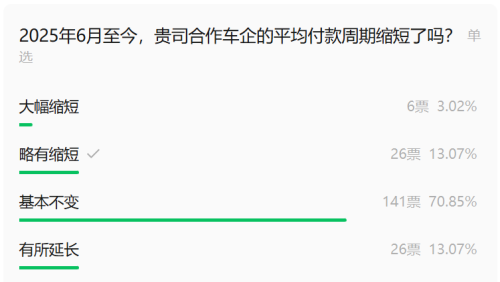

Gasgoo Munich-The spectacle of suppliers "taking the stage" to endorse new cars is playing out with increasing frequency.Just last night, Bosch China took to Weibo to declare that its "millimeter-level precision protection and clear driving vision" were empowering the Huajing S, generating buzz for the global debut of the "large six-seater" model. This is hardly an isolated incident. So far this year, suppliers like Bosch, Forvia Hella, Michelin, Brembo, and Valeo have rallied to build buzz ahead of the Zeekr 8X launch. Similarly, when Changan Automobile unveiled its first localized Thai model, the NEVO Q05, Autoliv announced it was powering the vehicle with a "globalization plus localization" safety solution. Once hidden behind the curtain, parts suppliers are now stepping into the spotlight of new product launches with unprecedented visibility.Image source: Weibo screenshotFrom braking systems and chassis to intelligent lighting and safety features, names that once appeared only in industry forums or supplier directories are now joining joint marketing campaigns aimed directly at consumers. A wave of supply chain "hidden champions" is moving to center stage. This shift represents more than just a change in corporate branding strategy; it reflects a profound transformation in the underlying logic of the automotive industry.From Behind-the-Scenes Support to Center Stage: The Supplier's Role Has ShiftedIn the era of internal combustion engines, automakers held absolute dominance at the industry's core, while parts suppliers remained in a subordinate position. This created a one-way model where automakers defined requirements and suppliers simply fulfilled them. Back then, even global giants like Bosch and Continental rarely engaged in direct brand marketing to consumers.This "invisibility" was both a deliberate choice and a necessary reality for supply chain firms. The nature of B2B business meant they didn't need to interface directly with end-users, while long-standing, stable partnerships allowed them to remain comfortably hidden in the shadow of the automakers' brands.But the technological upheavals of electrification and intelligence have shattered this rigid pattern.Take the Zeekr 8X. Core components like the Bosch IPB 2.0 braking system, Michelin Pilot Sport 5E tires, and Brembo high-performance braking technology are no longer cold specifications on a configuration sheet. They have become key selling points that directly define the vehicle's capabilities and build a competitive edge. When braking distance, turning radius, and moose test results become hot topics among consumers, the suppliers behind the technology naturally get their moment in the spotlight.More importantly, today's consumers pay close attention to core components. They actively compare air suspensions, LiDAR systems, and silicon carbide power controls. A supplier's brand endorsement not only adds technical credibility to the new car but also leverages the vehicle's high visibility to boost its own influence—a win-win scenario.In an interview with Gasgoo, Valeo noted that joint marketing campaigns between automakers and suppliers reflect more than just promotional value; they signal a profound shift in the industry's supply-demand dynamics. Both sides are moving beyond traditional transactional relationships toward deeper levels of joint development and ecosystem integration. This deep partnership spans the entire collaboration process, with joint promotion at product launches serving as a natural expression of that alignment.Image source: VCGThe underlying logic for this shift is straightforward: the technical architecture of smart electric vehicles differs vastly from traditional internal combustion cars. In the era of electrification, automakers aiming for differentiation must often bind deeply with core suppliers early in the R&D phase to jointly define technical solutions. When a supplier's technology is deeply woven into the vehicle's DNA, it becomes only natural for them to step into the spotlight and speak up.Rising consumer awareness has further fueled this breakout for the supply chain. Many buyers of high-end smart EVs are tech enthusiasts who can discuss the 8155 chip, Orin-X computing power, 800V high-voltage platforms, and silicon carbide control systems with ease. Consequently, a supplier's brand power now directly influences purchasing decisions. Supply chain firms have keenly recognized this shift and are consciously building their own brands, moving from industry-only recognition into the public eye.A New Ecosystem of Co-opetition: Reconstructing the OEM-Supplier RelationshipOn the surface, the supply chain collectively endorsing new cars looks like a marketing stunt. But behind the scenes, it represents a deep reconstruction of the cooperative relationship between automakers and