens and later reverses. The fossil fuel cargo base is not permanent. Some new cargo appears. Critical minerals move. Clean technology moves. Some biomass, biofuels, methanol, ethanol, ammonia, or other low-carbon molecules may move. But these do not replace fossil fuel shipping ton for ton. A world that electrifies road transport does not need tankers to deliver the missing gasoline. A world that electrifies heat does not need LNG carriers to deliver the missing gas. A world that makes more steel in electric arc furnaces from scrap ships less metallurgical coal and less iron ore than a blast-furnace growth case. The first fuel saved in shipping is the fuel not burned because the cargo was no longer required. That is why the “how can we possibly fuel all ships with green fuels?” panic is overstated. We do not have to fuel all of today’s ships with green fuels. We have to decarbonize the smaller and different fleet that remains after fossil bulk trade declines. That still leaves a large global industry carrying food, manufactured goods, minerals, vehicles, machinery, chemicals, and construction materials. But it changes the size of the problem. It also changes which solutions matter. Batteries will do more than official maritime models assume. The usual objection is that batteries cannot carry a container ship across the Pacific. That is true today and not the point. Maritime shipping is not one route, one vessel, or one duty cycle. Ferries, harbor craft, offshore support vessels, tugboats, inland vessels, lake vessels, short-sea ships, and many coastal routes have known schedules and fixed ports. That is the geography batteries like. The vessel returns to the same dock, or a small set of docks. The operator knows the route. Charging infrastructure can be built where the ship already stops. Ferries are the leading edge. Norway proved the first wave. China is scaling larger battery vessels. British Columbia’s Island Class ferries were built as battery-capable diesel hybrids, waiting for shore power to catch up. Uruguay’s China Zorrilla showed that very large ferry batteries are no longer a laboratory exercise. Batteries are becoming normal in ferry procurement because route economics, energy efficiency, maintenance reductions, and public expectations all point the same way. Ports are the second leading edge. Port equipment, drayage trucks, yard tractors, cranes, cold ironing, harbor craft, ferries, and local vessels all point toward the same electrical infrastructure. A port that builds substations, shore power, battery buffering, renewable power purchase agreements, smart charging, and vessel charging is building the energy platform for maritime decarbonization. Once that platform exists, every additional electrified vessel becomes easier. Ports stop being only logistics nodes. They become grid-connected energy nodes. Hybrid electric systems matter because full electrification is not required for batteries to cut fuel demand. Hybridization allows smaller engines to run closer to efficient load, provides hotel loads at berth, reduces local air pollution, supports zero-emission operation in ports and sensitive areas, and creates a bridge to larger battery fractions as prices fall. The battery cost curves that transformed cars, buses, trucks, and stationary storage are now arriving in maritime. Studies from even five years ago often assumed battery costs and energy densities that are already stale. For the remainder of shipping, simple liquid fuels look better than dramatic molecules. Methanol has moved up the list because it passes more practical tests than I once gave it credit for. Biomethanol is constrained by sustainable feedstock, but it is real. Ethanol deserves more attention than it gets for similar reasons. Biofuels made from biomass waste have far more feedstock availability than most people assume. The test is not perfection. The test is low lifecycle emissions, safe handling, workable storage, certifiable systems, and realistic scale for the smaller shipping sector of the future. Hydrogen, ammonia, LNG, and shipboard carbon capture all have significant shortcomings. Hydrogen brings low volumetric density, cryogenic or high-pressure complexity, safety zones, and a high delivered-cost stack. Ammonia brings toxicity, green hydrogen dependency, combustion concerns, and port safety burdens. LNG brings methane leakage and fossil lock-in. Shipboard carbon capture brings energy penalties, space claims, offloading logistics, and a missing global CO2 handling chain. As I have argued in previous analyses of maritime hydrogen, ammonia math, LNG lifecycle emissions, and shipboard carbon capture, these options are not impossible, just uncompetitive. The cost story is where the debate becomes calmer when the math