suppliers.Traditionally, the relationship between automakers and suppliers could be described as "linear": information flowed top-down, with demand passing from the automaker to Tier 1 suppliers, then down to Tier 2 and Tier 3, leaving little room for collaborative R&D. But in the era of smart EVs, innovation requires synergy across the entire supply chain; a weak link in any single stage becomes a bottleneck for the whole vehicle.Consequently, the relationship has evolved from "upstream and downstream" to "partners in the journey," upgrading from a transactional buyer-seller dynamic to a strategic partnership of shared interests and risks.Valeo reveals that automakers are indeed more open to joint marketing with suppliers, with many actively inviting partners to participate. This shift in attitude is a concentrated reflection of changing cooperation models and value logic during the industry's electrification and intelligent transformation. Technological innovation by core component makers has become a crucial pillar for building differentiated products. The dynamic between automakers and suppliers is shifting from a linear chain to a network structure, moving from traditional procurement toward deeper collaborative co-creation—a trend becoming increasingly visible across the industry.At the heart of this collaboration is the adoption of "joint development." In the past, automakers defined product parameters first, then tendered to suppliers, awarding contracts to those who met standards at the lowest price. Suppliers had little say, simply developing to spec. Today, automakers invite core suppliers to participate early in R&D. Together, they customize technical solutions based on model positioning, target audiences, and brand identity. A supplier's technical prowess, R&D timeline, and capacity planning are now deeply interlocked with the automaker's product matrix.Valeo states that on one hand, this approach allows it to visually demonstrate the mass-production application of its innovative technologies to the industry and end-market, showcasing its technical strength and real-world value. On the other hand, it hopes to use this connection to explore and build a healthy industry ecosystem defined by joint creation and shared value with automakers.Image source: VCGOf course, in this new ecosystem of co-opetition, the balance between rivalry and partnership is delicate. While the two sides collaborate deeply on R&D to boost product competitiveness, they also engage in subtle competition over value distribution and technical influence.Automakers are wary of being held hostage by any single supplier, so they maintain control by diversifying their supply chains. For instance, they might bring in two or three battery suppliers or two intelligent driving solution providers, creating an internal race mechanism. This ensures supply security and provides leverage in price negotiations. Meanwhile, suppliers are locked in fierce technological contention. The first to mass-produce next-generation technology secures major orders from top clients and gets to define industry standards. From millimeter-wave radar and 4D imaging radar to steer-by-wire chassis and 800V electric drive systems, every specialized field is crowded with competitors.Even more noteworthy is that some leading automakers are encroaching on territory once belonging to suppliers. In-house chip development, proprietary operating systems, self-driving algorithms, and even battery manufacturing—once unimaginable—are becoming reality. The logic for this upstream expansion is clear: core technology cannot be outsourced, and differentiation cannot rely on external parties. But this creates new pressure for suppliers: what happens when your customer becomes your competitor?This complex interplay of rivalry and cooperation is the defining characteristic of today's OEM-supplier ecosystem. Collaboration and competition are no longer mutually exclusive choices but simultaneous, dynamically balanced forces. Only suppliers that can clearly define their positioning and establish indispensability in this complex environment will stand a chance of winning in the next phase.From "Endorsement" to "Symbiosis": A Long Road AheadThe collective endorsement by suppliers is undoubtedly a clear signal that relations are warming. But sharing a stage at a launch event does not equal true symbiosis. Beneath the surface buzz, the chronic issues of the traditional OEM-supplier relationship persist, and new conflicts are surfacing. The reconstruction of this relationship—from "standing on stage" to genuine strategic alignment—has only just begun.Indeed, the relationship has evolved positively in recent years. More automakers are opening their R&D systems to core suppliers during the product definition phase, making joint development and early involvement the norm. In core fields like autonomous driving and air suspensions, suppliers are no longer mere executors following blueprints; they are collaborators deeply involved in defining the technological roadmap.Dong Yang, chairman of the China Automotive Power Battery Industry Innovation Alliance and vice chairman of the China EV 100, recently noted that the industry is facing breakthroughs across multiple fields. No single automaker can master or lead development in so many areas simultaneously. New technologies require collaboration and refinement between technical capabilities and market demands to deliver mature user experiences, making deep cooperation essential. Moreover, as new technologies continue to evolve and iterate, the relationship is no longer a simple transaction; it requires long-term partnership. This means the shift from a "one-off deal" to a "long-term companion" model is an inevitable requirement of the times.But there is another side to the coin. Structural contradictions in the traditional relationship haven't vanished just because of a few joint press conferences. The most typical—and most challenging issue for suppliers—is payment terms. In the Chinese auto industry, it is an open secret that automakers withhold payments. Payment cycles of six, nine, or even more months are standard practice for some OEMs. The widespread use of bank acceptance drafts further reduces the actual value suppliers receive.To address this, the China Association of Automobile Manufacturers (CAAM) released the "Initiative on Payment Norms for Auto Suppliers" in September 2025. It stipulates that payment cycles must begin upon delivery acceptance and cannot exceed 60 calendar days. A CAAM research report published in February showed that the average payment cycle for 17 key automakers had dropped to 54 days.However, a significant gap remains between policy initiatives and industry reality. A survey by Gasgoo of roughly 200 voters (an open poll where multiple employees from one firm could vote) found that only about 3% reported a "significant reduction" in payment cycles, while about 13% noted a "slight reduction." Strikingly, 70.85% of participants said payment terms remained "basically unchanged," and another 13% reported they had "lengthened." This suggests that while some leading automakers have acted, many suppliers have yet to experience substantial improvement in their day-to-day operations. Turning "initiatives" into reality—especially regarding the core issue of payment terms—will require a long and arduous process.The root cause of the persistent payment issue lies in the power imbalance within the relationship. Leading automakers control the allocation of orders, and suppliers, desperate to keep their clients, often dare not raise objections over payment terms. This structural dilemma cannot be solved by a single paper initiative. It requires a deepening of industry consensus, optimization of competition rules, and a fundamental shift in mindset—where automakers truly view suppliers as partners, not tools.Dong Yang also issued a warning to the industry: be wary of the trend toward "full-stack in-house development" and the neglect of partners. He pointed out that Tesla didn't pursue full-stack self-development because it wanted to; it did so because traditional system suppliers couldn't meet its needs for progress or iteration speed. Even so, Tesla continues to seek new system partners, with CATL serving as a key collaborator on batteries.He emphasized that the "winner-takes-all" mentality from the internet sector is harmful to the auto industry. Cars are long-cycle products; new technologies, structures, and features cannot be monopolized indefinitely. Furthermore, the extreme safety requirements of automobiles make them fundamentally different from internet products that can be updated rapidly. Therefore, automakers should engage in close, long-term collaboration with key partners rather than trying to do everything themselves.The reconstruction of the OEM-supplier relationship cannot be achieved through a few joint press conferences. Payment terms, intellectual property rights, and price transmission mechanisms are challenges that require systematic solutions. Encouragingly, the industry is becoming aware of these issues. Some leading automakers are actively optimizing payment management and shortening cycles, while others are establishing long-term strategic frameworks with core suppliers, pledging sustained collaboration across multiple vehicle platforms.Taking the stage is a good start, but it is not the finish line. The next phase of this relationship will be defined by who can offer goodwill and solutions on real issues like payment terms, IP rights, and profit distribution. Those automakers willing to treat suppliers as true partners, rather than tools, will build the most solid supply chain moat for the next stage of competition.