is done. Low-carbon marine fuels will cost more than bunker fuel. That does not mean decarbonized shipping makes ordinary goods unaffordable. Fuel cost is one component of shipping cost. Shipping cost is one component of delivered cost. Delivered cost is one component of retail price. The carbon-price component is smaller again. By the time the cost is spread across thousands of tons of cargo and thousands of kilometers, the consumer price effect is often modest. Burning 1 ton of heavy fuel oil releases a bit over 3 tons of CO2 before upstream emissions are counted. If a ship used 50 tons of fuel in a day, that is more than 150 tons of CO2. A carbon cost of $100 per ton of CO2 would add more than $15,000 for that day of fuel emissions. That looks large to the vessel operator. But if the ship is moving tens of thousands of tons of cargo, the cost per ton of cargo is small, often a few dollars or less depending on vessel size, load factor, speed, route, and fuel burn. For containerized cargo, that cost is then divided across high-value goods. A phone, a pair of shoes, a refrigerator, or a box of components does not become inflationary because the ship paid more for fuel across an ocean. Bulk commodities are more exposed because they have lower value per ton. Grain, ore, cementitious materials, and basic chemicals feel freight costs more than electronics or apparel. But even there, the policy answer is not to pretend marine fuel can stay outside climate policy. The answer is revenue recycling, targeted support for vulnerable importers, efficient vessels, and a global fund that directs money toward countries with real exposure. A global IMO framework is better for equity than fragmented regional charges with no common redistribution logic. Shipping is hard to regulate politically, but not that hard to decarbonize technically. Ships are large assets operated by professional firms. Routes are planned. Ports are fixed nodes. Fueling is centralized. Maintenance is scheduled. Regulators can focus on a small number of large vessels and owners compared with the millions of buildings, hundreds of millions of vehicles, and dispersed industrial heat users that other sectors must manage. The practical roadmap is visible: electrify fixed routes, hybridize the next band, build port electrical infrastructure early, and use sustainable alcohol fuels and biofuels for the routes that remain hard. The real barriers are political, institutional, and narrative. Fossil fuel exporters want to protect demand. LNG suppliers want to preserve the transition-fuel story. Some shipowners want to delay capital decisions while keeping optionality. Some developing countries have valid concerns about trade costs and revenue distribution. The United States, under Trump, has chosen to defend the old system with threats rather than help design the new one. Saudi Arabia has done what a petrostate would be expected to do. Equity concerns should lead to better revenue design, not indefinite delay. The December 2026 IMO window matters because it comes after the US midterms and before another year of investment drift sets in. If the midterms strengthen the administration’s congressional platform, Washington’s threats will look more durable. If the midterms weaken it, other countries may feel more room to proceed. Either way, the rest of the world should not give the United States a veto over maritime decarbonization. The IMO is a global body. Shipping is a global system. US obstruction is consequential, but it is not physics. The industry should prepare as if the framework, or something close to it, will arrive. The EU is already moving through its emissions trading system and FuelEU Maritime. China is moving on batteries, shipbuilding, and port electrification. Customers are asking for lower-carbon logistics. Insurers and financiers are watching transition risk. Ships ordered now will operate under rules that become stricter over time. Waiting for perfect certainty is not prudence. It is a decision to be late. Maritime decarbonization is manageable because the future fleet is likely smaller in fossil bulk terms, because many vessel classes are electrifiable, because hybridization cuts fuel demand where full electrification is not ready, because practical liquid fuels can serve much of the hard-to-electrify remainder, and because the cost per ton of delivered goods is small enough to absorb with limited consumer price impact. The IMO framework surviving matters because it keeps the global signal alive. The framework is late, compromised, and still at risk. It is also the clearest global maritime climate architecture the sector has had. The clock is ticking because the path is visible, the economics are manageable, and the excuses are wearing thin.